Here we go again–can the rally in stocks and bonds continue after taking a tiny breather last week? At this moment equity futures are darned near flat.

Last week the S&P500 fell by less than 1%–closing at 3972 which was 27 points below the close of 3999 the previous Friday. The index was off about 3% until Friday when markets rallied about 2% –based on no particular news.

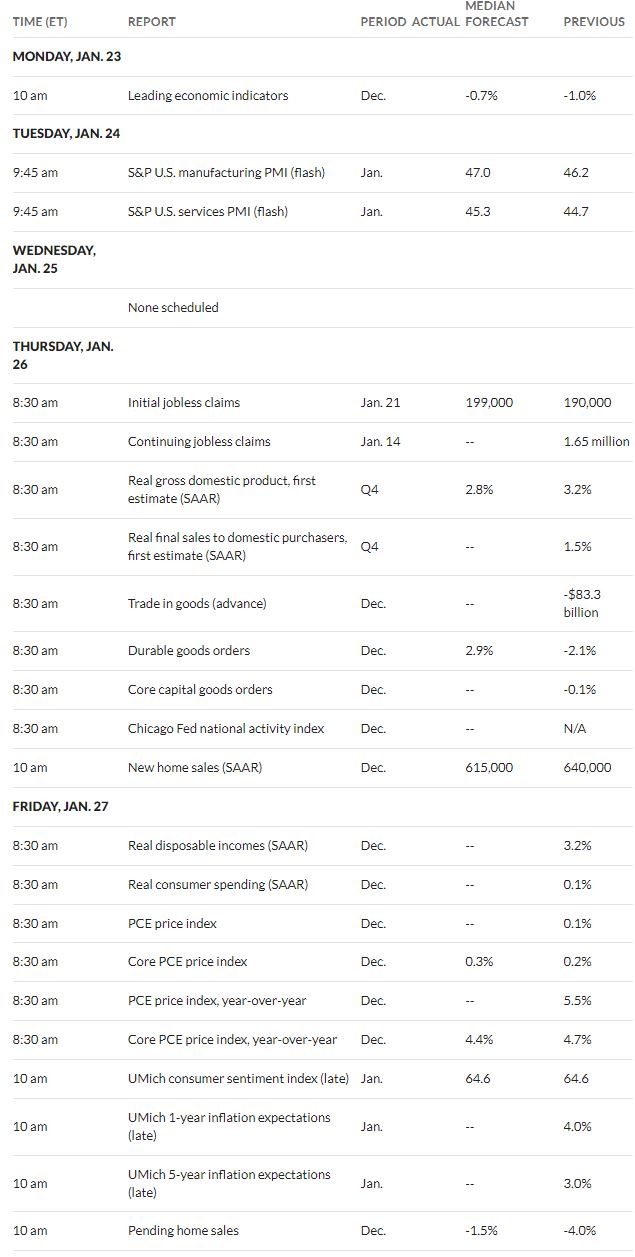

Interest rates, as displayed by the 10 year treasury, closed at 3.48% on Friday after trading as low as 3.37% on Thursday. The closing yield was 3 basis points below the previous Fridays close on 3.51%. The slowing of retail sales, as reported last week, shows the economy potentially slowing with slowing inflation–a decent recipe to keep rates from spiking too much higher. This week there are plenty of economic reports which may move markets.

The Fed Reserve balance sheet showed a reduction in assets of about $20 billion last week. We are now at $8.49 trillion which is down from a record high of $8.97 trillion—guess we have quite a ways to go—just so we get it low enough so there is dry powder for the next quantitative easing cycle–whenever that may occur.

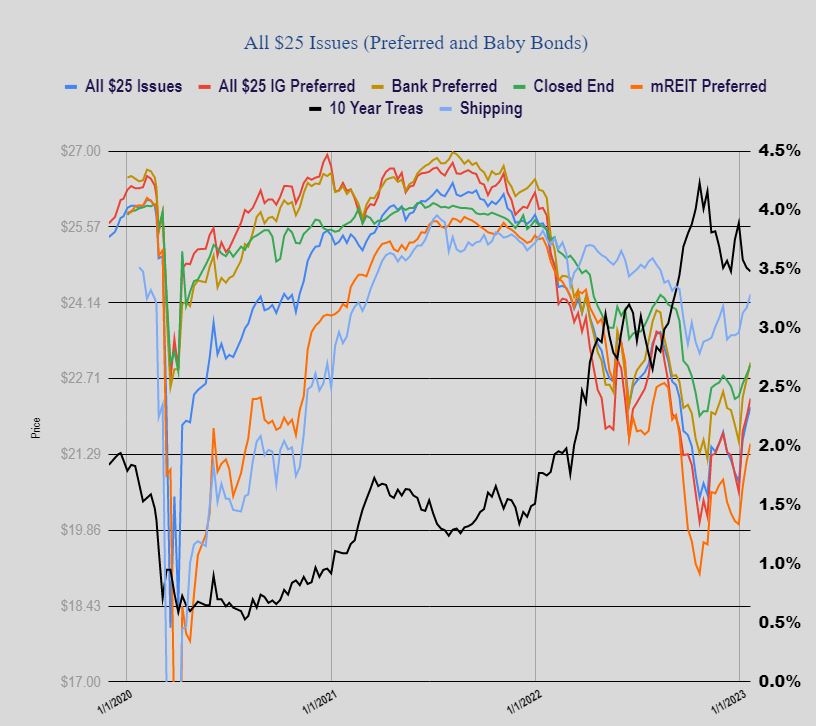

Last week the average $25/share preferred or baby bond continued higher with a gain of 28 cents–most of the gains occurred in the earlier part of the week. Investment grade issues rose 34 cents, mREIT issues rose 33 cents, CEF issues rose 17 cents and shipping issues rose 25 cents.

We had no new issues priced last week.

The previous week we had the new Redwood Trust 10.00% fixed-rate-reset preferred begin to trade and in spite of the very high coupon the issue closed at $24.85. This issue remains trading on the OTC market.