Well last week was a very strong week for equities of all types. The S&P500 gained around 4% on the week–a very strong rally after a Fed rate hike and relatively week GDP numbers for the 2nd quarter. Seems like a little backing and filling is in order–but who really knows.

Interest rates moved lower last week with the 10 year treasury closing the week at 2.64% which is 14 basis points lower than the close the previous week. Certainly the bond markets are signaling a belief in a slowing economy, but as we all know these things can take time to develop.

The Fed balance sheet fell by $9 billion last week–of course the balance sheet will never fall appreciably because of congress’s spending habits. With the balance sheet at $8.89 trillion down from an all time high of $8.96 trillion I think the odds of the balance sheet ever getting below $8 trillion are pretty low.

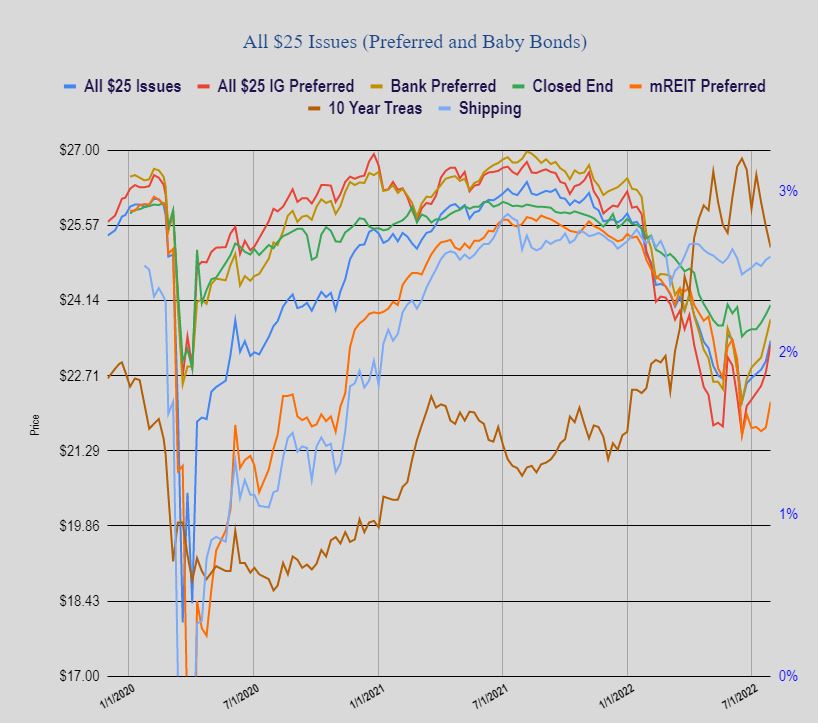

Last week was an excellent week as $25 preferred stocks and baby bonds moved strongly higher.

The average $25/share preferred and baby bond moved up by 39 cents last week. Investment grade issues powered higher by 53 cents, banking preferreds moved 37 cents higher, mREIT issues were 49 cents higher, while CEF preferreds were up only 18 cents and shipping preferreds moved 6 cents higher.

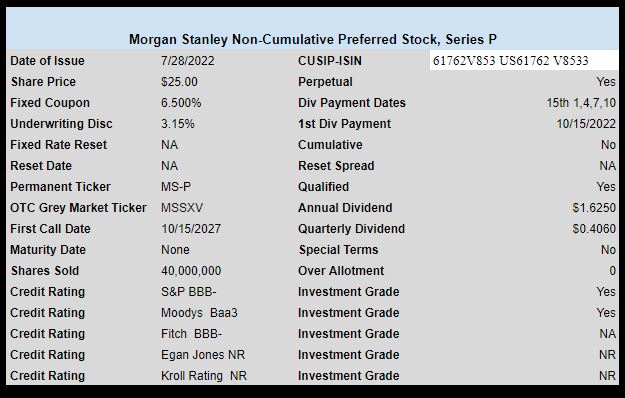

Last week we only 1 new issue priced and the issue was from Morgan Stanley.

Morgan Stanley (MS) priced an investment grade perpetual non-cumulative preferred stock with a very tasty coupon of 6.5%. The issue is now trading on the OTC grey market under ticker MSSXL (a change from the ticker shown in the chart below) closing at $26.06 on Friday.

Tim.. August 1 , wake-up call……….,Bargains fading Fast…. Thank you..

Yep they have gotten to be harder to find.

BPYPM up big today so I shaved my position…looking for a replacement at some point

Sold everything in the $23.30s…done with it

But it’s intriguing to me what the out-sized action is all about…

Today’s action indeed was astonishing – I hold several hundred shares of the BPYs and am underwater by more than this company should be… what is there about BAM that raises apparent concerns? Too much office real estate?

randall,

Same here – I’ve got 400 BAMH at a cost basis of $25.13! (it’s now at $19.73). I got into it a year or so ago when it was hard to get 4.60% yield on an IG issue.

It’s my most underwater position too, but I’m not sweating it. I didn’t choose to sell it when things were looking hairy in June and July. It’s gone up ~13% from it’s $17 low, so there’s some movement. I could have doubled this position to improve cost basis but I don’t want more of it as I’ve got 800 of BPYPP.

Yeah, I had 1000 BPYPM at $24.67 from a year ago and watched it erode down to the low $19s. When it popped this week to the mid-$23s, I took the chance to exit. With the divvy collected, I escaped with a smidgen of red instead of what might have been $3K-$4K. Now I need to deploy that cash at some point.

yazzer – I love doing just what you did, then buy the freakin 1,000 BPYPM back now at the high $21’s – you’ve just “made” $1,100.

Tim,

I cancelled my order for the Morgan Stanely 6.5%, after my order at $25.25. Not even close. Today, RWAYL appeared today both at Schwab and Fidelity. I do recall that you and several other deem this baby bond from a small but seemingly decent BDC could be worthwhile. I bid $25.13 for 200 shares when the market opened and it got filled very quickly. Actually I forgot if the coupon was 7% or … After I called Schwab, I saw that the coupon was 7.5%, decent unlike OXLCN 7%. It went up and down with small volume. For those who might be interested, I believe that you should be able to get it around $25.13 or possibly lower.

BTW, recently I bet on SHO hotel recovering. Both Schwab and FIdo seem to like SHO plus market action on SHO. I picked up quite a few SHO-H and sold off some GLOP-B. Someone at old Doug’s web like OZKAP, regional bank with one notch + below IG. I picked up some before the ex div. Today I picked up some remants of RIV-A at $24.7, now a penny below.

Thank you for your BEST Income Investing WEBSITE in this world.

All my best to you and your family.

Thanks John–I will look into this deeper (RWAYL) tonight for a nibble tomorrow. I do have around a 1/2 positive in the RIV-A issue because it is a solid issue (being a CEF).

Your most welcome on the website. About to get back on it heavier (I think). May day job is slowing some more.

Simple question. What is the relevance of maturity date versus call date? I noticed that RWAYL has Term-matures on 07/28/2024 and a call date of 07/28/2027. TIA Windyducat

Other way around: call date is 28 jul 2024, matures on 28 jul 2027.

From the prospectus supplement at https://www.sec.gov/Archives/edgar/data/0001653384/000110465922082047/tm222341-9_424b2.htm: “The Notes will mature on July 28, 2027…. We may redeem the Notes in whole or in part at any time or from time to time on or after July 28, 2024 at our sole option at $25. Holders of the Notes will not have the option to have the Notes repaid prior to the stated maturity. ”

Pretty clear language:

– as of 28 jul 2024, the company may (at its option, not yours) redeem the Notes. If you’re holding them and they decide to redeem early, you will receive the liquidation pref ($25) plus accrued & unpaid dividends.

as of 28 jul 2027, the company must redeem the Notes.

Clear?

Bur, thank you. The dates are reversed on another site, which I thought was odd, and thus the question.

I think of call and maturity dates like cooking steaks on a grill. After a few minutes, you can take them off the grill (call them)… or leave ’em on the grill for awhile and let them mature until they are well done. Unfortunately they will tell you how to eat your steak, as they “may” redeem them any time after the call date.

Not knowing the degree of your sophistication regarding term dated preferreds and bonds, the simple difference between call date and maturity date is maturity date is a mandatory date on which the bond/preferred will be redeemed by the company at par/liquidation preference amount. Call date is an optional date at which a company has the right but not the obligation to redeem the security. Usually a company’s call ability is continuous from the given date onward, however, it is almost always expected to be exercised when it’s least beneficial for the bond owner and most beneficial to the company. In other words, it will be exercised by the company at a time when the owner of the security will have a hard time replacing the yield he has been receiving with a comparable quality security of a similar maturity. Is this what you’re asking?

” Usually a company’s call ability is continuous from the given date onward…” This is correct. However, there are exceptions – some are only callable on dividend payment dates, and the “Resets” will mostly be callable only at the time of the reset, typically every 5 years. There will also be a notice requirement, generally, but not always, 30 days. Check the prospectus.

Knowing how verbose I can be, I chose to leave out the exact same exceptions you’ve added, nh …. lol You’re of course correct.

I actually find you usually to be quite concise. Maybe not to the extent of mcg, but still concise.

Windy, 2WR as usual did a fine job explaining that companies typically “call” an issue when it is too their advantage. In 2021, in round numbers, a gazillion preferreds (actually ~125) were called because companies could raise new funds at a lower rate.

A common problem that some investors had was only looking at the “current yield” and not understanding the “yield to first call.” For example, lets assume a $25 preferred had an 8.0% coupon which means that it paid out $2.00 per year in dividends. In 2021 when interest rates were low, maybe people had bid the price up to say $27.00 which would give a current yield of 2/27= 7.40%. Investors would see that large, juicy dividend yield and NOT understand that the issuer could “call” that issue and only pay you $25.00. If the investor paid $27.00 for it, he would suffer a $2.00 capital loss.

We saw this repeatedly in 2021. It is not as much of an issue currently since interest rates have increased and many preferreds trade for less than their $25 call price. But NOW is the time to understand how “calls” work and make sure you do NOT get yourself into a situation where you can suffer a major capital loss if the issue is called. Some III’ers make educated guesses whether an issue will be called on XYZ date and are willing to risk a capital loss of say 5 or 10 cents. The risk of losing 10 cents is very different than potentially losing $2.00.

My strong recommendation is for ALL preferred investors to take the time to understand how calls work and use that data to influence your buy/sell decisions.

We are either in a recession already or will be in one soon. What I know about recessions is that inflation and treasury yields peak during recessions and then fall after. I still think the fed funds rate and core PCE are going to merge.

I think its more likely we stop paying China for holding our treasuries as a form of taxation. Would add an immediate 3% boost.

Oh yeah- a default on debt would help… lower the US credit rating.

Many more debt holders too.

QRTEB today up from $4.27 to $18.23 on heavy volume of 14.1 million shares for a stock that averages 82,000 shares. Market cap increased from 1 billion this morning to 7 billion at closing today. I have searched for news but nothing comes up under the various QRTEA, QRTEB, QVCC bonds, QVCD bonds and QRTEP (which has fallen from 110 per share 6 months ago to a little above $50 despite its 8 percent face rate. A very strange occurrence today.

How will if affect QRTEP, QVCC, QVCD????? A search of their prospectus on quantum online does not provide any clues either.

>How will if affect QRTEP, QVCC, QVCD?????

Short answer, it will not.

I was wondering about the difference between QRTEA and QRTEB, so I looked it up.

“What is the difference between the Series A common stock (QRTEA) and Series B common stock (QRTEB) of Qurate Retail, Inc.?

The Series A common stock (QRTEA) has one vote per share, while the Series B common stock (QRTEB) has ten votes per share.

The Series B common stock is exchangeable at any time on a one-for-one basis for Series A common stock. The Series A common stock is not exchangeable for Series B common stock.

The Series A common stock is broadly held and actively traded; the Series B common stock is held by a relatively small number of holders and thinly traded.”

Source: https://www.qurateretail.com/investors/stock-data/faq

So, it looks like this is partly about controlling the company. It seems like some well-informed people are quite bullish on the stock.

Alternate theory: short squeeze.

No default. Just taxed away before delivered. $240 billion payment would be saved against their $8 trillion dollar treasury position. Could even remove tariffs costing consumers extra at stores.

Mica, what do you mean by ‘taxed away before delivered’?