Well is the bottom in for now? I don’t really know–no one knows, but there is plenty of speculation by the talking heads expecting a 10% bounce in common stocks at this time–of course with the 6.5% bounce last week it may be near over.

Last week the S&P500 rose by a healthy 6.5% in a holiday shortened week of trading. The index started the week at 3675 and closed on Friday at 3912–right near the high for the week.

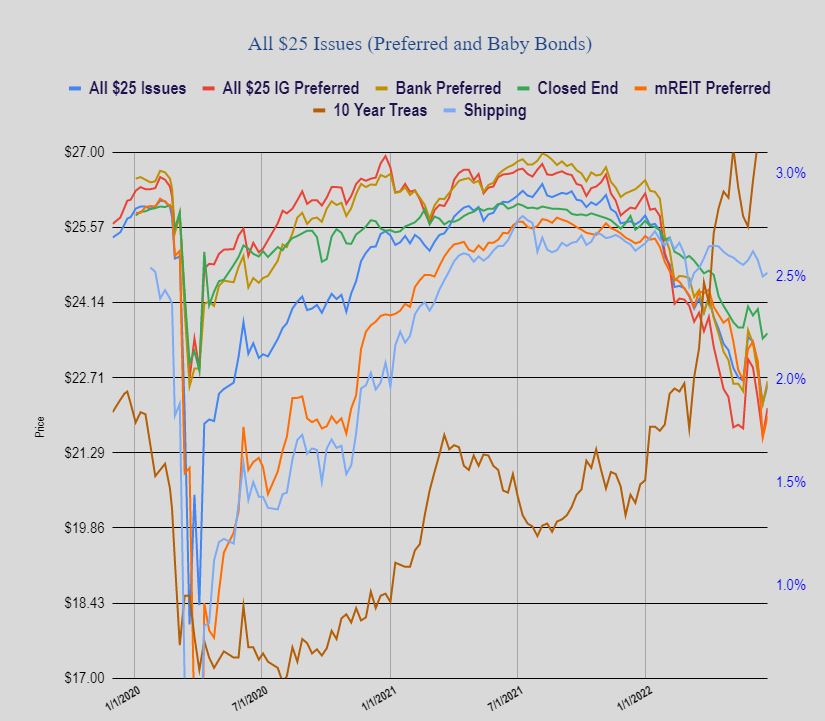

The 10 year treasury yield was at 3.24% the previous Friday traded as low as 3.01% during the week before closing the week at 3.125%. Recessionary fears appear to have a grip on the market–for now. Friday we will have another inflation indicator–the PCE index will be released on Thursday and will be closely watched by markets as it is said to be a key indicator for Fed Chair Powell.

Last week the Fed balance sheet rose by $2 billion to $8.934 trillion.

Last week we saw some strength in the average $25/share preferred stock and baby bond with prices rising by 35 cents/share. Investment grade shares were very strong with gains of 54 cents/share. Bank issues rose 43 cents, mREIT issues rose 40 cents, while CEF preferreds rose just 10 cents.

As has become typical in these times of volatility no new income issues were priced.

Even First trust appears to have thrown in towels on equities… When you lose Brian Westbury……. BTW he’s very concerned with M2

Hmmmmmmmmm, radio silence here this morning on III. I wonder if that means everyone is feeling as clueless as I feel today…

I made a couple trades but didn’t accomplish anything other than shuffling money around. Rearranging the deck chairs?

That is funny, Martin. I almost made a trade this morning too. But then thought what am I accomplishing doing this, so I passed. I did make one puny 100 share trade this week and it has netted me a negative $50 bucks for the effort.

Im really just in hold waiting for a lot of cash to be freed up from redemptions next month. And then promptly look to flip it into… 6 month up to 2 yr Tbills.

3% treasuries? Are you expecting the floating 6%ers to get into some kind of trouble?

Im just widening out my diversity. Credit spreads could widen to make a 6% er a 6.5% or 7%. Even 50 bps is a $2 butt kicking. Its possible we havent felt any pain yet. There are a lot of issues still positive on the year including divis, and we really havent had any disorderly pain yet, except for the 4% issues that was easily avoided if one was inclined towards capital protection.

But that being said since I know nothing and dont really have any feel either, I still bought 400 shares a week or two ago of WELPM at $106 that is below 6%. I definitely am heavily heavily leaned towards call anchored, term dated, and live floaters. But I am about to lose a big chunk of the call anchored stuff so I will drop that money into the short duration treasuries. Maybe if Tex’s boy Rob Arnott is correct, I should dial up another friend of mine and do another 10k IBond gifting.

I’m trying to figure out why MITT-B is trading higher than MITT-A.

so you can sell B and buy A. Taking the profit is easier than asking why.

I traded every share of B that I had for A last week when B was 2% below A, and I thought I was so clever…

Sailor… For arb swaps I find (free) big charts to be helpful. Get the chart of one ticker, select “compare to” “symbol” for the other ticker and the historical spread will be shown for the time frame selected. Early September and late November were similar opportunities for the tickers mentioned. prices that invert often could suggest a good candidate for this technique

Thanks for the resource, Lucky. I hadn’t seen that before, and it looks like a good first screen for pairs of issues that criss-cross frequently in value.

What I try to do is make a swap that *should* pay off with a later trade, but also that I feel gives me better value even if the later trade doesn’t materialize. My simple model for MITT A/B is that 100 shares of MITT A are worth 100*(8.25/8) = 103.125 shares of MITT B. That’s because either basket gives the same quarterly dividend of $51.5625. Yes, I recognize that MITT-B might be worth just a bit more than that if one or both issues are called, or if MITT goes bankrupt. However, at current valuations the risk of the former seems low.

Charting this takes a fair bit more work. From Marketwatch, I can download historical quotes for both issues and then multiply the MITT-B closing prices by 1.03125 and put them next to the MITT-A closing prices. Then, I can make a graph showing the fluctuations in my model. Of course, a simpler approach is to just divide the current MITT-A price by the current MITT-B price. If the result is bigger than 1.03125, MITT-A is relatively overvalued. If the result is smaller, MITT-B is relatively undervalued.

Comparing a fixed rate issue like MITT-B to a (soon to be) variable rate issue like MITT-C is harder, and I won’t bore you with how I deal with that. It’s enough to say that I traded MITT-C for MITT-B when their prices were equal and was happy to do so. In hindsight, the market is telling me that was a mistake.

Cheers,

Retired Sailor

I also swapped early. Sometimes I’ll keep some shares in reserve in case it gets more ridiculous. Doesn’t always work. Satisfied wirh 1% bonus every couple weeks or so, in addition to the divvy. MITT-C has been a litte wild lately if you include that in the mix.

Not really doing much. I get the feeling something will happen over the next several months to allow a good buying opportunity so I am just reinvesting divs/interest/distributions and tossing some money at the account every once in a while to buy something like PACWP. Everyone seems to think fixed income securities will get cheaper some day soon and it really does not hurt to wait and see. I have enough invested for now. No hurry.

Last week was likely a dead-cat bounce, and we certainly haven’t had capitulation . . . But

Anyone else feeling a touch of a ‘FOMO put’ under the market?

It’s like potential buyers are seeing inflation down to 3-4% by the end of 2023, employment cooling down, oil coming down with economies slowing, central banks trying to thread the needle . . . “let’s party”!!

Feels a touch FOMO-ey.

I am sensing people are nervous and unsure of themselves. That stage. The up days appear to be lower volume then the down days. No conviction. Just people flailing around hoping for some gains and the wind keeps changing direction almost daily as news comes out. Talking heads cannot make up their minds and they trot them out constantly. Capitulation might not even appear. It could be a slow grind down and the bottom does not ring a bell. The bottom might not even be known until much later. So your fomo feeling may very well be gone before Friday.

Tim I enjoy and appreciate the Monday morning Kick-0ffs to start the week . Hey having the 10 year Treasuries in the 3’s is almost back to normal, whatever that is now-a-days. Some risk averse investors may just jump on board but the inflation issue may prevent them from doing so.

“Last week the Fed balance sheet rose by $2 billion to $8.934 trillion.”

Does not look like the Fed is living up to its words about shrinking its balance sheet. Kinda stuck in a hard place wanting to, but really not able to.

Been lurking here the past year….found this group during the onset of the covid correction and it was my “sane and safe” place. Thanks for the great host and members.

IMO this is a tradable bottom, but not the bottom. Many buyers including tutes like these prices regardless if the market moves lower. IMO we are in “no mans land”….no one knows. I think we are not going to get off with the simple scenario….fed rases rates, inflation abates and there is a shallow recession. Too many unknowns, like oil and ag, wage inflation, future price/earnings, supply chain. No fed stimulus…market must stand on its on.

Thank you for “decloaking”, windy. The water is warm jump in!

windy….never heard the word tutes before. When I looked it up, I found definitions ranging from inflicting corporal punishment, to a tin foil opiate pipe, to a Spanish card game. None seemed to fit so just wondering…

A famous college with Instutute in the title calls itself The ‘tute. So I’m guessing it means Institutional investors.

Whatever it is, if you’re Cajun, you better not mess with it…. https://www.youtube.com/watch?v=Yqf10CmdiD0&ab_channel=Rockin%27Sidney-Topic

I like a little Zydeco every now and then. I live in Louisiana.

The urban dictionary says tutes is slang for prostitutes…however, I’m going to guess there’s a letter missing and he meant to say touts. 😬

Citadel and Martin….. I like the blend of institutional investors and prostitutes…..it’s not about the love, it’s about the money

Concur. Back in my salad days (early 1980s), cynical analysts would call always-rosy analysts “lousy touts.” So touts are what I thought of right away. Perhaps windy will enlighten us at some point!

As Martin G got correctly, Institutional investors. Cheers!

That was quick! Thx.

Tutes are the big guns, with all the money. Institutional investors include credit unions, banks, large funds such as a mutual or hedge fund, venture capital funds, insurance companies, and pension funds. They control 75% of the equity markets. We are the remaining 25%, smaller but smarter, and much more nimble.