Another exciting week in the stock market–although in a positive sort of way with the S&P500 closing the week at about 4501 which was about 1.6% higher than the previous Friday close. No doubt we will follow this week up with more volatile trading this week.

Interest rates as represented by the 10 year treasury broke convincingly above the 1.90% mark to close the week at 1.93%. No doubt heading to 2% soon–I just hope it takes a full month to get through that mark since we need digestion of rates to keep from decimating income securities, which had another rough week last week.

The Fed balance sheet grew by $13 billion last week reversing the minor fall in assets from the week before.

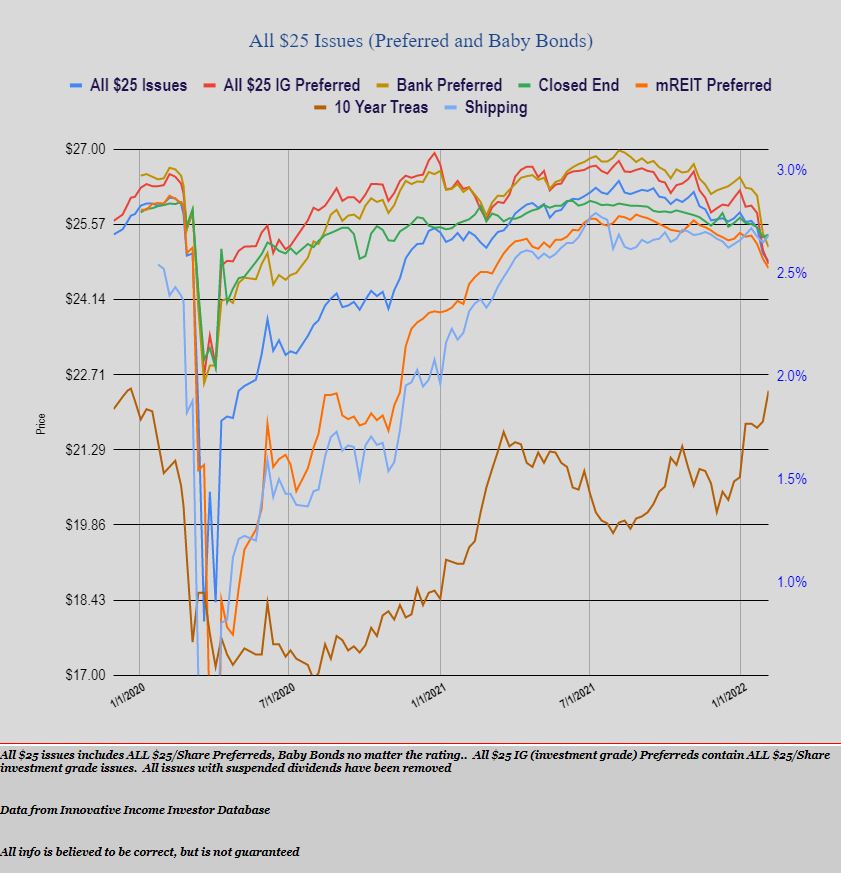

Last week was another difficult week for $25/share preferred stocks and baby bonds with the average issue falling another 15 cents. Investment grade issues fell by 27 cents as lower coupon, high quality issues fell by almost double the rate of fall of ‘junkier, high coupon’ issues. Banking issues fell by 27 cents, while mREIT preferreds fell by 18 cents while the shipping issues were the only winners on the week at a plus 13 cents.

Last week we had 1 new preferred issue brought to the market with another preferred being reopened.

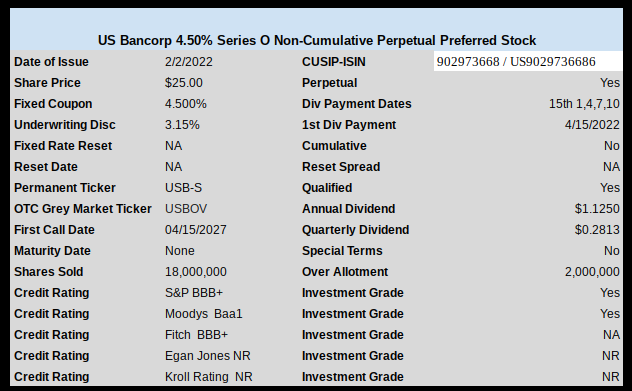

US Bancorp (USB) brought a 4.50% perpetual preferred to the market. The investment grade issue is trading on the OTC market under ticker USBOV and closed last week at $24.67.

mREIT Arbor Realty (ABR) ‘reopened’ their 6.25% fixed to floating rate preferred (ABR-F) by selling over 3 million new shares at pricing of $24.20. Unfortunately this sale served to send the issue to a closing price of $23.80 last week.

It’s becoming blatantly obvious to me that the only path open for all preferred and baby bond holders going forward is to sell them all and join Eminem and The Biebs and buy into the Bored Ape Yacht Club…….. I might even start the InnovativeBoredApeYachtClubInvestors,com website…….. ha… Just kidding, Tim……. It makes investment sense, doesn’t it? What could go wrong?

I had success trading PLBY. There is some excitement about the Rabbitars and other NFT art in which they are involved.

https://playboyrabbitars.com/#meet-the-rabbitars

I don’t own it now, but I watch it every day — it ran from $10 to $60 last year.

Hedgeye loves the stock, and McGough is one of the smartest guys in the room.

https://www.youtube.com/watch?v=fkL0gSvbU5w

Two investment terms can scare me when applied to the markets. They are “exciting” and “interesting”.

My scary investment term is ‘This time it is different’ !

Back when we were charged commission for trades my scariest term was “Partial Fill”

I had a 1 share fill on a sale of $4 OTC stock at Schwab last week. So I netted about -$3 of proceeds.

Another scary term is “this is a once in a generation financial event”. Starting with the 1987 black friday crash, seems I have been through about 8 of these once in a generation events!

Most of my issues have not been impacted significantly as they are term preferred or BB’s due in 4 years. I am taking a beating on my mReits such as NRZ and NLY. While they are floating issues (2024, 2023 respectively). that doesn’t seem to be helping them. They are both down almost 4% for me.

Just musing out loud. I am not making any changes. Too many things in flux, semi irrational behavior with some issues, the bargains may not be true bargains yet, no consistency with the action from my point of view, etc…

Take HBANP. Last trade is 22.60 it seems. That is nearly a 5% yield from a split IG bank. Then you have BOH-A, last trade, at 23.29 for less yield (4.7%). IG from Moody’s. Both have a 1st call date of 2026.

Lots of examples like this. Which is the “more correct” pricing going forward? HBANP even pays a div way before BOH-A to boot timeline wise.

All of these people selling hard and fast. What exactly are they doing? There is nothing to buy yet that pays quite a bit more for the same type of risk. I do not see them coming down the pipeline anytime soon.

So isn’t that the question to figure out? Are they just sitting on cash and plan to for quite a while? There are only so many choices to buy that mature soon, protect you from inflation, etc… to pile into. I need to think about this. Or will they simply start buying the same old stuff in 6 months when they realize there is only junk for more yield?

fc:

Not just “people” selling. The behemoth preferred ETF PFF has already had $400+ million in outflows in 2022. It is still an $18.8 Billion ETF.

This is only the beginning of the outflows for them this year, and they are mostly price “insensitive” when their shares outstanding start to fall and they need to sell. They hold only 17 basis points worth of “cash”.

Rob,

Yes. That is true. I guess I use people generically to represent everything while your statement rings much more accurate.

Which makes me think I should be examining PFF’s holdings more closely to figure out what they might be dumping and when it could almost be finished down the road. Specific issues or the whole basket? Not sure how ETF redemptions play out when a market maker demands the actual shares in exchange for ETF shares.

https://www.ishares.com/us/products/239826/ishares-us-preferred-stock-etf/1467271812596.ajax?fileType=csv&fileName=PFF_holdings&dataType=fund

Here is their detailed holdings. HBANP appears to be listed based on the price of the equity.

BOH is not listed. Holding up stronger. I guess that could possibly make HBANP a deal right now. I wonder what others are on that list performing poorly compared to something else. Hm.

Thanks for the reply.

As between HBANM and HBANP, do you like HBANP better? HBANM has 5% YTC (12/1/2022) and $1.425 coupon. It seems like it should hold up better if interest rates continue up. Of course, if there’s a dip in rates, there’s probably more upside potential in HBANP, but right now it seems like we’re all concerned about the present trend continuing (I know I am). I have a few shares of HBANM.

I agree that the outflows for any preferred stock fund might just be beginning, given the most likely course of the Federal Reserve on interest rates.

You might see a serious “puke” of preferred stock in the late fall, when tax-loss selling begins.

Yield on cost going up 5% or more on some preferred. All over most likely .50-.75 real increase in yields.

Fixed income investors sure know how to throw out the baby with the bathwater. They are pros!

HBAN’s common took a beating recently, so the preferred just fell in tandem, even though outside of being seized by the FDIC, Bank preferreds pay their dividends on time.

“All of these people selling hard and fast. What exactly are they doing?”

Selling and buying back at a much better price.