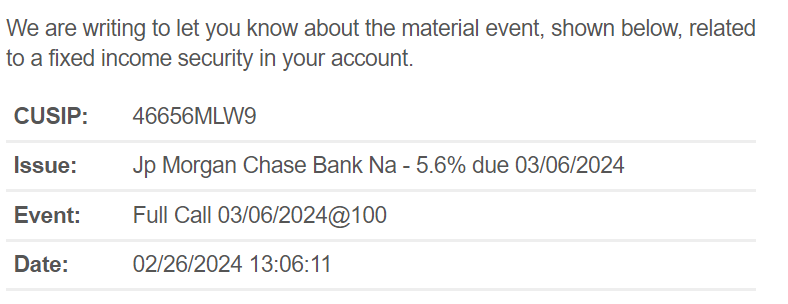

Well yesterday I had my 1st ever call on a CD–a JPMorgan 5.60% issue. As shown below.

I wondered how the mechanics of a call worked—now I know. Prior to 2 years ago my CD experience was only with local bankers.

It looks like JPM is only needing about .2% or .25% in reduction of rates to make an early call—so I will have more calls since I have a 5.7% issue as well.

So while I would rather receive 5.6% than 5.3% rates remain good and I will roll these unexpected funds into a new CD.

The notice I received is below.

JP MORGAN SUPPRISE CD CALL! CALLED MY CD!!!

i WILL NOT TRUST jP mORGAN AGAIN!

I wouldn’t buy callable CDs these days (or maybe ever). The bank gets duration as well as the option to call and you take the interest rate risk.

I also wouldn’t buy most fixed rate callable preferreds that are trading close to par. If rates fall, good chance they will be called and no potential upside in terms of capital gain. If rates rise, they could fall in value…a lot. Sounds like a lose-lose situation to me.

I agree, Dick, and only have a couple that are callable. Most of the time the tradeoff was a bit lower yield, which I accepted for duration security. And the few callables I have were bought with the implicit understanding they would be redeemed first call date. For example I have a 5.8% CD that is a 5 year duration, callable this October. I have it on my ledger as an October maturity. If I am wrong, I will be pleasantly surprised.

If the bank calls the CD, it’s because the market is offering them lower rates/better terms now. It’s not time to be mad at JP Morgan. They are just exercising the option that you agreed to when you bought the CD. If you want better terms, stop buying these things.

I own shares of SLMNP that are noncallable by the company but I have an option to sell the preferred shares back to the company for $848.27, which comes out to a yield of 7.07%. I bought my shares right around the option price and it’s one of my larger positions. If interest rates rise significantly and I can get better that 7.07% in safer companies, I will exercise my option and switch to something better. If rates go a lot lower, I’ll continue to hold and the company will have to keep paying me above average yields. Sounds kind of like the callable CD except my position is like JP Morgan and the LYB (preferred issuer) sounds like the retail investor who bought the CD. I can do ok if rates go up or down or unchanged.

You have to try to stack the deck in your favor as much as the market will allow. You need to be able to understand a potential “path to victory” and what you’ll do if rates go up, down or sideways.

I agree Gridbird. There is a reason for the higher yield on a callable CD. Like you, If I have a 2-year cd with a 1 year call, I think of it as a 1-year issue. For simplicity, however, I now tend to stay away from callable issues

That is on you, not JP Morgan

Know what you buy. You gave them the right to call the CD in exchange for a higher than market rate.

They can issue new CDs at a lower rate so they naturally exercised their right to call. Smart business

DO NOT BUY JP MORGAN!!!

I had a big CD there, it was 15 mo 5.60 callable this March. NBD no big deal. But in general I only buy non calls. So looks like highest I was seeing around 1 yr 5.30.

Thats brokered. Direct I’d be surprised if we couldn’t find 5.40+

Does anyone else read the post title like from Pink Floyd’s Another Brick in the Wall?

Hey!

Dimon!

Leave CDs alone!

It’s been a long week

Guilty as charged….

Probably better as HEY!, JAIME!, Leave those CD’s alone!, because all in all, CD’s are just another brick in the wall (of investing)

BearNJ,

I looked up the CUSIP 46656MLW9 on Schwab – it shows a maturity date of 8/6/2024. It looks like it was originally an 11-month CD.

Correct Red Owl

Which begs to ask How much concession (fee) did JPM have to pay to issue that. Before 2018 they were paying big bucks. As in 50-70 basis points. That must have compressed significantly as rates dropped from 5 down to 1. Maybe dropped to 10 basis points? And w rates surging over 5 did the broker concession stay razor thin??

So they have to eat the concession, and pay another to replace. (Plus the concession is time weighted. So a 1 yr CD pays dealer 2X a 6 month CD. Which means if they did a callable CD all the commission is paid up front. It effectively ups the cost in basis points. If they paid 10 basis points for 1 year, and called it in 6 months the deal costs 2X 10….20 BPs……..In other words they have to be able to re-issue at east 25 points cheaper. This call doesn’t make a lot of sense to me!?!

Its not clear to me what the maturity date is vs the call date on your CD. The end of your post suggests that the maturity date and the call date are the same. 3/6/2024.

I used to avoid callable CDs, but have warmed up to them. I look at a callable CD, something like say, a callable 18-month CD as a two-part transaction: a 12 month non-callable CD sure-thing plus a 6-month option in the bank at the tail. As long as I am happy with either tail outcome, I am okay with buying the callable CD. (However, I was was hoping Chase would need .050 before a call – I will find out in a few months. )

JMO. DYODD.

BearNJ–sorry I wasn’t clear–Red Owl had it correct. Maturity was originally 8/24.

I don’t avoid the callables because at least I get the superior coupon while it is available–but there is always reinvestment risk.

Tim,

when choosing a CD over Tbills, do you take into consideration that Tbills are state tax free and Cds are not? 3 month Tbills are in the 5.4% range today.

thx

JF

I do. CDs mostly in IRAs, treasuries in taxable accounts.

Jim—I do not take taxes into account–I only invest through my IRA’s. Actually I have some large accounts in ‘savings accounts’ that I pay taxes on each year–but no choice on investment other than Farmers Insurance savings @4.5%