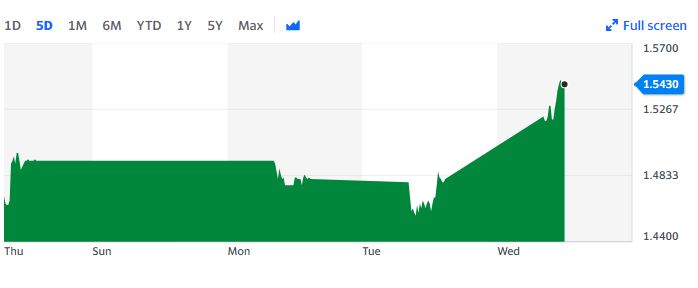

Today I see that the 10 year treasury is popping a bit–up 7 basis points to the 1.54% – 1.55% area.

Logic tells us that with Fed tapering supposedly going on there is substantially less demand for all the paper that the Treasury has to sell. We have seen some firming of interest rates globally and minor reductions in quantitative easing which could possibly reduce demand for U.S. paper.

I will not be surprised to wake up one morning and find the 10 year popping into the 1.70 to 1.75% area in the month ahead. It is likely that this ‘pop’ will cost us a little capital, but by remaining in shorter maturity bonds and term preferreds losses should be very minimal.

Your website is the go-to source for our investment community. Thank you and have a blessed new year.

if they float to “libor + x%” (which the NRZ ones do) will Libor be zeroed out and the X% be the new floating rate?

Franklin – if you’re asking what happens if LIBOR is completely done away with on a fixed/floating rate issue, the answer most likely is in the individual prospectus… It’s possible that some of the older F/F may not have covered the possibility but most others do and, I don’t believe there’s any particular convention set. In other words, the answer as to what would happen is a case by case basis…… Want the particular answer on an NRZ issue? This is from NRZ-A Brace yourself for some fun reading from the DESCRIPTION OF THE SERIES A PREFERRED STOCK section:

For each Dividend Period during the Floating Rate Period, LIBOR (the London interbank offered rate) (“Three-Month LIBOR Rate”) will be determined by us or a Calculation Agent (as defined herein) as of the applicable Dividend Determination Date, in accordance with the following provisions:

• LIBOR will be the rate (expressed as a percentage per year) for deposits in U.S. dollars having an index maturity of three months, in amounts of at least $1,000,000, as such rate appears on “Reuters Page LIBOR01” at approximately 11:00 a.m. (London time) on the relevant Dividend Determination Date; or

• if no such rate appears on “Reuters Page LIBOR01” or if the “Reuters Page LIBOR01” is not available at approximately 11:00 a.m. (London time) on the relevant Dividend Determination Date, then we will select four nationally recognized banks in the London interbank market and request that the principal London offices of those four selected banks provide us with their offered quotation for deposits in U.S. dollars for a period of three months, commencing on the first day of the applicable Dividend Period, to prime banks in the London interbank market at approximately 11:00 a.m. (London time) on that Dividend Determination Date for the applicable Dividend Period. Offered quotations must be based on a principal amount equal to an amount that, in our discretion, is representative of a single transaction in U.S. dollars in the London interbank market at that time. If at least two quotations are provided, the Three-Month LIBOR Rate for such Dividend Period will be the arithmetic mean (rounded upward if necessary, to the nearest 0.00001 of 1%) of those quotations. If fewer than two quotations are provided, the Three-Month LIBOR Rate for such Dividend Period will be the arithmetic mean (rounded upward if necessary, to the nearest 0.00001 of 1%) of the rates quoted at approximately 11:00 a.m. (New York City time) on that Dividend Determination Date for such Dividend Period by three nationally recognized banks in New York, New York selected by us, for loans in U.S. dollars to nationally recognized European banks (as selected by us), for a period of three months commencing on the first day of such Dividend Period. The rates quoted must be based on an amount that, in our discretion, is representative of a single transaction in U.S. dollars in that market at that time. If no quotation is provided as described above, then if a Calculation Agent has not been appointed at such time, we will appoint a Calculation Agent who shall, after consulting such sources as it deems comparable to any of the foregoing quotations or display page, or any such source as it deems reasonable from which to estimate LIBOR or any of the foregoing lending rates or display page, shall determine LIBOR for the second London Business Day (as defined herein) immediately preceding the first day of the applicable Dividend Period in its sole discretion. If the Calculation Agent is unable or unwilling to determine LIBOR as provided in the immediately preceding sentence, then LIBOR will be equal to Three-Month LIBOR for the then current Dividend Period, or, in the case of the first Dividend Period in the Floating Rate Period, the most recent dividend rate that would have been determined based on the last available Reuters Page LIBOR01 had the Floating Rate Period been applicable prior to the first Dividend Period in the Floating Rate Period.

Notwithstanding the foregoing, if we determine on the relevant Dividend Determination Date that LIBOR has been discontinued, then we will appoint a Calculation Agent and the Calculation Agent will consult with an investment bank of national standing to determine whether there is an industry accepted substitute or successor base rate to Three-Month LIBOR Rate. If, after such consultation, the Calculation Agent determines that there is an industry accepted substitute or successor base rate, the Calculation Agent shall use such substitute or successor base rate. In such case, the Calculation Agent in its sole discretion may (without implying a corresponding obligation to do so) also implement changes to the business day convention, the definition of business day, the Dividend Determination Date and any method for obtaining the substitute or successor base rate if such rate is unavailable on the relevant Business Day, in a manner that is consistent with industry accepted practices for such substitute or successor base rate. Unless the Calculation Agent determines that there is an industry accepted substitute or successor base rate as so provided above, the Calculation Agent will, in consultation with us, follow the steps specified in the second bullet point in the immediately preceding paragraph in order to determine Three-Month LIBOR Rate for the applicable Dividend Period.

Thanks 2WR…that was pretty exciting reading (not!), lol. I guess what i’m wondering — and i will ck individual prospectuses, is can the LIBOR replacement be less than zero, thereby lowering the overall adjusted yield. For preferreds where LIBOR or its replacement can’t be less than zero (if there are such) than a FTF with a good percentage rate added on to the LIBOR would still seem like a good purchase.

Franklin – again, more often than not, especially on the newer F/F issued based on a rate, the answer as to what happens if the setting rate goes negative can be found in the prospectus… Some will say if the base rate goes below zero we’ll treat it as if it was zero but others do not address the possibility at all.

Here are the type you have to be aware of especially if adjustment yield is low. This is a Citi one…Could be an ouchie….

….However, if fewer than three banks selected by the calculation agent to provide quotations are quoting as described above, three-month LIBOR for that dividend period will be the same as three-month LIBOR as determined for the previous dividend period or, in the case of the dividend period beginning on September 30, 2023, 0.2544%. The determination of three-month LIBOR for each relevant dividend period by the calculation agent will (in the absence of manifest error) be final and binding;

I think I presently only own two Libor issues. NSS which is already a live floater, and TECTP which has a 0% floor, so it could never go negative. The latter also has a high adjustment to help mitigate some. Its fall back provisions are at the end “suitable recognized replacement” or if that wont work “previous last reported Libor”.

FYI, the 3mo rate will stick around:

“The overnight, one-month, three-month, six-month, and 12-month USD LIBOR rates will continue to be published through June 30, 2023.”

(https://www.schwab.com/resource-center/insights/content/libors-slow-phase-out-continues)

And yet, IG issues are holding steady.

Grrrrr ……..

I’m guessing a buying opportunity that we are all waiting for will not arrive until the interest rate hikes actually start. It looks like the income market is looking at the end of the Fed bond buying with a big yawn.

Chances are that if inflation remains at >4%, and GDP slows to 3% or under and the 10 year goes to 2% – stagflation will hit and the fed will panic then do something less than beneficial. What that may be I don’t even want to think about.

Anyways

Happy New year to all

As you mentioned a possible capital loss for income investors I really wonder what will happen to REITs if rates truly do go up. There are some big names with yields less then 2% now days like MAA as an example. I am not sure why “some” people like buying some of these names at current valuations and what they actually pay out for the cash invested.

There’s a group of REITs that seem to be overvalued everyday yet never stop going higher….like apartments (AVB MAA), warehouses (PSB STAG EGP) and storage units (PSA CUBE). You can toss SAFE and LAND into that group too. Excluding those, I like to look at REITs like this, which seems to holds true since 2008. If the market goes up, REITs go down. If the market goes down, REITs go down. But that dividend keeps getting bigger and never stops being paid….unless you bought EPR for some reason lol.

DaddyDollars:

Not sure why you would say, “I like to look at REITs like this, which seems to hold true since 2008. If the market goes up, REITs go down. If the market goes down, REITs go down”

And REITs are up 36% in 2021, dramatically outperforming the S&P 500.

https://www.reit.com/news/blog/market-commentary/reit-average–historical-returns-vs-us-stocks

You must be riding the always in a bubble REITs that pay no dividend or you’re dumpster diving on saved from bankruptcy REITs that rebounded if you have REITs gaining 36% in 2021. Nothing on the top shelf with 4%+ yield gained anywhere near that.

DD:

Nope. All you had to do was buy the big REIT ETFs.

The largest REIT ETFs like VNQ and IYR are both up 36% YTD with dividends. But they both only yield a paltry 2%.

I bought VNQ in my wife’s IRA at the beginning of the year and it has had a tremendous run. Have recently started to take some profits.

DD — 4% yield is not really do-able on some of the bigger better REITS BUT in addition to VNQ’s rise , as pointed out by Rob, PSA is up 62% in past 12 months (with a 2.15% dividend) and extremely low beta. Other storage REITS have also done well and offer low beta. Self storage in the SouthWest (and other REIT types in that area) are growth stories for now with lower dividends than we get from prefereds but don’t throw out this entire asset class, which should also give a hedge against inflation. Disclosure: I own several.

DD, of the ~ 180 equity REITS that we track, the median year to date gain is 31.6%. VNQ, the largest equity REIT ETF which is market cap weighted is up 36.2%. One low yielding 2.2% REIT we own in nearly every account is EXR which is up 94.7%. They recently raised the dividend 25%. Long term, the best total returning REITS are generally ones with low dividend yield, but higher dividend growth rates. As opposed to high yielding ones that have low to zero dividend growth rates, aka “bond proxies.”

We are going to trim back the EXR holdings because they have become too high percentage of the overall portfolio. Kind of a rebalance. It is the best performing REIT we own.

You are correct that a few of the dogs have shined if you only look at 2021 results. If you look at 3 year or 5 year returns, they are generally negative

One thing I think is important is the fact interest rates have been low for so very long now it seems. We all know finding income is difficult so we keep going up the risk ladder. Good REITs have a reputation of being somewhat safe and a decent long term investment. An ETF of REITs is appealing for set it and forget it investors. In the past the yield was often a hardy 4% plus. Not bad.

Using VNQ as an example we can clearly see it’s yield is basically as low as it has ever been in it’s history basically. Currently sitting at 2.57%. Now some will say that when interest rates go up REITs could go down. I have seem information refuting that but I tend to agree with the basic premise. What I think is important is that the above yield clearly shows how much they have ran up in price.

One buys property to get a 5-12% cap rate on it. Hopefully your property goes up in value over time as well. One buys a REIT to get a 3-6% yield instead of owning the property yourself. It is suppose to be a source of income in my opinion. Now some REITs had phenomenal growth in the past. Cell tower, data center, warehouse, etc.. So those REITs always seem to have a low yield compared to others due to the fabulous growth of the company. But just how sustainable are those truly? Those cell tower REITs are now buying each other out since the growth is harder to come by. Datacenters REITs are merging or buying others out. In my book that means organic growth is more difficult then just buying other company’s cash flow.

Point is have we reached peak enthusiasm/growth/prices for many of these REITs which have been past darlings? Will possible new investors actually want some income if growth slows? If interest rates rise a full percent and IG fixed income starts paying 5% what exactly happens here? VNQ could fall from 115 per share to 85 pretty easily. Bring it down to a more historic yielding 3.5%. We are talking about a 20-25% drop in share price.

Now inflation should make their properties more valuable but REITs cannot just up and sell everything they have. Rent/lease prices should keep going up with inflation. But in the end are people buying these as growth companies or income or both? I think a time will come when many expect actual income again and no longer want the risk at these levels. That is pretty much my point. Too much risk for the income.

FC Said: “If interest rates rise a full percent and IG fixed income starts paying 5% what exactly happens here?”

FC, IG yields are about 2.3% currently. The largest IG ETF VCIT has a current 30 day yield of 2.27%. If IG yields climb up to 5.0%, that is more than a double. I agree with your point that equity REITS would get crushed. But I would also expect the broad stock market to get crushed. Of course, ALL and I mean ALL of our preferreds/baby/terms would get crushed, just like darn near all fixed income.

If my personal forecast called for 5% IG yields in say one or two years, I would be deciding on how to lighten up darn near all stocks, REITS, bonds, preferreds/babys/terms/kitchen sink. Many III’ers have commented they are moving to more babys/terms instead of preferreds for that possibility. We all know if we are buying basically any medium to high quality preferred in the last few years, we are playing with nitro and a pack of matches.

The question is how much probability to give that scenario? Each investor has to decide on their own. My guess is that many investors don’t have great or for that matter any models of what to expect IF IG rates increased that much.

We are already seeing the results of perceived interest rate risk, in the expected places we are all looking at here, but also in many meme tech names with operating losses. It isn’t pretty what happens to DCF models when the risk-free rate assumptions rise.

Like Gene Wilder in “The Producers.”

“No where to run . . . no where to hide . . .”

https://www.telegraph.co.uk/films/2016/08/30/gene-wilders-funniest-movie-scenes/

Tex,

I think exceptions to the ALL getting crushed by a 1% interest rate spike would be the past call issues that are still out there – AXS-E, ARGD, the Entergy issues, etc. Now I’m not saying they wouldn’t get their hair mussed, but I would expect the damage to be relatively light. Of course, holding those past call issues, you are pretty much forgoing any potential upside and there is the risk of loss on call, so as always there are trade-offs.

Tex, is it fair to compare IG bonds to common shares of reits when discussing IG yields? I was thinking more long the lines of IG preferred like PSA as an example. I should have been more clear and used the lingo correctly.

REITs, perhaps more than any other sector benefited from massive government intervention in response to the pandemic. Commercial businesses that should have gone under were propped up, workers who should have been laid off were paid to stay home, borrowers that should have gone broke were given forbearance, real property valuations that should have cratered went up. The true cost of all that intervention has yet to be tallied (estimates of $100B of outright fraud notwithstanding) but its almost certain to be a burden borne by our grandchildren.

Shouldn’t floating rate preferreds do well as rates go up….not just terms? Several floaters like CIM and NRZ still seem to be cheap for some reason.

3 of their 4 pfds (A,B,C) float to 3mo Libor. So some risk there if libor stops being quoted.