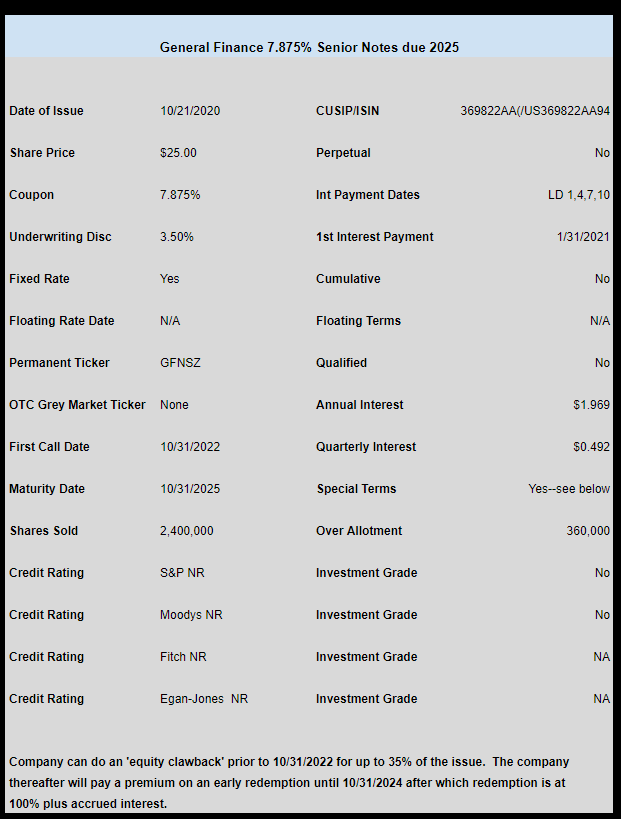

Container and storage lessor General Finance (GFN) has finally priced their new issue of baby bonds.

The issue priced at 7.875%. They will be selling 2.4 million baby bonds with another 360,000 available for over allotments.

The issue will be redeemable on 10/31/2025–the short maturity helped the company to garner a slightly lower coupon. Longer dated issues will have to pay a higher coupon.

The issue will first become redeemable on 10/31/2022 at 104.50% of liquidation value until 10/30/2023 and then 102.25% of liquidation value starting on 10/31/2023 until 10/31/2024 after which it is it is redeemable at 100%.

The company will be able to do a ‘equity clawback’ prior to 10/31/2022 for up to 35% of the bonds at 107.875% of liquidation value. The ‘equity clawback’ allows the company to sell equity to be used in redemption.

Of course all early redemptions include accrued interest.

The pricing term sheet can be read here.

The claw back feature on the new note is rare these days and is similar to a conversion clause…except there is no set share price or triggering mechanism for when the claw back is exercised. Adds an interesting level of complexity to the risk of holding these notes.

I’m sorry; I still don’t understand. What does the equity clawback feature say?

Thanks.

David.

It is posted at the top of the article

David–in a nutshell–they can redeem up to 35% of the issue prior to 10/31/2022 (1st call date) at 107.875% (plus accrued interest) if they issue equity (common stock–or preferred) and use the proceeds to redeem some of the debt.

Thanks.

My GFNSL redemption notification from Fido says full call . . .

D–they can use cash or their revolver to do a full call.

I’m fine either way, not sure about moving into the new one, will wait and see. I have a few GFNCP picked up last spring in mid-90s, may be enough exposure for me. Thanks to all.

“The company intends to use the net proceeds to redeem a portion of the $77.4M principal amount of its 8.125% Senior Notes due July 2021.”

They’re only able to drop the rate from 8.125% to 7.875% and raising only about 60 mill of 77.4 they owe. I’m still scratching my head over this. Considering the underwriting fees and any other expenses that may be associated with this offering, can someone explain the logic behind this move?

They want to push out their debt maturity schedule while the debt markets are hot. For a company like this, they have to roll debt when markets will let them. You don’t want to wait until the last minute. The small amount of the 2021 notes they are leaving outstanding won’t be a problem to roll even in an unforgiving market. They may also be able to pay it off with FCF or cash on hand.

When you are a small fish in the sea, the waves are crashing on you, and you are doing everything you can to keep your neck above the water… you pray that you can kick the can down the road. This is a great time to kick the can as rates are really low. They have a lot of debt and anything you can do to keep borrowing and extended the maturities, keeps your company alive.

Artemisa–the refi part is understandable since it matures in less than a year–the less than full redemption is puzzling. On the other hand they can likely still do a full refi if they want using cash or revolver.