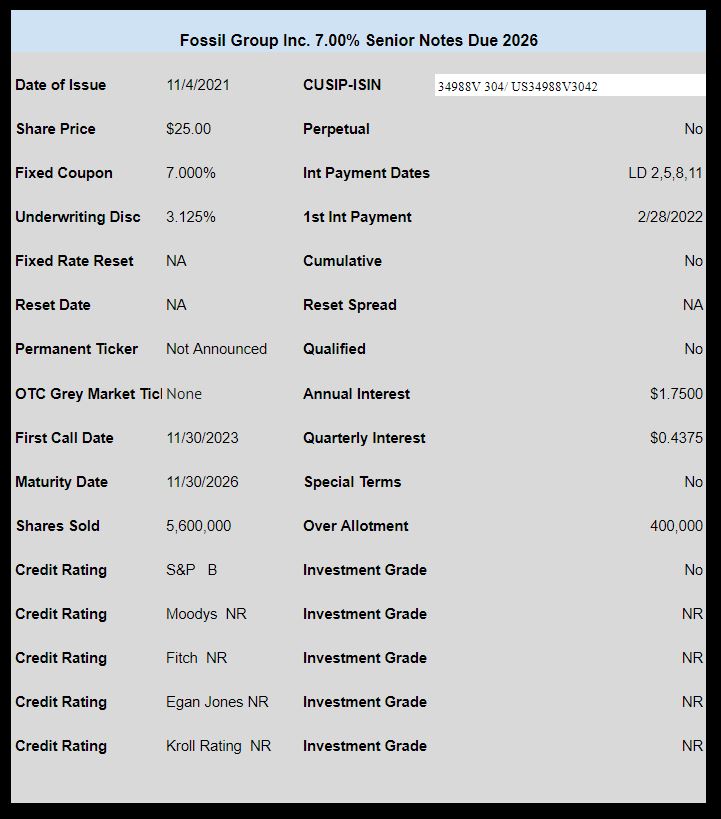

Fossil Group (FOSL) has priced the previously announced baby bond issue.

The issue prices at 7.00% for 5.6 million shares (bonds) with another 400,000 shares available for overallotments.

This issue is rated ‘B’ by Standard and Poors.

The bonds may be redeemed early beginning on 11/30/2023 at $25.50 until 11/29/2024, then on 11/30/2024 until 11/29/2025 at $25.25 then on 11/30/2025 until maturity on 11/30/2026.

The bonds may be redeemed prior to 11/30/2023 with payment of $25/share plus the greater of 1% or an amount determined based upon a treasury discount rate plus 50 basis points (see the prospectus for full details). Of course additionally all accrued but unpaid interest.

There will be no OTC trading on this issue since it is debt, although those desiring to acquire shares prior to exchange trading may call their brokers bond desk and inquire as to availability.

The pricing term sheet can be found here.

There was some demand on this name…I got cut back 40% on my allocation.

Thanks, Tim.

It actually states they can redeem (at $25.50 + accrued) BEFORE 11/30/23.

“Prior to November 30, 2023, the redemption price will be …”

Maybe I’m misunderstanding something …

Here’s the text from the FWP:

“We may redeem the Notes for cash in whole or in part at any time at our option. Prior to November 30, 2023, the redemption price will be $25.00 per $25.00 principal amount of Notes, plus a “make-whole” premium calculated at T + 50 bps, plus accrued and unpaid interest.”

Hi mbg–yes I noticed that–I am looking for the calculation of the ‘make whole’ premium’.

The way a normal make whole provision works means you’d calculate the YTM (or more likely the yield to first optional call) based on a price that would provide a yield equivalent of the comparable US Treas + 50BP… That would mean that if you used today as the day it was called under make whole (just to illustrate), the yield on a 2 year Treas is approx, .48%.. Tack on +50 to get to .98% and then calculate the dollar price and that will give you the call price if called today.. So in round numbers, if this were to be called today (obviously it’s not) it would be callable at around 28… So it’s always a sliding call price based on USTreas bond yield and the changing comparable issue to use as time decays to optional call date.

2wr–yes you are correct. I posted a short note above and folks will have to go to the prospectus to figure it out.

mbg–thanks. I read through the calculation for the pre 11/30/2023 redemption and posted a short recap–but folks will have to go to prospectus to read it for themselves.