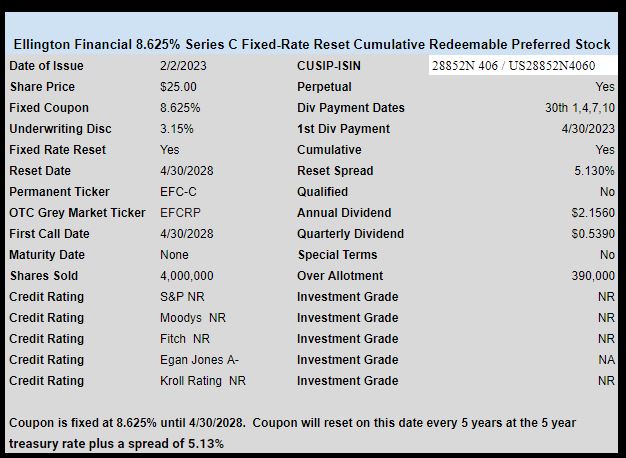

Below is the pricing information on the new Ellington Financial (EFC) fixed-rate reset perpetual preferred.

The issue should be trading on the OTC market today under ticker EFCRP.

The pricing term sheet can be found here.

7/25/2024

Our site runs on donations to keep it running for free. Please consider donating if you enjoy your experience here!

Below is the pricing information on the new Ellington Financial (EFC) fixed-rate reset perpetual preferred.

The issue should be trading on the OTC market today under ticker EFCRP.

The pricing term sheet can be found here.

Ellington did a Presentation to Debt & Preferred Equity Investors last November 2022, showing their portfolio as of 9/30/22. It shows 44% in “Residential Loans and REO and Retained Tranches” @ 7.7% yield and 28% in “Fixed Rate Agency Pools” @ 4.9%. They have other assets with higher yields, but the majority of their book are the two residential loan holdings. Then they go float a new preferred @ 8.625%.

What kind of borrower would pay 8.625% + a margin above that for Ellington to make a positive spread? To paraphrase Graucho: “I would never make a loan today to anyone having to pay 10.625%.” (Graucho’s actual quote was: “I Don’t Want to Belong to Any Club That Will Accept Me as a Member.” )

Through Q322, EFC lost 1.82/share and today it closed @ 13.91. Most of the loss was attributable to unrealized losses on their portfolio. You hold a lot of fixed interest rate paper and rates increase, book value goes down. Kind of like low coupon preferreds in 2022. On their low coupon paper, how many people do you know that are paying off their existing ~ 3% mortgages to take out a new one at 6.0% to 7.0%? Stated differently EFC is stuck holding most of the paper that is underwater to their cost.

Bottom line to me is that raising funds ~ 8.625% seems a little desperate.

We do not hold any EFC common/preferreds in any account, nor have any open buy/sell orders.

Link to EFC presentation:

https://www.ellingtonfinancial.com/static-files/ca08a79b-8ac7-4fd2-8a30-df44f40bbedd

Thanks Tex,

No interest in swimming today with the sharks. Seals are on the beach here in Calif. having pups and staying in colonies. Sharks just off shore looking for a newbie seal pup to wander into the water.

I have followed EFC for over 10 years and own the A’s and B’s. The decline in book value (and market price) is mostly related to mortgage spreads blowing out on all mortgage instruments (as well as high yield, etc). They hedge most of the interest risk. With rates moving as quickly as they did the hedge is not perfect. As it relates to the 8.65 C offering my belief is that they can invest the proceeds in very attractive returns and the offering makes sense for EFC, as opposed to issuing common below book value. The A’s move to floating in 10/24 and at todays rates would reset to 10% – which they might choose to call. The C issuance is positive to common holders and a negative to preferred holders as the total preferred outstanding verses common went up $100mm.

Fryman, yeah the one variable is where will interest rates go. But even if they start to come down, C seems to be overpriced in relation to A. Maybe I am missing something but I am not sure how you calculated 21 months for A to break even with C

Today you buy EFC-A for $2.45 a share less than C. You will make 81 cents more in dividends with C until 10/24 when A goes floating. So A would still be ahead by $1.64

And with a 5.169% kicker, LIBOR would have to fall under 3.5% for A to pay less than C after 10/24. Even if LIBOR falls to 2.5% it would take over 6 years to make up the $1.64

So the only conclusion I draw is A is underpriced and will need to rise a lot or C is overpriced in relation to A . I learned my lesson on AGNCL with this same scenario as I was focused more on locking in a higher rate longer term than the relative value of the sister issues to each other. But obviously you should do what you are comfortable with. Good luck

Mav – I just eye-balled that A would be making about 1% less than C for 21 months, then if Libor was at 4.8%, A would start paying about 1% more than C, therefore taking about 21 months to catch up. There is probably a lot wrong with that quicky calc!

I also took a hit with AGNCL. It came out at the worst time for skyrocketing rates and max doom and gloom, although it has come back nicely. Hopefully better times ahead! Thanks for the response.

Yeah, took some deft trading for me to turn AGNCL into a positive. Averaged way down . Sold some higher priced shares to capture some tax losses and used the proceeds to buy AGNCN before it went floating -and rose a lot generating some nice capital gains

So I am ahead on it all – but had to work too hard to do that, LOL

Anybody else having trouble buying this? TDA giving the following message:

“No opening transactions are allowed on securities affected by amendments to SEC Rule 15c2-11.”

I picked up a couple hundred on Fido at $24.56. Was easy to buy. They appear to be a reasonable mreit. This pref is paying a full point over the existing ones. I don’t plan on a long term hold. Seems low risk in the short term.

Schwab is showing it with quotes etc, but looks like you have to go to the desk for now.

Most buys/sells are 1000shs or more. A few at 200-300.

Now trading under EFCRP at about $24.55

Anyone have any opinions about EFC?

What is odd to me is that I paid quite a bit of attention to mreits during the covid crisis, I follow along with the more sturdy ones to keep an eye on things, I have holdings in a few mreits, but in the end I never discussed/read diddly squat about EFC. I know almost nothing about them. Even after I have read so much from Colorado on SA.. I cannot recall anything much about EFC. It is like they are truly an odd one out from the bunch from my own perspective.

I have owned a number of mReits and never have owned or followed EFC

Just looking at this, and learning a lesson from AGNCL, this is probably overpriced at $24.55 compared to EFC-A depending on where you think rates move

EFC-A is selling at $22.10 and pays $1.69 a year to yield 7..64%.

EFCRP is selling at $24.55 and pays $2.156 a year to yield 8.78%

However EFC-A floats starting 10/24 at 3 month libor + 5.169%

So you are earning 46.6 cents more a year for 21 months = 81 cents more till EFC-A goes floating at a higher rate yet you are paying $2.45 more to buy EFCRP

So unless you think rates crash in the next year and a half, if this follows the pattern of AGNCL when it was first issued, the price of EFCRP should fall more

Now I could be totally wrong, but I am not buying

In my opinion EFC is a high quality mreit. It is small so it is under the radar. Ellington Capital has been around for a long time and I believe manages about $10B. Their experience with mortgages is second to none. They were around in 1998, 2008, etc. EFC allocates significantly less capital to the leveraged agency space and much more capital to the mortgage credit space. They have protected book value much better than most alternative mreits, which is exactly what I want as a preferred investor. Insiders also own about 6% of the common. The B’s and A’s are cheaper than the C’s. B’s are less liquid than the A’s. The C’s are a nice piece of paper.

Mav- I like your thinking but I have my doubts if Libor will still be climbing in 21 months. Even it stays at the current 4.8%, it will take another 21 months for the A to break even with C. I own a lot of floaters but expect them to crater if rates start declining. Anyway, my crystal ball is fairly crappy so I will take a bird in the hand with the C. Good luck.

Theoretically, the floaters should hold their value if the spread is around market. In a world where rates come down sharply I would expect floaters to trade around $25, while for example the EFC C would move to a premium until the reset and then $25 at reset date (as long as the spread is market for the issuer).