Investors don’t know whether to buy or sell today–maybe some of both as the S&P500 is flat as a pancake.

I bought a nibble of the newer Lincoln National 9% preferred–more of a placeholder position — something to remind me to buy more if it passes due diligence. Looks like they have had giant write downs and maybe some drama in the C -Suite–regardless I need to dig deeper. Hopefully there issues are resolved so I can get a big chunk of this one next week–may have to reduce other positions to get it but it would be worth it I hope.

Today we had existing home sales announced as down 5.9% from the previous month–no giant surprise. This is a modest decline all things considered and I am surprised sales have been as good as they have been up to this point. But eventually the declines in the various housing data points will take a toll–i.e. house building and employment.

The 10 year treasury is up 4 basis points to 3.82%–trading up a few basis points and then down a few–that is how I like it–none of this up and down 10-20 basis points which scares the shix out of everyone.

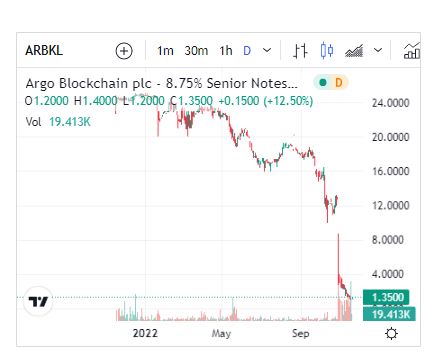

Under the filing of ‘glad I didn’t buy this’–Argo Blockchain 8.75% notes–a new issue almost exactly a year ago.

Has anyone else noticed the closed end fund TY preferred is in the $45 range? I started a small position. This one has always fascinated me because of its outsize coverage ratio (about 4,000%) but the price was always too high until now.

If you like this type of safety and are looking to pair it with shorter duration, you may consider looking at the Prologis preferred. A rare seller has been out at 54.75. Stripped out that is about 6.2% for mostly likely a call in 3 years as Prologis has half the 25 year old old 8.54% float bought out already. The less than 5 million payment obligation isnt even a speck out of their earnings. And of course its A rated debt is only about 13% of its capitalization.

Of course risk remains. The biggest two are: They chose not to redeem it and then you are stuck with a high quality 8.54% preferred. Or the other risk is Samuel Bankman-Fried becomes CEO.

I sell this bad boy when liquidity dries up and then buy it when it appears. I about have my cost basis driven down to par just in past several months alone. I bought 100 more at that above price yesterday (which is higher than my last 400) to retop the tank as exD is coming next month.

Grid, YTW is the 6.2% your talking about?

Yes, Charles. Quantum lists as 11/13/2026 as maturity but that is incorrect their SEC filings show it as redeemable by company at that time. But being it was issued when company was in infancy and they clearly dont use preferreds for their capitalization it has to be assumed as a goner then. But yes, back out the accrued of going exD in a month at last $54.75 ask, and your going to get about 6.2% with my eyeball math holding until that date.

Picked up a couple hundred shares of TY-P under $45. Cost basis will be less than 52 week low with upcoming dividend. Am looking to buy more as I think (hope) the current price range will turn out to be a good long-term entry point in long-term.

Since TY- is not 100% qualified dividend why not just buy something like PSA-L and squeak out a bit more yield? 5.55% versus slightly above 6% based on Fri pricing give or take a tiny bit. Maybe TY- is mostly qualified? I have never owned it and have not researched that angle. Anyone know?

I feel that 6% should be the goal for high IG rated preferred right now. The recent uptick in prices may very well revert giving chances to keep that goal of > 6% alive.

With that said.. TY- at 45 is not a bad buy to stick in the sock drawer. It is tempting if one is not looking to get every ounce of yield out of every single purchase.

The TY preferred shares are in my IRA so qualified/unqualified really isn’t an issue for me. Also, since it has been around since 1963, there’s a chance it will never be called (famous last words). And if it is called at $55, the capital gain will provide a consolation prize.

JV,

On a high volume down day, put in a bid below what is showing for 100 shares. If it hits, put in another 100 share order in. If it hits, keep moving the limit down until it doesn’t hit. Then you know where the floor is that the sellers are willing to let go. I picked up 500 shares for my wife’s IRA this way.

Tim, you can add Greenidge Generation GREEL to your preferreds of note. I have posted about it several times, but it keeps finding ways to fall. It is a $25 par, 8.5% baby bond maturing 10/31/26. It IPO’ed one year ago but has been struggling recently. Take a look at a one year chart. Looks like a Grid ski slope to me. Today it decided to fall another 25% from 1.20 to 0.90. Very impressive to go from ~25.0 to 0.90 in the first year after IPO’ing. Takes a special kind of business, management AND underwriters to pull that off. . .

Gee, talk about outperformance, it took OTRKP two years to reach that kind of level…

2WR, do you think is there any hope that OTRKP will reinstate dividends or bankrupcy is more likely in the near future?

Don’t reallly have a strong or informed opinion but the market sure does… no

MFZ, I looked at the company and found some unfortunate highlights:

Revenue for the third quarter of 2022 was $2.8 million, representing an 85% decrease compared to the same period in 2021.

Operating loss for the third quarter of 2022 was $(11.1) million compared to an operating loss of $(5.5) million for the same period in 2021.

Adjusted EBITDA for the third quarter of 2022 was $(7.7) million compared to adjusted EBITDA of $(1.7) million for the same period in 2021.

Net loss for the third quarter of 2022 was $(12.8) million, or an $(0.62) diluted net loss per common share (after deduction for undeclared preferred stock dividends), compared to net loss of $(7.9) million, or a $(0.54) diluted net loss per common share (after deduction for declared and undeclared preferred stock dividends) for the same period in 2021.

Non-GAAP net loss for the third quarter of 2022 was $(9.4) million, or a $(0.48) non-GAAP diluted net loss per common share (after deduction for undeclared preferred stock dividends), compared to non-GAAP net loss of $(4.5) million, or a $(0.35) non-GAAP diluted net loss per common share (after deduction for declared and undeclared preferred stock dividends) for the same period in 2021.

You definitely should call the company and try to speak to the CFO or at the very least the Investor Relations Department and see what they say.

Wishing you the very best, Azure

Thanks Azure for the info. and thanks to 2WR as well. I have already sold for tax loss purposes. All the best.

On these quiet days I make a few trades just to prove I’m alive. Sold a couple shares of issues that held up after the rally. Shifted a little from float to fixed as the high rates may already be priced in. Unless you belive Powell”s 7% scare.

I got a plan, its just still a bit ambiguous to me, ha. I bought a lot of long dated IG bond market debt last month or so, so Im left having some self directed liberties to play short end. Although I exited last month,I bought back a full position of NSS past couple days. Just too tempting in $24.20s and a stripped out eyeballed ~11.3% or so. And at present Libor that is stripping out to around 12% and rising. Although no company is more successful at over promising and under delivering, they still have common covered by 2x, and will be zeroing out that 12 or 13% private placement ahead of schedule they announced. Albeit by cheating a bit with the lower interest rate revolver being used some though.

I added to NSS today as well around 24.25. A friend’s husband is an EVP down there and she never sees him, wants him to retire, they are very busy these days! Bea

I was thinking about you, Bea on this as I also knew it was on your stock mantle also. The underlying preferreds have been stable probably from fast approaching exD date. NSS will get its chance to move next month.

Grid, in NuStar’s latest 10-Q, https://investor.nustarenergy.com/static-files/b01af078-b1d9-4d6e-a684-44982f55b1e2, I see that NSS is mentioned as ‘Subordinated Notes, 9.2% as of September 30, 2022,” with a balance of $402.5M outstanding.

a. Since the original issue was $350M (per the prospectus at https://www.sec.gov/Archives/edgar/data/1110805/000104746913000236/a2212471z424b5.htm), I assume they must have sold $52.5M more of these notes at some point?

b. The current yield is 10.813%, per https://investor.nustarenergy.com/debt-information, and based on current 3M LIBOR will be higher when they reset it on 16 jan. Admittedly, this issue represents only 13% of their current LTD and the 2043 maturity is a long way off. Still, any idea why they aren’t calling these notes?

Bur its been $402 since I can remember and that is a long time. I suspect the rest were “greenshoed” by underwriters when it was first issued. The 10.8% is stated as off par price $25, so that is how the real current purchased price yield is higher, plus when you back out the accrued part of this cycle the yield is even higher.

Here is the reason why they arent called. Being they got into trouble with an ill fated asphalt business and a few other things over the years, they had to throw some newspapers over the dog doo doo to hide the stink. NSS, the $25 issued preferreds, and a private placed preferred were the newspapers. The senior lenders have all waived NSS as being considered debt, so its just being treated as a preferred and makes their debt coverage ratios look better. So its going nowhere. Their focus is knocking out the onerous private placed preferred. They recently announced an acceleration in being able to get it taken out…..

We’re now in discussions with the holders to repurchase as much as one-third of the Series D by the end of this year and we plan to redeem another third in 2023 and complete the redemption in 2024 several years ahead of schedule.

This redemption is another important step in our ongoing optimization which will meaningfully increase our free cash flow over the next few years. And while we now plan to move up our schedule we’re targeting holding our debt metric down around four times.

Makes sense…. Greenshoe is normally 15% of the original issue size and 350 x 1.15 = 402.5. And as notes, there’s no K-1 right?

Yes, for all practicalities, the only thing “debt” about this is the interest tax treatment. Everything else about it from senior creditors position, to the 0%-10% recovery in an “adverse event” (Fitch assessment awhile back) reeks of it being a preferred. But then again, you can largely say that about any subordinated debt from any company.

Whoa Nelly, I see now: the Series D rate is currently 10.75%, and goes to 13.75% beginning September 2024. Yeah I guess they’d want to scrape *that* s**t off their shoes… Thanks for the enlightenment, Grid.

And now that I’m looking again at their debt, how on earth did NSS qualify to issue GO Zone bonds? I thought those were for Katrina damage…

I like the cash flow coverage for this spec but it worries me that NS’ operating income has failed to improve over the last five quarters when the operating income of most other MLP’s has stepped up.

Bought a HD 2/15/44 BOND yields 5.3% last week.

Safer than the common which is all over the place.

IG bonds are a bargain. I’ll be dead before it’s called. More good news.

Same. Half the stuff I bought last month was IG bonds. I saw the prices & yields of baa2-A3 bonds and loaded up on 2040-50 maturities. If we can get the fed rate back to near 0, and the bonds back to 2021-early 2022 prices, then I’ll have some juicy 40-60% capital gains. In the meantime, 6.5-7.5% interest and not stressing… unless, 1929, 70s inflation calls, or UST liquidity issues that crash the entire system. Even then. I felt like these were good prices for companies like Citi, Lowes, Welltower, BoA, WF, Schwab, HP, OKE, Halliburton, and it would be hard to beat myself up over any unforeseen missteps.

I know what you mean. Boring day when there are no trades. to be made. But better to be patient than not. That said I did buy a very small amount of CHSCN today because I was bored. And I am glad I got my LNCDL shares two days ago at $26.01 and $26.03 after seeing the run up the last two days.