The S&P 500 opened last Monday at 3258, after closing the Friday before at 3338 and fell as low as 2856 on Friday before launching a fairly furious rally the last 30 minutes of Friday to close the week at 2954–a weekly loss of 385 points.

The 10 year treasury closed the week 1.12%, this is easily a record low.

Amazingly the Fed Balance Sheet fell by $13 Billion as no additional liquidity was added via repo operations or via QE (quantative easing) purchases.

Last week we had just 1 new income issue sold.

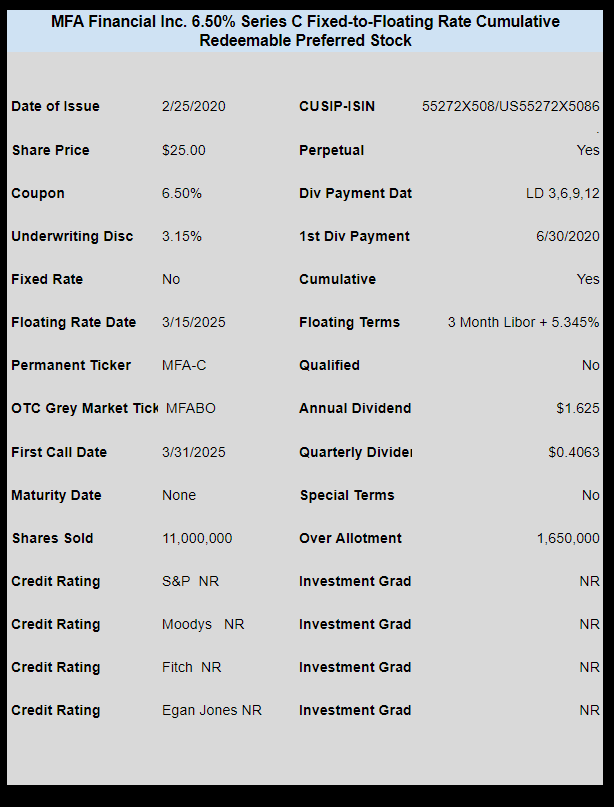

mREIT MFA Financial (MFA) sold a new issue of fixed-to-floating rate perpetual preferred with an intial fixed rate coupon of 6.50%. The issue is trading on the OTC Grey market now and closed Friday at $24.22.

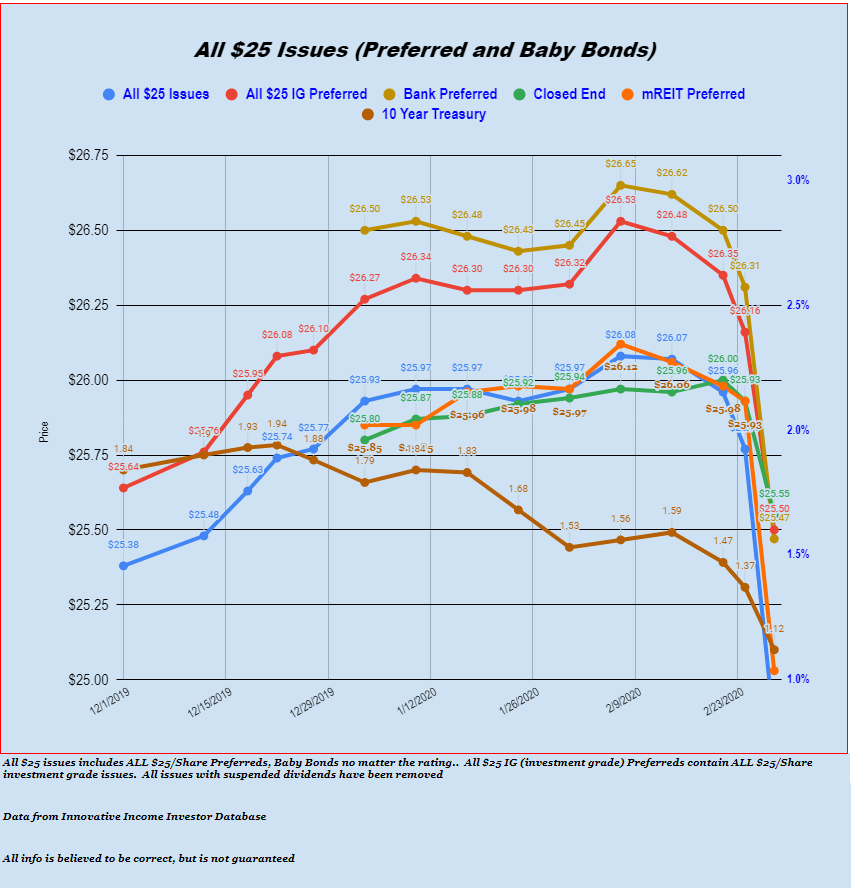

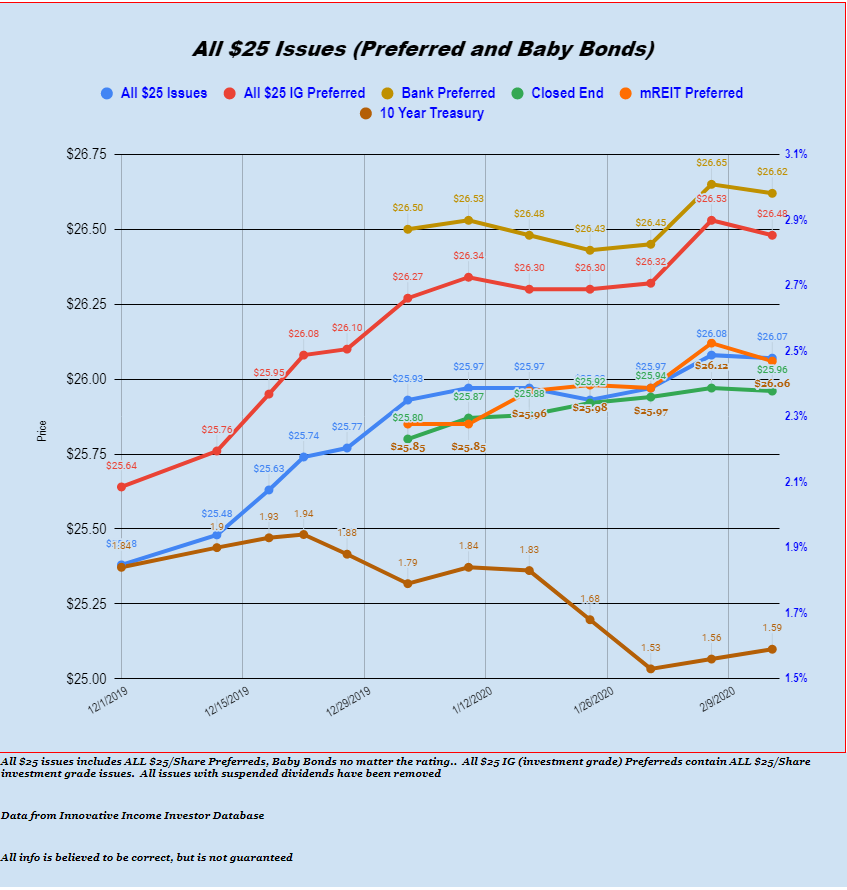

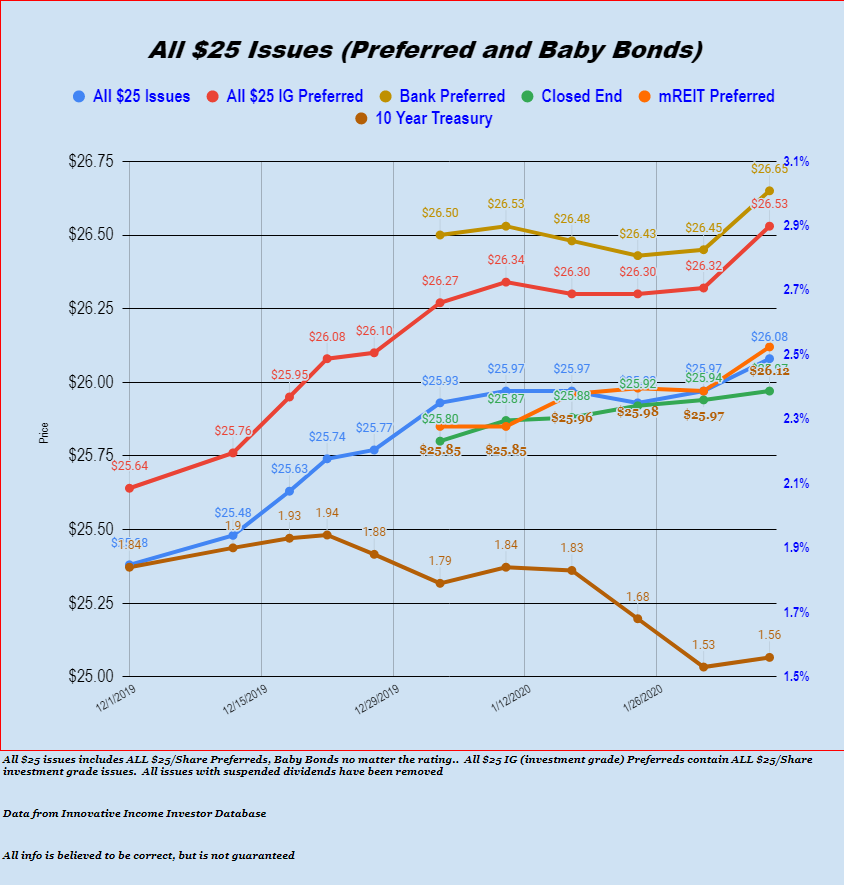

The average $25/shares issue lost 79 cents for the entire week. Investment grade preferred were off 66 cents. The chart below is truly ugly–most of the losses were incurred on Thursday and Friday.

This is abbreviated as the second outage on the website in 2 days makes it kind of irrelevant.

It looks like the week is going to start off with a bang as the corona virus spreads and is threatening to disrupt global economies in a big way.

The S&P futures are down between 2 and 3% and for the first time in quite a while stock movements to the downside should be getting everyone’s attention. Oil is down by $2 while gold is spiking up by $35.

We never advocate making rash moves (i.e. buying or selling) during these times of big equity moves–let’s sit back and observe the morning and see how it shakes out. There are high odds that most income securities will be just fine this morning–although we could be surprised.

Last week the S&P500 opened last week (which was a short holiday week) at 3369, hitting a low of 3328 on Friday and closing the week down 3338 off about 1% on the week.

The 10 year treasury has moved lower to closed last week at 1.47% after opening the week at 1.54% and hitting a high of 1.59%. Obviously global investors are piling into the safety of government debt as the corona virus spreads. This is in the face of the Fed slowly reducing liquidity–I guess the Fed will now reverse course in the face of falling equities. The 10 year treasury is now at 1.37%–near record lows.

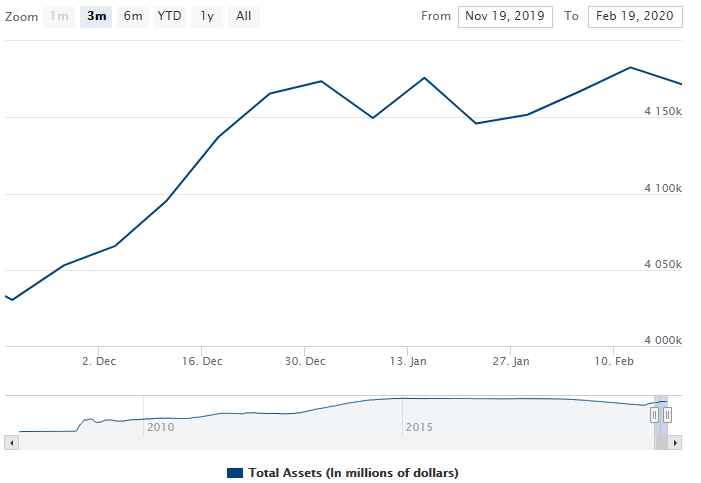

The Fed balance sheet fell by $11 billion last week which continues to keep the balance sheet flattish for this entire year.

Last week we had only 2 new income issues sold.

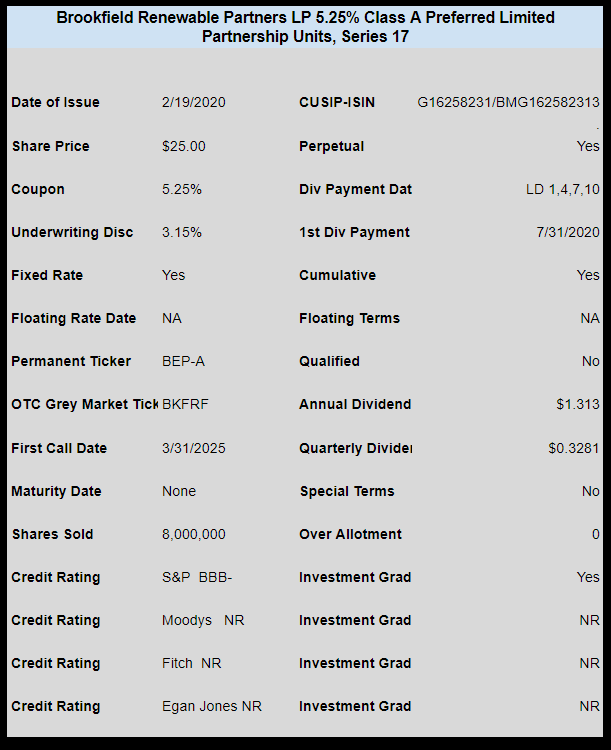

Brookfield Renewable Partners LP (BEP) priced a new perpetual preferred unit offering with a meager 5.25% coupon. The issue is trading under OTC temporary ticker BKFRF. The issue opened for trading around $25.39 and is now at $25.80.

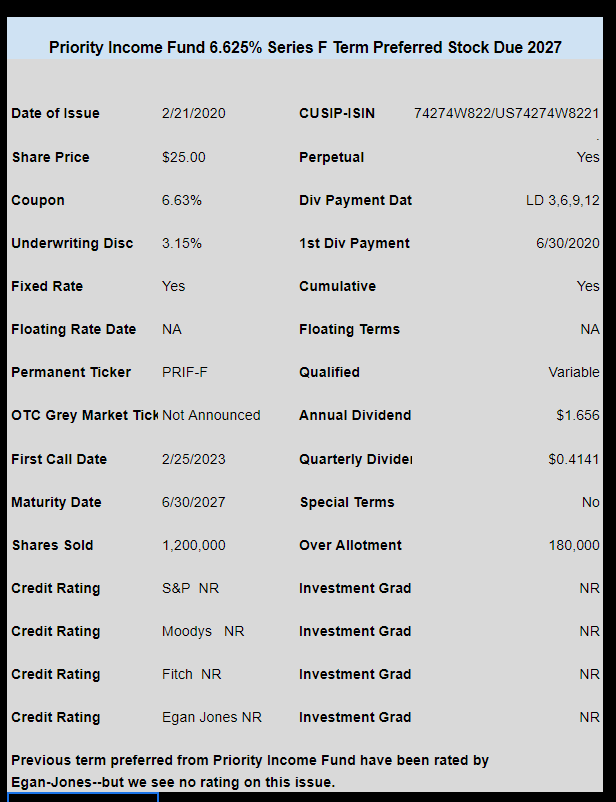

Priority Income Fund (non traded) priced a new issue of term preferred (PRIF-F) with a coupon of 6.625%. The issue is trading under OTC temporary ticker of PRYFP and last traded at $24.60.

The S&P500 opened the week at 3318 and closed the week 2% higher (of course) at 3380. The 10 year treasury started off at 1.57% and ended the week at 1.59%, although it was as high as 1.64% during the week.

The Fed Balance Sheet grew by $16 billion last week as the overall assets carried by the Fed remains flat over the last 8-9 weeks. The Fed had previously announced a reduced $5 billion weekly repo facility from mid January to mid February–they have now announced another $5 billion reduction starting in the 1st week of March. You can see the repo plans here.

The fact of the matter is that with the flattish balance sheet the last 2 months something has to give–we are now in very dangerous territory as the government debt continues to grow and the Fed will have to monetize the debt–with falling repo targets they will have to ramp up purchases of bonds and mortgage securities.

We are in significant danger right now of an INTEREST RATE SPIKE if the Fed doesn’t step in. We’ll just have to see what shakes out.

Last week we had a bunch of new income issues announced.

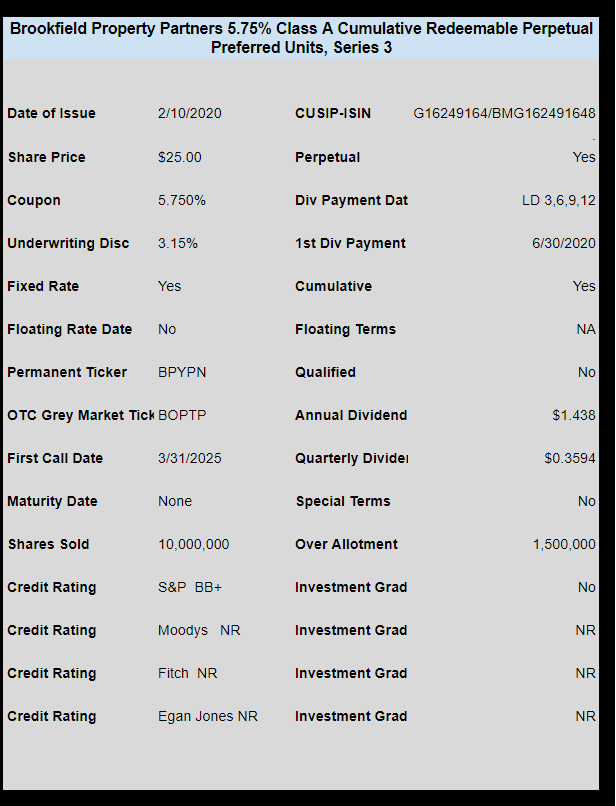

We started the week off with the pricing of a new perpetual preferred from Brookfield Property Partners (BPY). The issue is trading under OTC ticker BOPTP and last priced at $25.37.

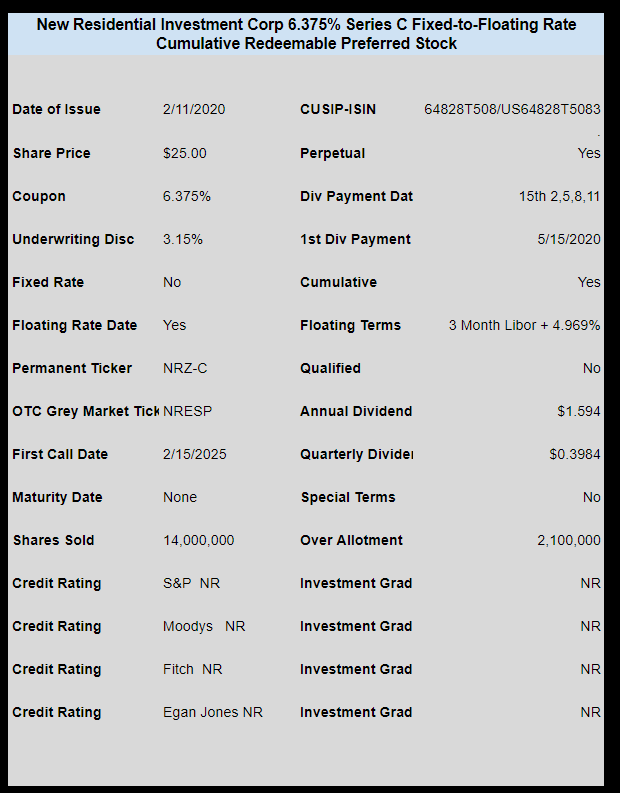

mREIT New Residential Investment (NRZ) sold a new fixed-to-floating perpetual preferred. The issue is trading under OTC temporary ticker NRESP and last traded at $24.81

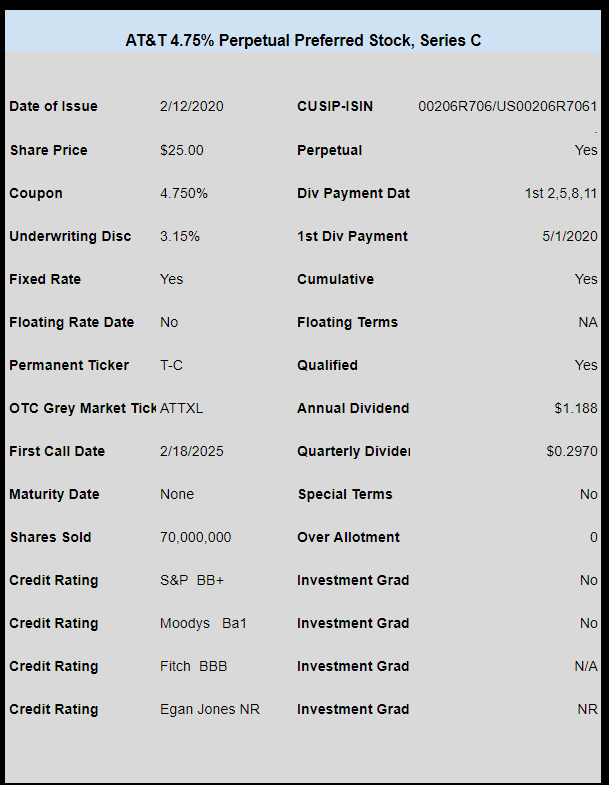

Telecom giant AT&T (T) announced a new perpetual preferred with a coupon of 4.75%. The issue is trading under OTC ticker ATTXL and last traded at $25.20

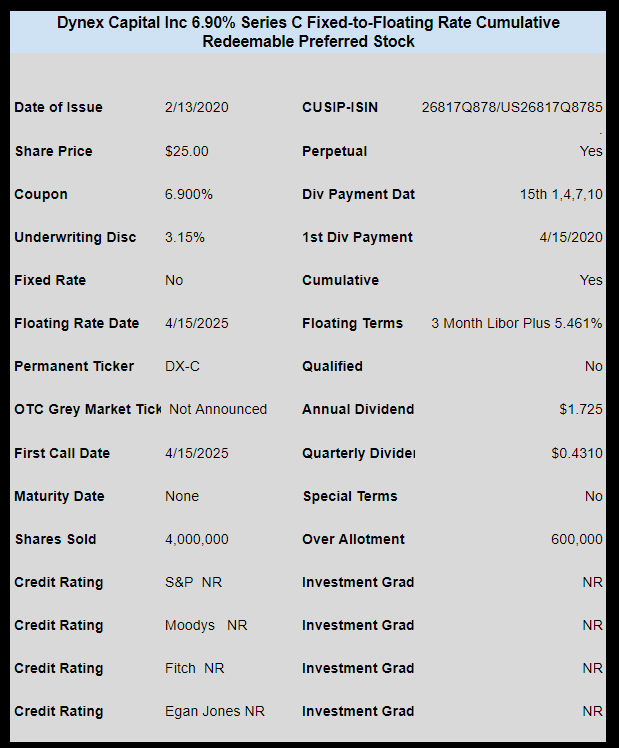

mREIT Dynex Capital (DX) sold a new fixed-to-floating rate preferred. The issue is trading under OTC ticker DXPBN and last traded at $24.95.

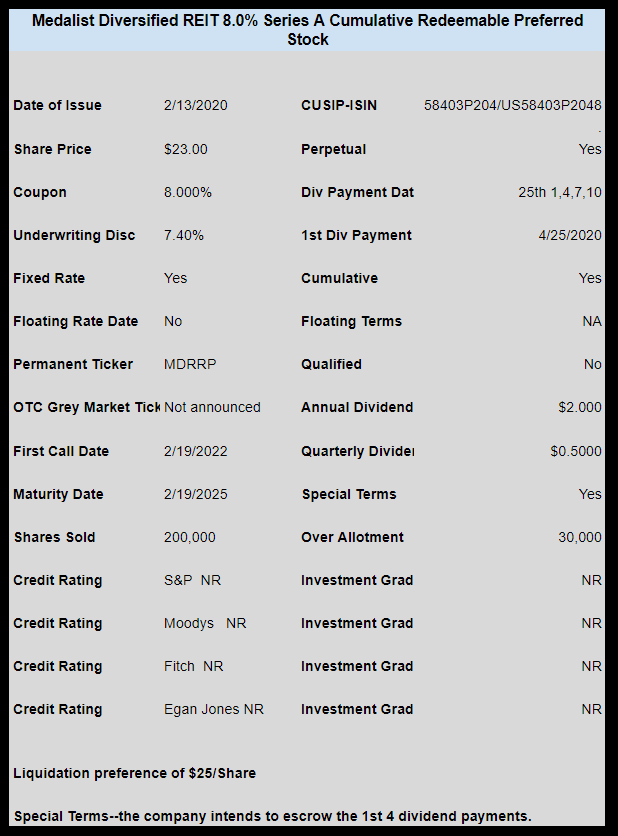

Lastly Medalist Diversified REIT (MDRR) sold a new preferred with a mandatory redemption in 2025. This issue came to market at $23 but has a liquidation preference of $25. The issue is trading on the NASDAQ and last traded at $20.56.

The average $25 preferred and baby bond moved by just 1 cent–lower last week. Banking too a nickel hit while the shipping issues (not in the chart) bounded back by 16 cents.

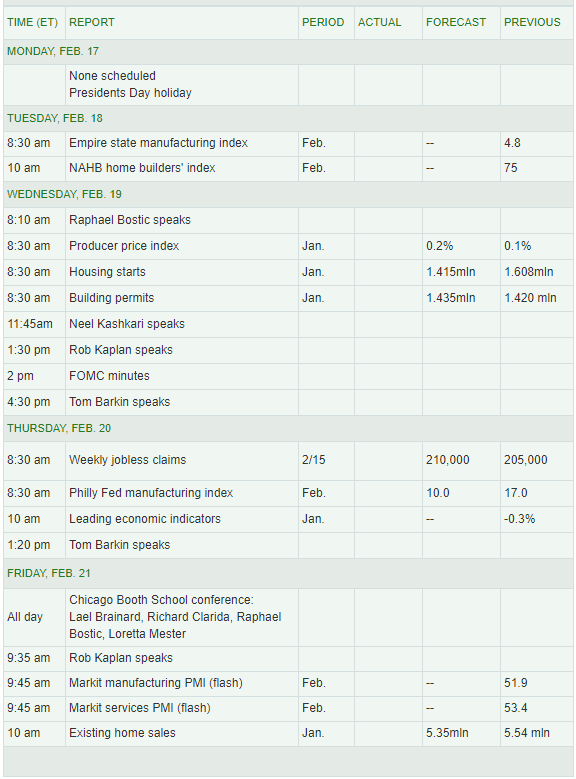

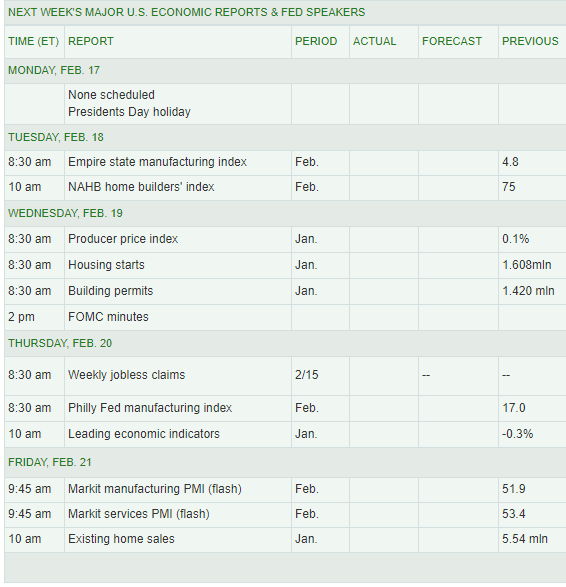

Below is the economic calendar for the week. All in all there isn’t likely much here that will move markets. The FOMC minutes are released on Wednesday, leading indicators on Thursday and PMI (purchasing managers index). While I am starting to believe more and more that the corona virus WILL start affecting economic numbers it may be too soon to see those showing up in any releases.

Here we go–a new week–what does it have in store for us?

As noted by Fabrib we kick the week off with REIT Simon Properties Group (SPG) announcing a buy of Taubman Centers (TCO). TCO has 2 preferred issues outstanding which can be seen here. Both are now callable and trading quite a bit above $25. I haven’t looked yet to see what the terms of the deal are yet–and they probably aren’t announced yet.

Last week the stock markets had strong gains–party on I guess. The S&P500 opened the week at 3236 and closed the week at 3328–about 3% higher.

The 10 year treasury opened the week at 1.56% and closed the week at 1.56%, although it hit 1.65% mid week. Obviously the blowout employment numbers were outweighed by the corona virus and the slowing of wage growth in employment.

The Fed balance sheet grew by $15 billion last week–continuing a trend of less than expected stimulus. The balance sheet remains at levels equal to the end of December.

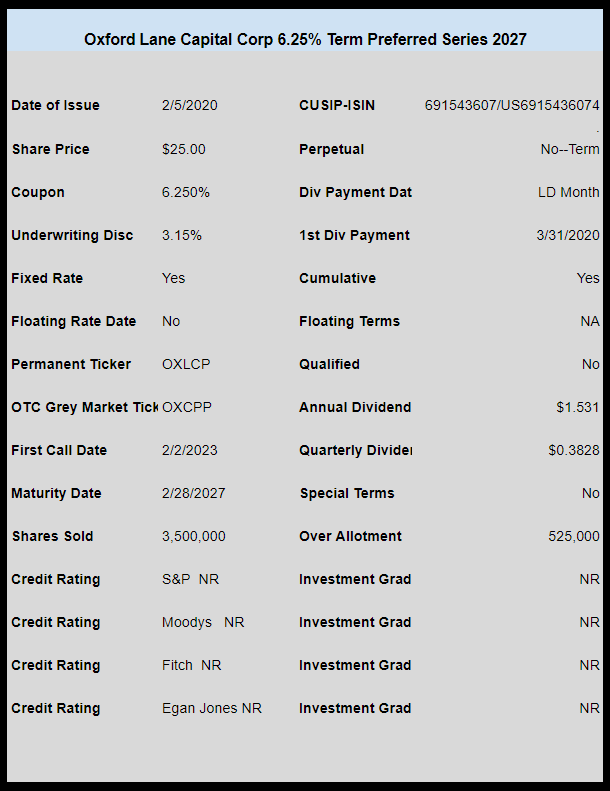

Last week we had 1 new income issue sold and that was from CLO holder Oxford Lane Capital (OXLC). The issue is trading on the OTC Grey Market now under ticker OXCPP and last traded at $24.81.

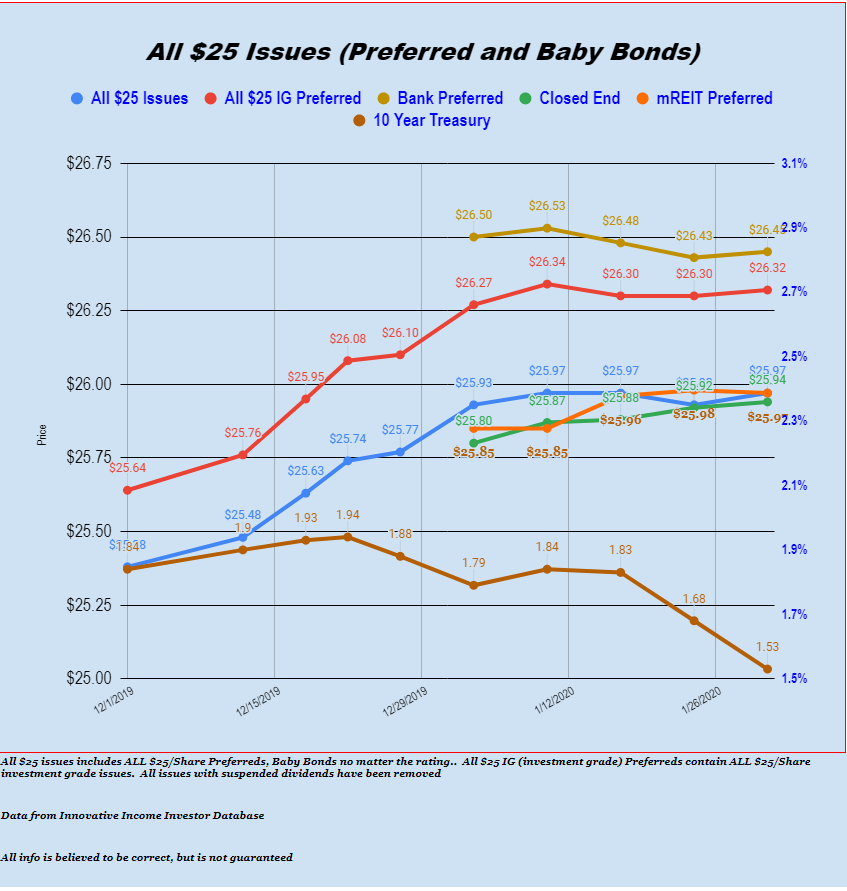

$25/share preferreds and baby bonds remain strong with a weekly overall gain of 8 cents with investment grade preferreds being very strong with a weekly gain of 17 cents with banking preferreds garnering a 15 cent gain. Shipping preferreds were down 46 cents.

Below is the economic calendar for the coming week.

I can’t wait to get this week started. The stock market was a bit soft last week for whatever reason–personally I think the corona virus was a good excuse to sell stocks down–they had gotten way ahead of themselves at values that were historically very high.

This in not to say the the corona virus isn’t potentially very serious–because I think it is, but wouldn’t the stock market have been off 10% or 15% or more if the marketplace actually thought the virus was going to cause a recession? Really with the S&P500 closing at 3225 after opening the week at 3247 can we say this drop of less than 1% in the week is a significant move? I don’t think so. Sure the market has dropped 3% from the record highs–but really -just 3% lower–big deal. It is only a big deal in the context of what might follow.

The 10 year treasury dropped to close last week at 1.52% after opening the week at 1.61%. After trading in the range of 1.80% to 1.95% late in 2019 we are now seeing trading at levels last seen in September. What this portends is for others to figure out.

In the end I never try to seriously predict economic activity–why waste the time? There are plenty of highly paid people to get the numbers of wrong. On the other hand I tailor my investing to what I think is occurring–for now that is simply uncertainty–keeping some dry powder and staying in shorter maturities when possible.

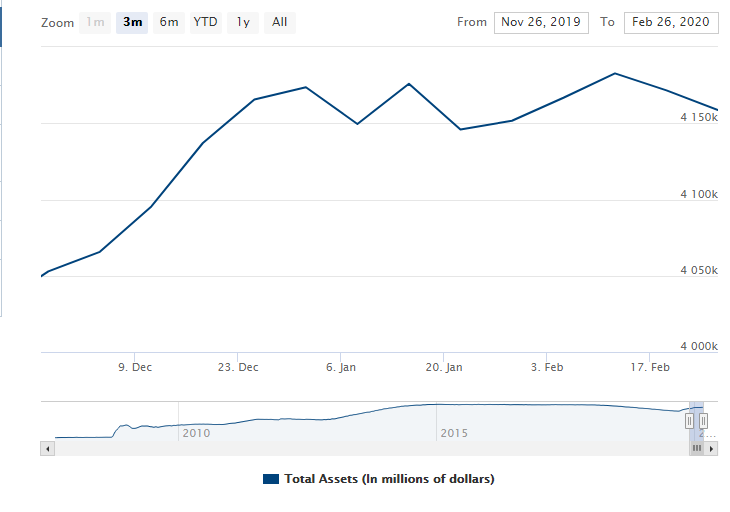

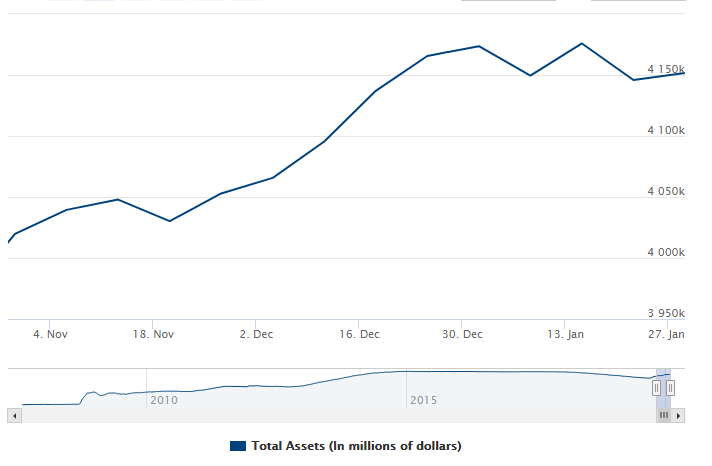

The Fed Balance Sheet grew by a measly $6 billion last week and if one didn’t think otherwise you might believe that the Fed was taking away the ‘punch bowl’. As you can see below Fed assets have not grown in 6 weeks–they are at about the same level as mid December. Maybe the stock market fall is related to reduced liquidity.

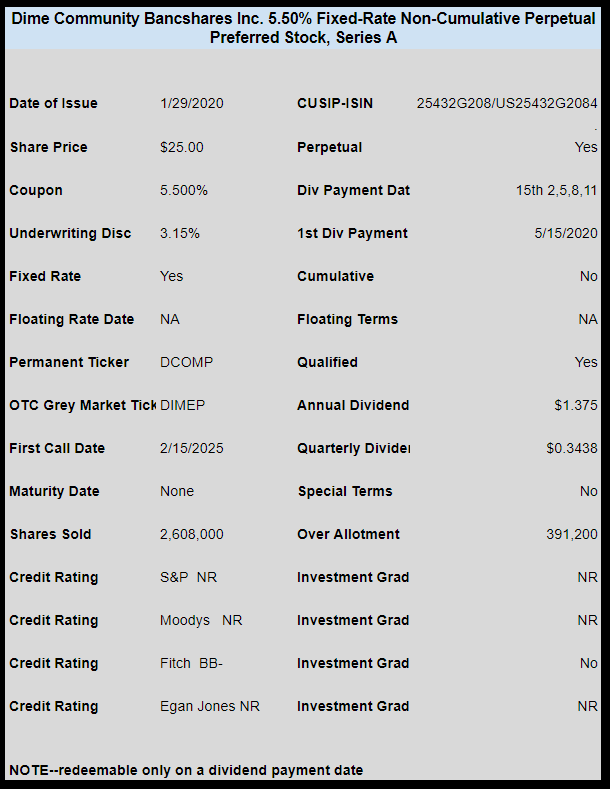

Last week we had 1 new income issue sold. This was a perpetual preferred from small community banker Dime Community Bancshares. The shares are trading on the OTC Grey Market right now and opened for trading at $25.40 and now are at $25.68.

The average share of $25 preferred and baby bond did rise 3 cents last week, but most sectors were essentially flat. We do note that shipping preferreds and baby bonds were down about a dime.

The average current yield on $25/shares issues of preferred stocks and baby bonds stands at 6.28%, while the current average yield to worst is around 3.21%. We will chart this data when we have more data recorded in the future.