It is strange how we can go from a fairly large drop in the futures markets overnight because of Iranian missile attacks to a market that is acting remarkably calm.

With the killing of the Iranian general last week I thought that we would see some short term market weakness, followed by a nervous flat market. With missiles flying last night from Iran I thought ‘oh no’ this could get much worse than I expected.

Last night I did take a peek at the futures markets and saw they were down a couple hundred down points–all things considered not a big deal-and by market opening today we were flat and interest rates remained flat in the 1.81% area.

So, for now, we are back to semi-normal conditions. Of course this will be hanging over our heads for another week and it will temper moves in stocks and interest rates.

We do have the employment report being released on Friday . The forecast is for a modest 160,000 new jobs being created–certainly if this number is close we won’t see interest rate reactions–but we shall see.

Sometimes we hesitate even posting items like these–most of the times they turn out to be meaningless.

On the other hand better to post than anyone get a surprise.

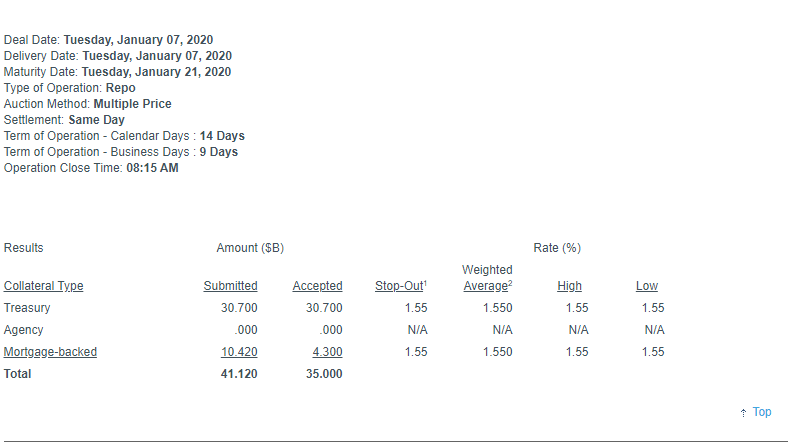

1st off I am not an expert on repurchase agreements that the Federal Reserve executes, but I am knowledgeable enough to know that the FED is now–and has been, executing repurchase agreements with the ‘primary’ dealers of government debt since September. The Fed takes government securities (including agency backed mortgages) as collateral and lends the institution money so they have enough liquidity to serve their customers.

The primary dealers are typically large banks and securities companies which are trading counterparties for the Federal Reserve. They are expected to ‘make markets’ in government securities. They generally must make bids for government debt at auctions. This is all done to implement monetary policy.

With that said the New York Fed releases a monthly forecast of open market REPO operations.

The Fed last released a monthly forecast on 12/12/2019 which can be seen here. This forecast covers the period ending 1/14/2020–thus we should see a new forecast soon–the end of this week or Monday.

Here’s the problem. When the REPO facility was started back in September it was in reaction to a huge spike in overnight lending rates–they spiked as high as 8-10% as liquidity was unavailable for those needing money. Supposedly the liquidity was needed for tax payments and for settlements of U.S. government securities–it was implied this was a relatively short term problem.

GUESS WHAT-the issue seems to go on and on and whether this liquidity crunch will improve is anyones guess.

Today primary dealers offered $41 billion in collateral for a 14 day REPO, but the Fed only accepted $35 billion–this means less liquidity was supplied than the market thought it needed.

The question is – is the Fed going to try to withdraw liquidity? What will their next forecast show?

I will make my own forecast–the REPO will continue indefinitely. Additionally the size of the Fed Balance Sheet will continue to grow all throughout the year–there is no choice–the U.S. is going to run another $1 trillion dollar deficit.

It was an interesting day of trading–although not really much movement after the 1st hour or so–at least in stocks.

The 10 year treasury closed at 1.79%, which is a good bit lower than the 1.87% to 1.94% range we had been trading in for the last couple of weeks. Obviously this is a move to safety after the killing of Iranian General Soleimani.

I have read numerous articles on the affect this will have on the market–and unfortunately they are all pure speculation and mean almost nothing. But this being said a rational person needs to look over their portfolio and see where they might be vulnerable.

The obvious place to be looking for vulnerabilities is in the energy and shipping sectors. If I was a betting person I would expect Iran to attack either oil fields in Saudi Arabia or ships in the Straits of Hormuz in retaliation. I’m not telling anyone reading this anything at all–we all know about these obvious weaknesses. It is the unknown areas that will cause the real issues.

For now I have mostly ‘sat on my hands’. History tells us that this will not be meaningful to income investors–BUT one never knows–if we knew we would have our own reality TV show reading minds and making predictions.

Investors always need to do what makes them able to sleep at night. If that means lightening up for a few weeks, so be it. I think everyone on this website knows that there are no right or wrong answers–just the answer that works for you.

While there was a time when I would react to global war type situations, time and time again, they have meant little to income investors.

The situation in Baghdad yesterday (the killing of the top Iranian general) brings out a ‘knee jerk’ reaction with stocks falling a bit and interest rates moving lower in a small flight to safety–but unless we see some kind of major escalation in the tensions it will be just a ‘knee jerk’ reaction.

We could see a minor move higher in the quality (i.e. Public Storage) low coupon preferreds as a small amount of excess buying pressure comes in–but likely not anything more than that.

So, for now, there is not a reason to get nervous on your holdings–let’s watch for potential escalations.

I left the office for 90 minutes today and was really pretty shocked to see a near 1% gain in equities–so indexes were already pretty darned high–so let’s stretch them further I guess. Oh well I don’t buy common stock any longer so it doesn’t really matter to me–but still WOW.

The good part of today is income issues also took a nice pop–why? There is a lot of money chasing around after yield-it is as simply as that–there simply is no other explanation.

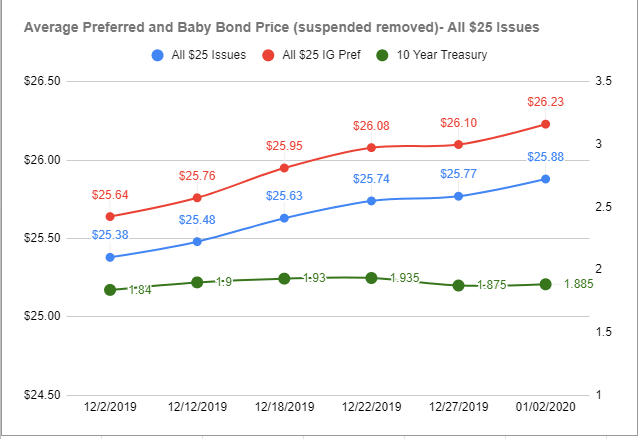

I thought maybe we had seen the peak in pricing of preferreds and baby bonds–but certainly the ‘average’ prices show we are continuing to see gains.

It was interesting to see interest rates tic 4 basis points lower to 1.88%–lower rates just don’t jib with skyrocketing stock prices. Oh well–what’s new.

It will be good to get to next Monday, when we get back to normal–folks will be back from vacation and we will start to see some new income issues once again. But for now Santa just keeps on giving.