I left the office for 90 minutes today and was really pretty shocked to see a near 1% gain in equities–so indexes were already pretty darned high–so let’s stretch them further I guess. Oh well I don’t buy common stock any longer so it doesn’t really matter to me–but still WOW.

The good part of today is income issues also took a nice pop–why? There is a lot of money chasing around after yield-it is as simply as that–there simply is no other explanation.

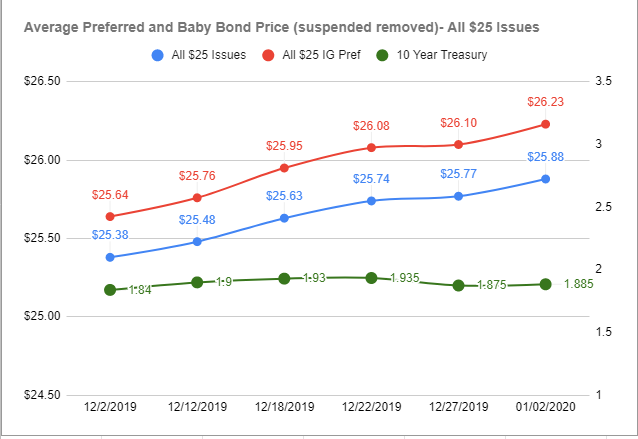

I thought maybe we had seen the peak in pricing of preferreds and baby bonds–but certainly the ‘average’ prices show we are continuing to see gains.

It was interesting to see interest rates tic 4 basis points lower to 1.88%–lower rates just don’t jib with skyrocketing stock prices. Oh well–what’s new.

It will be good to get to next Monday, when we get back to normal–folks will be back from vacation and we will start to see some new income issues once again. But for now Santa just keeps on giving.