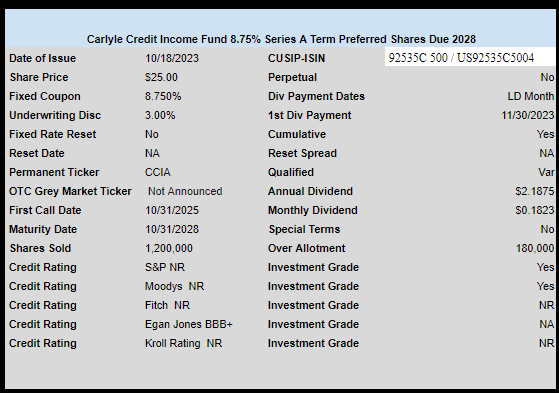

Closed end fund (CEF) Carlyle Credit Income Fund (CCIF) has priced their new issue of term preferred stock.

The pricing is 8.75%–a tasty coupon, for 1.2 million shares with another 180,000 for over allotments. The issue has a mandatory redemption on 10/31/2028.

Contrary to an initial press release the issue is rated BBB+ from Egan Jones (versus an initial indication of BBB-).

The fund is a CLO owner, and in many ways is similar to Eagle Point Credit (ECC) and Oxford Lane Credit (OXLC)–but much smaller with assets of less than $100 million.

The permanent ticker for the new issue will be CCIA.

The pricing term sheet is here.

FWIW Here is how I think of CLO equity which I have learned to compare to regional bank common equity.

With a bank the assets are cash and loans. The loans will be mix of mortgages, car loans, term loans to businesses etc. The Liabilities are deposits and term debt. Assets minus liabilities is equity.

Needless to say its the mortgage and the deposit flight that cause most banks failures.

With a CLO the assets are specifically leveraged bank loans. These are loans to large (generally public) firms which have below investment grade credit, variable interest rates and are secured. The liabilities are various tranches of bonds which are callable. Assets minus liabilities are equity.

CLOs don’t have mortgages or deposits which combined cause most bank failures.

With both CLOs and Banks – equity does not get $.01 until all of the creditors are paid.

A bank mutual fund is a portfolio of bank stocks.

A closed CLO equity fund is a portfolio of equity in various CLOs.

Bank preferred is non cumulative and is perpetual.

CLO preferred is always cumulative and commonly has a mandatory redemption. CLO CEF preferred also has preferable covenants. The terms and covenants of CLO term preferred are far superior to those allowed for bank preferred IMO.

So CLO equity actually has a few benefits over regional bank equity:

1)There are no deposits which can run. The bonds funding the CLO assets are not going anywhere and can be called.

2)All of the CLO assets are Sr secured bank loans with floating rates. No mortgages, no consumer debt, no loans to small businesses.

3)The CLO has a finite life with a well defined lifecycle featuring a reinvestment period. Structured securitizations comprised of other assets (EG mortgages) do not have a reinvestment period. Please see the Eagle Point video below for more on this topic which is quite involved.

4)CLO equity makes the determination when to call the various bond tranches.

5)CLO equity tranches earn positive abnormal returns. This is per the Wharton webinar available at the link pasted below. There are very few things on this planet that earn positive abnormal returns.

So some experts will say that a CLO is a better regional bank, and a CLO fund is better than a bank fund.

For these reasons I like CLO CEF term preferred equity and it is a significant part of my fixed income book.

I do not like the common equity in CLO CEFs because the fees are too high and bite into the abnormal returns. Common equity pays the CEF fees not preferred equity.

This the Wharton Business school video:

https://jacobslevycenter.wharton.upenn.edu/clo-performance/

I also find this video to be instructive which is from the CEO of Eagle Point

https://www.youtube.com/watch?v=OxivWs5vPTM

Hi A West- do you mind sharing your holdings re “I like CLO CEF term preferred equity and it is a significant part of my fixed income book.”

thanks

Sure ECCC and OXLCN are my two primary holdings in this space.

August, how do you feel about BDC preferred?

Hi Charles, I don’t own BDC preferred or common at present. I just prefer sr secured bank loans made against large public firms on the asset side of the ledger. There is nothing wrong with BDCs at all, and I know that many on here like them.

Hi August, I hold a couple BB notes for BDC’s for the same reason you hold the preferred of CEF’s just because there is a set date they need to be redeemed. I had been looking at the recent NMFCZ but decided to pass. I think both groups, BDC & CEF have companies that are better than others in their group.

I like your pick on the Eagle point , I own some EICB. Have been looking at the offerings of OXLC for a while but not sure I like how many preferred they have on the market but they do seem to be doing ok.

I personally like sticking with a company whose common is above $10.00 a share as I have trouble relating to how a sub $10.00 stock can have preferred worth more. Doesn’t mean anything I know, as people can point out examples why this is wrong. Just one of my rules.

Is NMFCZ actually trading?

David, Not sure, you might have to call in to place an order. Most times on stocks I wait to see how it trades the first week or so. I like to see what the market thinks and the people bringing it to market. If the demand is slow they will drop the ask especially if they don’t want to hold it. A few times I have missed out on a good deal waiting but I have no regrets.

This market might be on a run and it could continue through the end of the year, but I am sticking with deep out of the money bids and only moved my bid up on one or two GTC

Lately some of my bids have had partial fills which is fine by me.

Does anyone know the temporary grey market symbol for CCIA (or a good resource for finding these symbols)? Thx.

TDL–none has been announced. Maybe will go straight to permanent market. Normally they can be found here.

https://otce.finra.org/otce/dailyList?viewType=Additions

Thanks for that resource.

They were listed there Friday under symbol CARFP. I don’t see any trades yet.

Tasty is way more than 8.75% in this environment for a preferred equity issue.

legand.vs–yeah you are right–my brain was stuck in 2021–8.75% is more normal with 10% tasty.

CCIF is subject to the CEF leverage rules. CCIA should be fairly safe despite the CLO assets due to that. Of course, for those that want to walk on the wild side, if you can grab it at a discount as the underwriters sell, you will be paid better for taking the risk. It’s a higher coupon than ECCC, which is one of the most relevant comps.

8.75% isn’t great. You can get that YTM from ECCV which is a 2029 bond, not a term pref.

I agree Landlord. Plus, there are many bonds from other BDCs and similar shops with similar yields.

Pass

When you say bonds, do you mean corporate or baby bonds? Where would I go to find these? Thanks for any help.

RL – some are in the baby bonds which you can find here.

https://innovativeincomeinvestor.com/short-medium-maturity-income-issues/

Some are regular $1000 bonds which you can find on your brokerage site.

Does that really make a difference though? Is there a CLO apocalypse scenario where the bonds would be paid and term preferreds would not?

Yes.

David, this is an interesting question.

The preferred of Eagle Point Credit which is a CEF has the following covenant: “The Company is required to redeem the preferred at $25 per share plus accrued and unpaid dividends if they fail to maintain an asset coverage ratio of 200% (see prospectus for further information).”

So if a CLO apocalypse scenario unfolded in theory (at least) when the asset coverage ratio hit 200% the preferred would get called and the baby bonds would remain outstanding. The baby bonds don’t have this covenant. At least this is a theory – in practice it might not work out that way.

As a result I would rather be in the preferred and take the higher yield.

That is my theory at least.

AW – I only looked at ECCV but I suppose this applies to the other 2 notes as well – take a look at P S31 of https://www.sec.gov/Archives/edgar/data/1604174/000110465922004410/tm223013-1_424b2.htm#sDOTN

Doesn’t that say the note does have the 200% covenant?

We agree that, for the period of time during which the 2029 Notes are outstanding, we will not violate Section 18(a)(1)(B) of the 1940 Act, as modified by the other provisions of Section 18, or any successor provisions, whether or not we continue to be subject to such provisions of the 1940 Act, giving effect to (i) any exemptive relief granted to us by the SEC, if any, and (ii) no-action relief granted by the SEC to another closed-end investment company (or to us if we determine to seek such similar no-action or other relief) permitting the closed-end investment company to declare any cash dividend or distribution notwithstanding the prohibition contained in Section 18(a)(1)(B) of the 1940 Act in order to maintain the closed-end investment company’s status as a RIC under Subchapter M of the Code. These provisions generally prohibit us from declaring any cash dividend or distribution upon any class of our capital stock, or purchasing any such capital stock if our asset coverage, as defined in the 1940 Act, with respect to our borrowings or other indebtedness is below 300% at the time of the declaration of the dividend or distribution or the purchase and after deducting the amount of such dividend, distribution or purchase (provided that we may declare dividends on our preferred stock as long as such asset coverage with respect to our borrowings or other indebtedness is not below 200%).

Hi 2W:

When I read this is see that the covenant protection for the notes is focused on eliminating dividend payments to common and preferred given certain ratios. Note that this covenant benefits the preferred as well as the notes. This is because the common has a different threshold (300%) than the preferred (200%) for mandatory dividend cutoff. However, I do not see that it says that the bonds get called at par given asset ratio triggers of either 300% or 200%. Have I missed this specific language?

The covenant on the Preferred stock says that preferred stock gets called at par in the event given the asset ratio trigger of 200%.

While I suspect in practice this would be very messy, it just seems to me that the preferred covenant is better. I could be convinced otherwise. Prospectus language has proven to be a tricky thing.

In theory , it seems that there is a scenario in which the preferred gets called due to covenants and notes remain outstanding.

AW – I suppose that’s possible but I did not read further into the details… IMHO there are usually various avenues to cure a breach and a timetable to do it that include calling but could include other ways of curing as well. I did not look into the details…. It just seemed to be far too unusual to have a 1940 Act covenant protection written in that protects a preferred holder but not a noteholder so I went looking for the boilerplate on one of the notes and it seems to be there. I suspect but did not look that the preferred language also provides alternatives to calling them in to resolve a breach… No?

AW – A quick look at prospectus for ECCC seems to say what I would have suspected. From what you said, it sounded as though the first action required for a breach would be to call the preferred… I don’t think that’s the case… See https://www.sec.gov/Archives/edgar/data/1604174/000110465921080121/tm2119077-6_424b2.htm#tDOTS p S-27, “1940 Act Asset Coverage,” and then p S-28, “Redemption for Failure to Maintain Asset Coverage.” S-28 says nothing happens unless the breach continues after the Asset Coverage Cure Date which is defined on S-17, “Mandatory Redemption for Asset Coverage,” and even then a call need only happen within 90 days and only in the amount necessary to bring them back into compliance…

All of this is not to negate your point but to voice an opinion that there’s nothing special here and I would doubt (but could be wrong) that the said language is any stronger for the preferred than the note.. From the company point of view, there’s plenty of time written in to cure a breach before a call would have to happen…. Also note that there seem to be only specific days every quarter that a breach can be declared.

Hi 2W,

Fair enough, I am not saying it’s perfect. I agree with your point on the practicality of the matter, the timing and the amount of shares which must be called. This is all in the prospectus.

Furthermore, there are other cures that are not spelled out. For example, they could simply call the notes in order to bring the ratios into compliance. This, however, is the company option and is not mandatory.

This covenant also benefits the notes and the common.

The fact remains that there is a mandatory call provision on the preferred which does not exist for the notes.

For this reason, I still think that this covenant protection is superior to that of the notes.

Recall the original question was: what is the difference between preferred and notes given a CLO melt down scenario? Other than the obvious ranking in the capital structure and yields, I would submit that this is particular covenant is a material difference between the preferred and the notes. Furthermore, (given the fact that this is term preferred with a higher yield than the notes) I would submit that this difference is sufficient to select the preferred over the notes.

By hey to each his own.

Yup.. and to me this is an academic issue more than anything because “to each his own” leaves me not investing in either ECC preferreds or notes. No question it’s a complex issue and for all I know in the real world, the language for the preferred is stronger, but I doubt it. I’m not sure I agree with you about “they could simply call the notes in order to bring the ratios into compliance. This, however, is the company option and is not mandatory,” but again we’re in fine line differences here and we’re probably beyond the general level of interest of most here… But the note says, “You will have rights if an Event of Default occurs in respect of the 2029 Notes and is not cured, as described later in this subsection. The term “Event of Default” in respect of the 2029 Notes means any of the following [and includes]… “We remain in breach of any other covenant with respect to the 2029 Notes for 60 days after we receive a written notice of default stating we are in breach. The notice must be sent by either the Trustee or holders of at least 25% of the principal amount of the 2029 Notes.” And Remedies if an Event of Default Occurs says, “If an Event of Default has occurred and is continuing … The Trustee or the holders of not less than 25% in principal amount of the 2029 Notes may declare the entire principal amount of all of the 2029 Notes to be due and immediately payable.” That would say to me that it is not strictly at the company’s option….

But let’s agree to agree that the 1940 Act provides theoretically strong protections to noteholders and preferred holders that could be useful to either/both before any issuer runs into deep financial trouble. OK? Let;s hope we never have to find out how it actually works for either in applicable practice…

Works for me.

However, the topic might be more than academic for some, and should be of interest to others.

This mandatory call covenant of preferred is not unique to ECCC. The mandatory call of preferred stock covenant can be found in several CEF preferred issues listed on the CEF preferred list available on this site. What is interesting about ECC is that it has both preferred and baby bonds outstanding so this comparison can be made. So it seems to me it is relevant when comparing preferred vs bonds in any CEF which has, or potentially could have, both outstanding.

Carlyle has said they may issue baby bonds as noted on slide 9 of this deck:

https://filecache.investorroom.com/mr5ir_ccif/701/CarlylePresentationtoVCIFShareholders-May2023-CCIFWebsiteVersion.pdf

Also the Carlyle preferred that is the subject of this thread has this very provision in the prospectus.

One would think it is there for a reason. Perhaps it is part of the 1940 Act?

From a practical perspective, should the 200% threshold for the Preferred be breached, a possible cure would be to call the bonds thereby reducing leverage and increasing coverage.

We’ll have to see how it trades. If you can get CCIA for $24.50, that would be the same YTM as ECCV and a much higher CY.

To me this seems like it could be an LNC-D like opportunity.

How does the risk/reward look to you guys?

I don’t think that large collections of CLOs are all that dangerous, even if things go bad.