Bankers are getting hammered once again–PacWest, Zion, Western Alliance and First Horizon (because of a failed merger with TD bank). If we are going to see another bank failure it is PacWest – this will play out within a week I think. Personally I have a handful of banking preferreds, in small quantities, but even the small quantity caused some pain yesterday. My desire to balance treasury and CD holdings with higher yield small banks appears to have backfired for the time being–i.e. It was too early. My hope is this plan will work out very well, but certainly now is probably not the time to buy.

After the FOMC rate hike yesterday we need to start watching for weakening economic data – starting this morning with initial unemployment claims and then tomorrow with lower new job creation and higher unemployment. It is time to stop hiking interest rates, but we need to get affirmation from the data and employment is a giant factor in the Fed decision making. Never underestimate the ability of the Fed to screw things up. We’ll see!

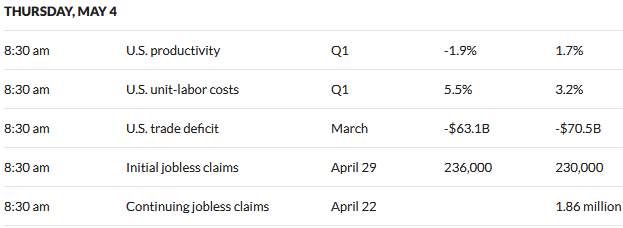

Here is today’s economic calendar.

I wrote yesterday that I bought some of the RiverNorth Opportunities Fund 6% preferred (RIV-A) via a good til canceled order at $22.50. The 6.68% current yield provides a great yield for a closed end fund preferred with a A1 rating (assuming the rating is meaningful). It is my intention to put in another good til canceled order today maybe at $22.

Equity futures are a bit soft today while the 10 year treasury yield is lower – now at 3.35%. Let’s get to going and see what the day brings us!!

Doesn’t matter until the dust settles but a local Northern California Bank

I read about that doesn’t have any deposits over 30,000 and hasn’t been at the Fed window.

TCBK, Divy is only 3.87% but if it falls farther could have a lot of upside when the economy starts growing

My low bid of 37.70 for NYCB PU hit yesterday.

Oh my I was buying yesterday around 330pm. It seems the panic is real and there is blood in the streets. And I saw two quality 7’s under 19. Maybe I round up on the opening……

Mtg reit preferreds getting dumped along with banks despite not exposed to the same type of bank run risks. Ofc exposed to funding risk and spread risk, but at least they mark to market and have some term financing.

Three failed US banks had one thing in common: KPMG

https://www.ft.com/content/feb33914-493e-467c-b67e-28fcd1b3814d

You can cut and paste into https://archive.ph/

Some days you are the bird 🦅, this week anyone that has financial investments is the statue 😱 or in Latin aliquot dies es avis, alii tu statua!

I think the bird of paradise flew up my nose today…….

With all the turmoil in the regional banks, the big banks seem to be doing fine.

I bought a little JPM late last year around $110 and sold for $140 last month. Thought I might be able to re-enter with all the bank mess, but no – JPM is still in the $130s.

Must be nice to be too big to fail.

PACW @ noon EST…

stock down 50%

trading volume 4X normal

Adios

Watching OCFC, might be next up

Righ now 5/4 CD rates at Fidelity top out at just over 5% and thats for a yr or less…..goes down from there and they are callable….I own WFC and C preferreds…should I be worried about these?

no, because wells is a Global Systemically Important Bank. Doesn’t mean they couldnt suspend the dividend, but highly unlikely based on their recent financials and the fact that if Wells go down, it really doesn’t matter where u have your money at that point.

IG insurance issues appear to be holding so far.

I’m watching the IG larger banks to fill positions BAC / JPM / USB when this mess settles. When? Not sure but building cash. If all this happened later this year I would be taking a real beat down. Better lucky than good timing.

One of the talking heads this morning noted that the recent bank crisis cost almost totals Leman Brothers fiasco.

That gave me pause and made me think a moment.

I already have full positions in the ONBPO / ONPPP issues but may add as well later on.

What give me pause is the debit ceiling fiasco. I have no answers but could be a disaster either way.

Be well, stay safe.

Speaking of larger banks, yesterday Moody’s upgraded a bunch of BAC paper, including preferred stocks (up a notch, from Baa3 to Baa2).

https://www.moodys.com/research/Moodys-upgrades-Bank-of-America-Corporation-senior-debt-to-A1-Rating-Action–PR_475974?cid=GAR9PTU7VKT2671&emailToken=eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzI1NiJ9.eyJVc2VySWQiOiJkYzVkYjczMC01NTBiLTQ3ZjctYjhjZi05NzY2ZjAxZmU0MzMiLCJEb2NJZCI6IlBSXzQ3NTk3NCIsImNyZWF0aW9uRGF0ZSI6IjIwMjMtMDUtMDNUMTc6NTQ6MTYuMDgwMzY4NC0wNDowMCIsImV4cCI6MTY4Mzc1NTY1NiwiVXNlck5hbWUiOiJjcGFtaWtlbWJhQHlhaG9vLmNvbSIsIlVzZXJUeXBlIjoiMiJ9.gKZ7QCK2v7GSBd5fSj1V6yGnl3JKIjTZiBIbEX0N_T0

Among the Upgrades:

….Pref. Shelf Non-cumulative (Local Currency), Upgraded to (P)Baa2 from (P)Baa3

….Pref. Stock Non-cumulative (Local Currency), Upgraded to Baa2 (hyb) from Baa3 (hyb)

I must be missing something, but how is it that the Fed raises the Fed Funds rate, but the 10 year yield goes down? I know they are slightly different animals, but they are related, and really, they raise the rates they charge and the result is the rate the government borrows at goes down? This seems like an upside down world. How long can that last?

The hike was expected and the Fed signaled it could be the last hike. Buyers anticipate future rate cuts though the timing of them is just an educated guess now. Fears of recession and further weakness in the banking sector after another bank in trouble announced after market closing yesterday. Lending is freeezing up. Numerous factors could be moving rates, including panic and flight to safety.

MBIN getting spanked and I have MBINM which is getting spanked along with it. I am thinking just avoid all banks till this blows over.

MBIN preferreds are puking HARD. I own a bit and have been keeping my eye on it because their book is largely floating-rate and they don’t really have the kind of problem that SIVB or FRC did.

Like any bank, none of that will matter if all the depositors decide to pack up and leave, but I think MBIN is better situated than most…

Good news is that I shorted WAL pre-market at $25.70 but then sold the $24 puts for May for $3.70. I’ll make $$$ there but could have made TONS!

I don’t understand, why did you sell the puts?

FYI – Pennypacker & Crew put a BUY yesterday on BTO. This is a 20% leveraged $550 Million closed end fund (that does not hedge its floating rate debt costs) that invests almost exclusively in regional banks that also trades at a 14% premium to NAV.

Only that crew could recommend paying a 14% markup on a leveraged regional bank portfolio in this environment. You can’t make this stuff up.

We may have a long way to go in this bank selloff. The banks are already knocking on the SEC’s door begging them to restrict all short sales in the banking sector. Certainly could happen.

Amazing Kid Twist. Thanks for posting this. I almost fell out of my chair laughing and I am still at risk to do so.

Ocean First had some reassuring comments. Not in as big of a hurry to dump it anymore.

From the 10Q

Robust Liquidity Position: The Company enhanced on-balance sheet liquidity by increasing cash and due from banks by $328.2 million with a corresponding increase in deposits of $317.9 million. Excluding a $364.2 million increase in brokered time deposits, deposits decreased less than 1%, reflecting stability in the deposit base. At March 31, 2023, the Company’s loans-to-deposit ratio was 100.5% and the Company had total available liquidity and funding capacity across multiple liquidity sources of $3.6 billion.

Strong Balance Sheet Quality: Stockholders’ equity increased to $1.61 billion at March 31, 2023, or 11.88% of total assets, which were adversely impacted this quarter by the increase in on-balance sheet liquidity. Additionally, the fair values of total debt securities portfolio improved $23.6 million and asset quality remained strong.

Solid Margin and Earnings: Net interest margin was 3.34%, an increase from 3.18% in the prior year and a decrease from 3.64% in the prior linked quarter. The current quarter yield on interest earning assets expanded to 4.68% and the cost of funds increased to 1.76%. Costs of funds were impacted by the tightening of liquidity across the industry and, to a lesser extent, the increase in on-balance sheet liquidity. This resulted in net interest income of $98.8 million, an increase of $14.6 million from the prior year and a decrease of $7.7 million from the record prior linked quarter. While down relative to a very strong linked quarter, the current quarter results compare favorably to the preceding three quarters of 2022.

Ha….. As if anything like solid facts and figures reported by any bank at this time matters…….

@2wr

Yeah, I hear you. Triumph and Hartland preferreds starting to dive dive dive.

Caveat emptor

They were one of the 7’s I was referring to. One problem with their issue is the bid/ask is wide enough to drive a truck thru it…..with the doors open. I don’t know about their financials, though they have some fans locally!

With the 5 year treasury down to 3.35%, and a 5 year CD from MS for 4.5%, while not the 5% like cd’s were, seems like a big spread presently

Better double check though, often those longer-dated CDs are callable by the issuer so it’s not an apples to apples comparison.

O. Chongusu….the cd mentioned, cusip 61690U5S5 is not callable

PACW is creating its own bank run on itself. Deposits were actually flat-to-growing since SVB. They had a pretty decent earnings reports overall. By leaking this news, they’re crashing their own stock price which could spook depositors.

Landlord,

I’m sure they understood that. Maybe there’s something they know we don’t.

The silver lining in the First Horizon disaster- apparently they negotiated a decent break up fee. First Horizon will be paid 200 millions plus an additional 25 million in reimbursements for fees and expenses.

IIRC, there was also 400mm converted into equity at $25.