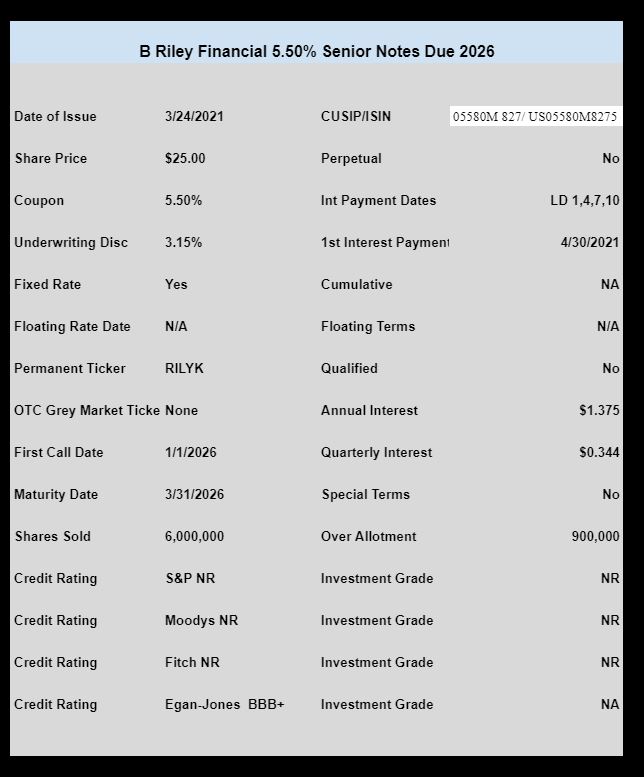

Financial services firm B Riley Financial (RILY) has priced their new issue of baby bonds.

The company has priced 6 million shares with a coupon of 5.50%. There are 900,000 shares for over allotment.

The company has stated that proceeds over $100 million (if any) will be used to redeem some (or all) of the 7.25% issue (RILYG) issue.

The issue is rated BBB+ by Egan Jones.

The ticker RILYK will be used for the new issue once it begins to trade on NASDAQ. There will be no OTC grey market trading in this issue.

The pricing term sheet can be read here.

Why wouldn’t they call the RILYH shares instead? They pay a higher interest rate and mature much sooner.

They’d have to redeem H at ABOVE par before 5/31/22–see QOL.

Good question…I would have guessed the 2023 maturity date on RILYH would hold precedence over the slight premium they’d have to pay for an earlier redemption. Plus they’d save a bit on the interest rate. Someone good at math can figure this out

RILYK is now trading

The pricing sheet says first call is 01/2026 and maturity is O3/2026. Is the call date incorrect?

Wilson–like me you did a double take. I triple checked and that is what is printed.

Does pay to double/triple check. I recently bought some OFSSG well over par as QOL showed both call and maturity dates 9/30/23, so I figured still decent YTC for short term holding. Only afterwards did I get that feeling that I should confirm via prospectus…and found call date actually 9/30/21. YTC quite a bit less (although I’d still be ahead). And QOL quickly updated after I notified them.

RILY is taking a page from the book of institutional issues, where first calls often come just shortly before maturity.

It has to do with something called the Liquidity Coverage Ratio. When a debt issue matures in less 30 days the issuer has to keep additional reserves on hand, which they don’t want to be obligated to do.

From an investor point of view shortening the time from first call to maturity is a good thing:

https://www.investopedia.com/terms/l/liquidity-coverage-ratio.asp