Below is a link to a story on an office tower than just sold in downtown Minneapolis.

The building sold for about 1/2 of its assessed value–what the previous owner was carrying it on the books at I have no idea, but you can be certain it was way above the sales price. This one appears to have been owned by a retirement fund who walked away from it and now the seller is Northwestern Mutual.

As we watch for earnings coming from the regional and community bankers we need to watch for how much of their commercial real estate loans are in central business districts–hopefully not too much.

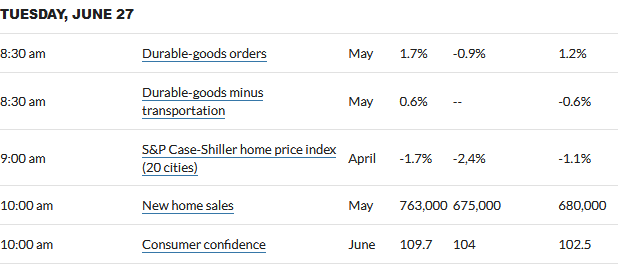

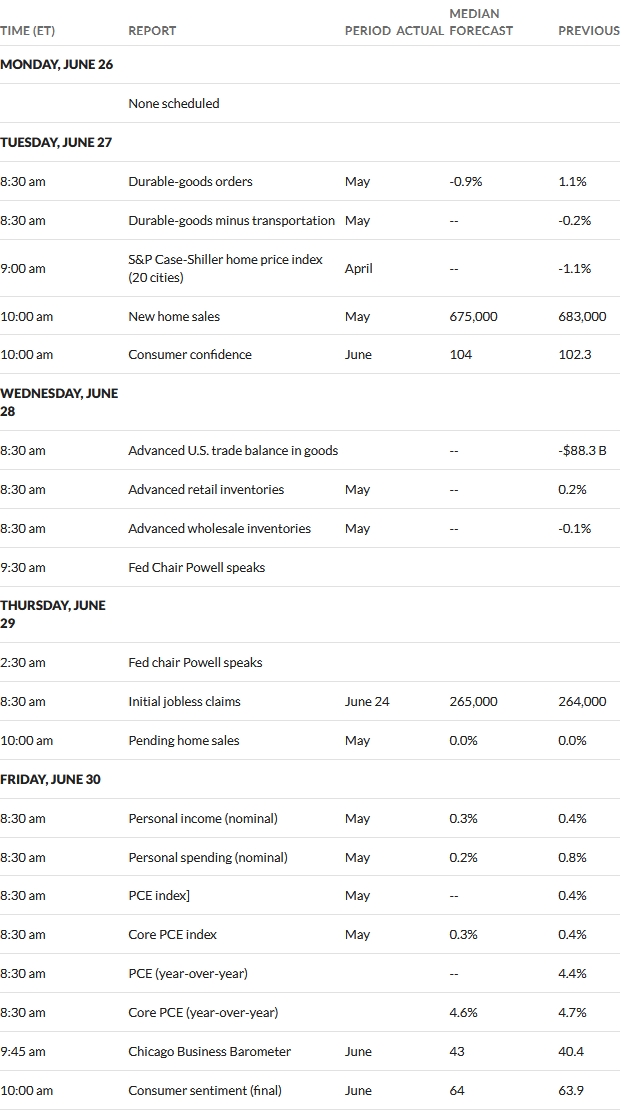

Yesterday we had new home sales numbers released that blew the forecasts out of the water–763,000 versus 675,000 forecast–wow!! Strong employment is driving housing and new house sales are up because folks in a house with a 3% mortgage don’t list their houses for sale–buy new or go home. At the same time as sales shot higher Case-Shiller showed prices down 1.7%–that is a 20 city average–I question this because anecdotally prices are moving higher (albeit at a slow rate) in much of the midwest.

Durable goods orders moved higher by 1.7% versus a forecast of -.9%. Data is building for a Fed funds rate hike in July–it is way to early to say for sure, but the Fed is looking for ‘cover’ to be able to justify their ‘data dependent’ rate hike.

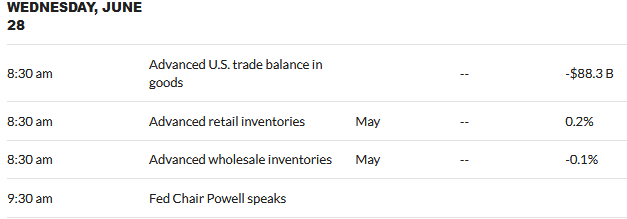

Today we have just minor economic new on the calendar – but Powell is speaking (and we know what his line is).

Many of you already know that Brookfield Reinsurance has made an offer to buy American Equity Life (AEL) which has 2 preferred issues outstanding. Preferreds of company’s that are bought by any of the Brookfield divisions tend to fall sharply–but the AEL shares did not fall yesterday. It is a misplaced belief that Brookfield suspends preferred dividends – they make each company carry their own weight and the parent company does not ‘bail out’ various divisions that can’t earn their dividend. Let’s hope sane heads prevail with the preferred shares.

Below are press releases from companys with preferred stock or baby bonds outstanding – or just of general interest. News is very light at this time, but earnings season starts in just a couple of weeks.

Below is a link to an interesting read on a study of the performance of high yield preferred stock ETFs. As individuals we can certainly outperform most of these ETFs–we all have opinions of course, but when you see the high yield funds giving a total return of less than 2% per year one must question why folks invest in the high yield funds.

Markets are pretty quiet this morning – both equities and interest rates. I know that I am not paying very close attention to the markets, partially because of the level of investments I have in fixed income vehicles at favorable rates. I can see it in the website traffic as well. During the summer traffic is always down from the colder winter months as people can get out and about. A good old fashioned ‘panic’ really drives website traffic. If I Iook back to August of last year website traffic here was up over 100% compared to previous months (an exception to the normal down summer traffic)–during August preferreds and baby bonds fell 20% – folks panic and come here to see what our very wise participants have to say and I have to say that folks on this website invest about as good as any I see anywhere.

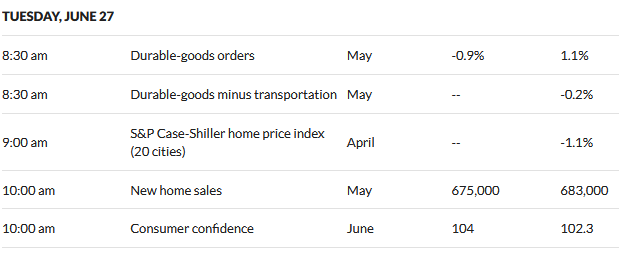

Well we get some economic news in 10 minutes – a few of the stats relate to housing and I watch these closely as housing is one important driver of the economy. Because markets are pretty sleepy it is unlikely that we see any sharp market reaction.

As mentioned yesterday I am in a holding mode until next Monday as I await maturities of CDs and treasuries on Friday. I am not really looking for more banking preferreds, but I still believe it is an area of great opportunity. Fortunately we will be getting earnings news from many bankers next month and with it will come data on commercial real estate–on the flip side as one awaits further data the best ‘bargains’ will likely evaporate–if the data gives one the green light prices will be higher leaving the maximum capital gains in the rear view mirror. We’ll see what the market presents us in the next few weeks.

As a bunch of treasuries and CDs mature on Friday one has to consider whether they should all be rolled over into new CDs. On the other hand I have little dry powder and want some available for ‘bargain hunting’. It seems to me that we could see some CDs near the 6% level in a couple months–that is a firm maybe of course.

Today I see this on Fido for short term CDs. Of course various terms are available (callable versus non callable)

Over on eTrade I see this rates available. Of course various terms are available (callable versus non callable)

I am fairly certain I will take maybe 50% of my proceeds on Friday and go right back into new CDs–with the other 50% being held–at least for the time being, for potential preferreds or baby bond ‘bargains’.

Can the rates go higher–yes if the Fed follows through on their rate hike threats rates will go higher–6% certainly is in the realm of possibilities and decisions can be made later on on purchases at these levels as my ‘ladder’ of maturities will provide funds.

Last week, which was a 4 day week, we saw the S&P500 set back by about 1.4% which leaves the index about 2% off of the 52 week high. This morning the index is just barely red–kind of surprising given the absolutely crazy events in Russia and Ukraine over the weekend.

Interest rates are trading at 3.69% (the 10 year treasury) this morning which is about 4 basis points lower than the 3.73% close last week. Once again we had quiet trading in interest rates last week with the 10 year moving in a 12 basis point range (3.69% to 3.81%). This tight trading range seems to be holding irrespective of economic or geopolitical news – well we can be certain that something will break within 60 days, although by and large these events are not predictable and one can’t know what it is that will break.

Last week we had the chief Fed yakker (Powell) in front of congress testifying and it was obviously his goal to continue to threaten further rate hikes as soon as July (the next meeting is July 25-26). Of course if they are really data dependent none of them have made up their minds (Ha Ha). We get the supposedly important personal consumption expenditures (PCE) this week (Friday)—plus lots of other more minor data points all week.

The Fed balance sheet resumed the march lower falling by $26 billion last week to stand at $8.36 trillion which is down from the highest level ever which was just short of $9 trillion.

Once again I have no reliable data on the weekly movement of $25/share preferreds and baby bonds. Google continues to be unreliable relative to quotes. I have 3.5 years of history of value levels and want that data to continue to build so will look at alternatives for those quotes that have not been working–I have an alternative source, but even those have been unreliable.

Last week we had no new income issues announced or priced.

The fear trade is alive and well in the smaller community and regional bankers–fear of interest rate hikes and resultantly commercial real estate failures of which these bankers have some pretty large interests. Everyone needs to keep a close eye on these bankers, unfortunately after a month or 2 of over communicating we are all stuck now with little new data–on top of this we had the head Fed yakker testifying before congress the last 2 days-with ongoing threats of further rate hikes. Investors can either take another ‘bite of the apple’, sit back and watch or sell. Obviously with nothing new known I am holding–and will consider further nibbling in a week when a large number of CDs and treasuries mature replenishing my dry powder. I’m looking at the Merchant Bancorp (MBIN) issues and Associated Bancorp (ASB).

Well the S&P500 has been soft this week and is soft again this morning–all of which is helpful in resolving what I believe is an overly optimistic economic view of equity markets. It seems healthy to have some backing and filling in indexes instead of something that goes up week after week. This is not the S&P500 of the olden days–this index is filled with tech companies so necessarily the index will likely run in the direction of the tech company’s.

Economic news this week has been mixed–like it has been for months and months. Yesterday we had 1st time unemployment claims up some from what was forecast–264,000 versus 256,000 expected–no giant jump and a continuing indication of fairly strong employment. The number of housing starts, which was released on Tuesday, was truly impressive at 1.63 million new starts versus expectations of 1.39 million. I have always written, and believe, that employment breeds housing demand and to me strong employment is the number 1 indicator of the future of the economy. I’m still looking for the forecast recession–I can’t see it as of today.

Well lets’s get this day started–it looks like a soft day in equities, but a Friday at the end of June means that equity volumes may be light and directions can change quickly–whatever–it will do what it will do.