Am I missing something? Anytime a rock solid investment goes further south than one would hope I like to look back on the financials and see if I am missing something.

The Liberty Broadband 7.0% cumulative preferred, which has always traded very strong, has fallen more than I would have thought was warranted so I wanted to check the financials once again.

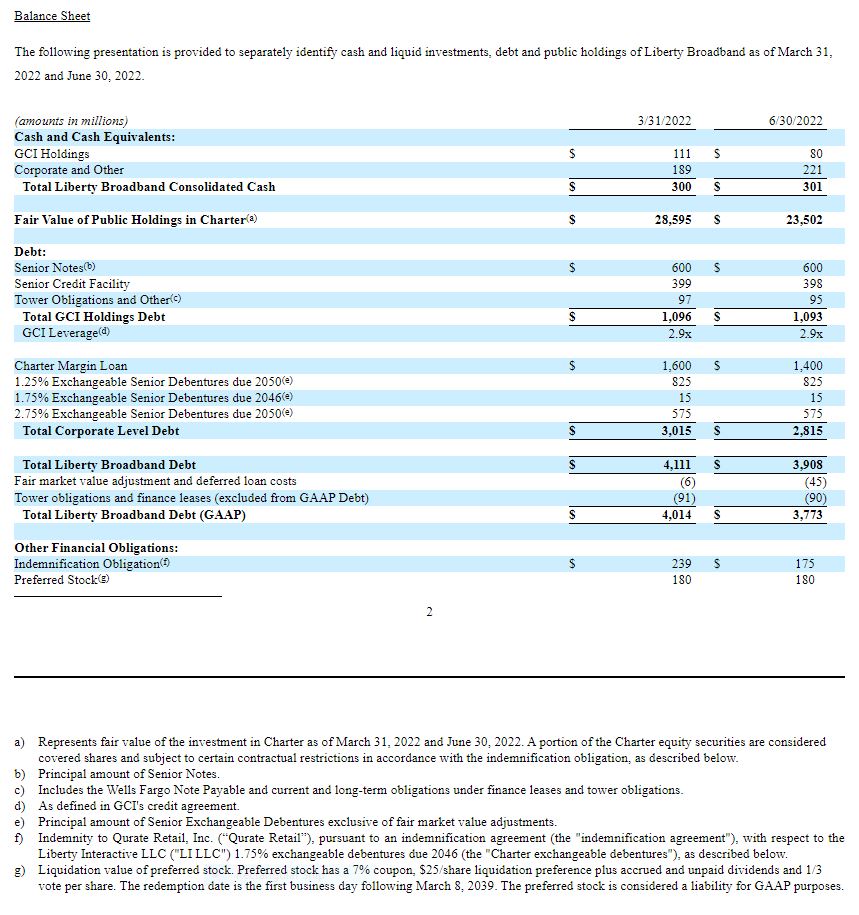

Below are the balance sheet financials for the quarter ending 6/30/2022 – the most recent available.

This shows that their assets are $23.5 billion in Charter Communications (CHTR) which is their main asset. Total liabilities were about $3.8 billion. Net assets being about around $20 billions.

Charters stock price had a 52 week high of $740/share and the price was $469/share on 6/30/2022. Share price is currently about $315. So the share price has fallen about 33% since the last report–this gives me a guesstimated asset value of close to $16 billion right now against liabilities of less than $4 billion.

The bottom line is that after Charter being totally ‘creamed’ in the last year Liberty Broadband still has net assets of about $12 billion to ‘cover’ $180 million in preferred stock—so it has coverage of about 60 times.

What this means is I am comfortable with this holding and even to add more to my position. Let the nervous nellies give me the shares cheap.

I think any investment where Charter/Spectrum represents a major portion is quite risky IMHO. Charter’s sales are about 33% VIDEO, 41% INTERNET AND 25% OTHER MISC. SEGMENTS. The 33% video segment is probably deteriorating at a fairly high rate due to streaming. Go to any Charter outlet and just note the number of customers turning in the cable equipment, me included. The price for content wasn’t too bad but that cash cow $10/mo charge for the interface box was terrible. Those boxes probably cost them less than $40 so after 4 months it was all profit and they won’t sell you a box. The content available on streaming is also so much greater. (I am spending less than 1/2 that I paid Charter for TV and have much much more to chose from for content with streaming)

I think losing a significant portion of 33% of their business adds considerable risk. To make up the difference in their other business segment would be very hard.

I don’t understand the love for LBDRP. CHTR bonds are not IG, so a fund that holds CHTR stock (with no asset coverage requirement) would have a greater chance of going to zero than CHTR bonds.

If CHTR was on the path to bankruptcy, would LBDR sell its CHTR stock to avoid bankruptcy for itself? I think the answer is no unless LBDR debt has covenants requiring a certain level of coverage. Even then, I think LBDR would go into technical default rather than sell a huge amount of CHTR stock at a low price.

That said, I don’t see the LBDRP preferreds as declining more than many other preferreds. Looks like it just got caught up in the general market pullback.

Got LBRDP at $24. Great review from Tim as usual.

Mkt weak going into the long weekend. Buying pfds now with an eye to holding for blended rates over 7% at least. These will be keepers in the Roth IRA. No flipping Bea, as tempting as it can ‘be’. I did well in the June swoon selling many names in Aug. But looking for more permanent plays.

Probably early I usually am. Recent buys include SLG.PI, AHH.PA, GMRE.PA (I know on the scarier side) CTO.PA , UBP.PH- at least at or near ‘for now’ lows.

GLTA Bea

Bea–7% is my minimum target on preferreds/baby bonds–my current yield is about 7.05% (of course it goes higher with each of the giant drops). But I added a little Ready Capital 6.50% preferred today with a current yield of 8.96% which helps goose things a bit.

me too finally after all these years getting some returns I can accept. My worry child is ATLCP (not that worried, they have $24/sh in cash as of 6/30 but their market tends low FICO. ‘juicing’ I guess..

Supposedly this market of folks is working and paying things!).. B Riley just put a buy on the common. My basis is about 23 so not too bad. I guess we all have one or two we think and rethink on.

My other holding is the STAR.PI despite all indications it will be redeemed who knows anymore, but it does feel safer w all the cash they have around. And NSS basis around 24.50 overall on that one. I did sell some post interest xd to buy the SLG.PI at 21.50.

Personally I feel advisors will be looking hard at a lot of pfd/bb bonds to quiet the calls into yr end on the stock/bond/crypto losses as ‘better than cash’.. people need income and are still retiring in droves in 1st world, US, JP, CN, EU… patience I think.

Tim – with so many different preferred’s how would one go about buying the “best” ones. I understand “best” is subjective, but in this case, the best % return for medium risk?

It seems a dauting task.

Much appreciated.

sjc, Subjective…yes…absolutely. Ultimately the answer will depend on your own criteria in establishing your “lane”.

I have an enormous amount of respect for the many talented contributors here (which is basically everyone), including the ones for which I don’t totally agree. We all have similar goals, though all with different sets of criteria. There are many “lanes”.

For myself, high IG (BBB at least), OK to buy into falling prices, hold for longer, low coupon is OK sometimes even preferable, no BDCs, no shippers, safety, safety, safety. Some would agree, others may think I’m nuts. In one way or the other, they’d both be correct.

Throwing one item out there for you that I’m sure all will agree. Once you have defined your goals, be certain you are spending at least as much time understanding the risk side of the equation as you are on the return. You will find your lane.

Thank you – much appreciated.

sjc – Agree with alpha here. There are tons of contributors here that execute at a much higher level than they give themselves credit for and each of us have a slightly different approach at it.

I tend to fall in very close lockstep with Alpha’s approach by my own design. Purely by our own personal objectives and solving our own needs and problems through investing. Sometimes I even ask myself “Is this investment boring?”. Seems to really round out any questions and due diligence on the risk side. I also tend to try to maximize my “Return on hassle (ROH)”. If I venture into some higher risk/reward stuff I really make sure I understand what I am getting into because there is a point where something just becomes way too big of a problem child for me to worry about it. Luckily, many of the contributors on here fast track that due diligence process. Almost a golden goose. Cheers

Shep

“ROH” … I’m going to have to steal that metric 🙂

LBRDP, due to the John Malone factor, has a low ROH in my opinion. Too much hassle for me to figure it out. It may ultimately be a fine security but it’s more brain power than I wish to expend on an issue. I use to own it but was lucky enough to sell it in early February as I didn’t understand it and had low conviction in holding. Just my two cents.

sjc—thats a tough one. First you need to know your risk tolerance – I don’t do shipping issues and very few residential mREIT preferreds–over a very long term basis (20 years) I have found they can lead to problems. I don’t chase the real high yield stuff with rare exceptions. I love investment grade and then next the issues that are just below investment grade (i.e. BB with Standard and Poors and Ba1 with Moodys)–this matches my risk tolerance pretty well–good yields with modest risk. My exceptions to good quality issues are those with short maturities–Oxford Lane and Eagle Point credit TERM preferreds since they mature in a short amount of time which typically helps their price to be kind of stable. Then I diversify bunches–right now I hold 51 issues (preferreds and baby bonds). Everyone is different and you will just have to try a few out–certainly there are lots of good ideas from folks on the website that have more wisdom than I have.

Hi Bea – Any concern with SLG capitalization as the stock is trading like the dividend is unsustainable.

Is there risk to a preferred divy cut? Or the preferred being stopped altogether?

Bea – Just my opinion, but I think that by not flipping, you’re missing an opportunity to book some gains to offset losses on long term holds, especially in this more volatile market. Keep the long-term outlook but take the gains and acquire more desirable issues.

the charter 2038 bonds trade 7.3/7.4% so isn’t this in-line? Are the bonds higher in the cap structure?

Added 100 shares of LBRDP 23.9s…..

bob–yes the bonds are higher in the stack–I should look at that.

The bonds that are being referenced are also senior secured bonds which make them quite a bit safer than the unsecured ones. You can get some unsecured bonds maturing in 2032 that yield 8%.

Hi all,

Great forum. Learned a lot. One tidbit to share. No idea if possibly relevant.

On the Fidelity website there is a misprint about LBDRP. It is quoted as:

LIBERTY BROADBAND CORP CUM PFD SR A 5.00000% 03/14/2039

Should be 7%. Called their trading desk yesterday and they said “thanks for the heads up”.

Best to all-

Mark

Mark– I have noticed that as I hold all y shares at Fido–maybe the nervous nellies think they have a 5% issue.

I believe it was a 5% issue originally, maybe when it was GLIBP. Then got boosted to a 7% issue. I know Grid knows the details as I recall reading this from some things he posted

And I think Grid also mentioned there is a kicker if they delay a payment

Yes, Mav,it was set up for 5% for a period of time then rolled over into the now permanent 7%.

I certainly dont think its a bad issue, as I was the one who originally brought it up as it was rolling into the 7% and got the appreciation, and have owned it frequently since. But as I have been saying the past couple weeks, I dont see any more relative value than other 7% plus issues. Charter Senior SECURED (not unsecured which is where rating agencies tend to start from) is Ba2. So senior unsecured would be slotted B+ range. A preferred would be B-.

I find it hard to believe if Liberty preferred was rated how it could be much above that since its value is largely derived of common stock from above said company.

The companies financials are typically unique “Malonesqe” so way above my inferior pedigree. Certainly I sense no problems here, I just think there are a lot of 7% ish issues of good quality now that can compete equally with it. Its just rerating to todays yield environment realty it appears to me. In fact it hasnt been hit as hard as many others.

Thanks Grid for the info.

I agree with you there are a number of 7% plus issues of good quality out there that are equally attractive, especially if you get them on some quick dips

I just bought a small amount of ESGRO for example under $24 today

Grid–thanks–I thought that was the case but my old brain couldn’t dredge up the details.

Not sure Grid–I like the asset coverage on the preferred–and their asset (Charter) is level 1 so we know right where it stands.

Grid , care to share some of the 7% issues of good quality? Of course will do my own digging but would love to hear what u think.

Franklin as you well know, beauty is in the eye of the beholder. And what will likely always pay doesnt ensure it wont keep dropping lower while still paying, ha.

Bea and Tim mentioned some to peruse. Others of course are CHSCL around 7%, The Urstadt Biddle preferreds will always pay as those 2 families run a tight ship and typically own anchor malls where people tend to pay for their goods instead of smash and grab. The BIP K-1 preferreds are default BBB- rated and near 8%. EP-C YTM is frequently 7% or more.

To be honest Franklin the only issues I have that are 7%-8% are the BIPs which I recently bought (K-1 alert), EP-C assuming it still is, RZA (gonna get called), and just toed back in on some GJH.

I tend to have more money in total in issues above 8% and lower than 7% for whatever reason. I have some short duration debt in 5%-6% range and some short CDs too. And I have been buying lots of my local utility 2039 A2 senior secured anytime it pops over 6.2% which it did again today. Also bought a smaller amount of nearby 2033 Senior Unsecured Empire District at about 6.15%. The drop off in duration debt has been dramatic, The Union Electric one now around $122 was over $160 earlier this year. I dont mind some 6% ish annuity debt to hold.

I own a decent chunk of live floaters too though so I am kind of spread out duration wise. That may not be ones goal, so that is kinda the prism I look through. I kind of am enamored with Fortis as I view it as a ute powerhouse, owning several large US utes and a huge former ITC named transmission line.

So I bought into the Series F when it hit 6.2% a little while ago and keep small ball buying the reset G issue in drabs buying 300 today at 12.57 USD. Those are a bit low for you, but G could possibly reset well over 8% next year…or not…The price one pays to step into the ring, ha.

Thank u Grid. That is very, very helpful and interesting. Much appreciated.

Even BIGCHARTS.COM has it at 5%, adding to quote confusion- and nothing on

QOnline.

Schwab got it right, but does also show “original 5%”

Tim

I’ve started a position at $24.09 and looking to add below $24.

I wonder if it’s a victim of being a large holding in an income fund or two which is having folks bail.

Greg – anytime an issue is out of the norm – folks don’t understand what Liberty Broadband is all about. Don’t know but you could be right.

Just looking at the trades the past week or so, many of which appear to be computer algorithm driven sometimes hitting within a split second of one another, I agree there is a large seller out there, likely a fund liquidating