kaptain lou had written about the 6% issue on Seeking Alpha a couple weeks ago and the E issue was trading at $24.35–yesterday it took a tumble to as low as $22/share–bouncing back today to $22.75.

BFS is one of the stronger retail REITs, but there again if you are totally negative on the sector these are not for you–but some due diligence by an investor may prove to them that at these prices there are bargains to be had if bought now.

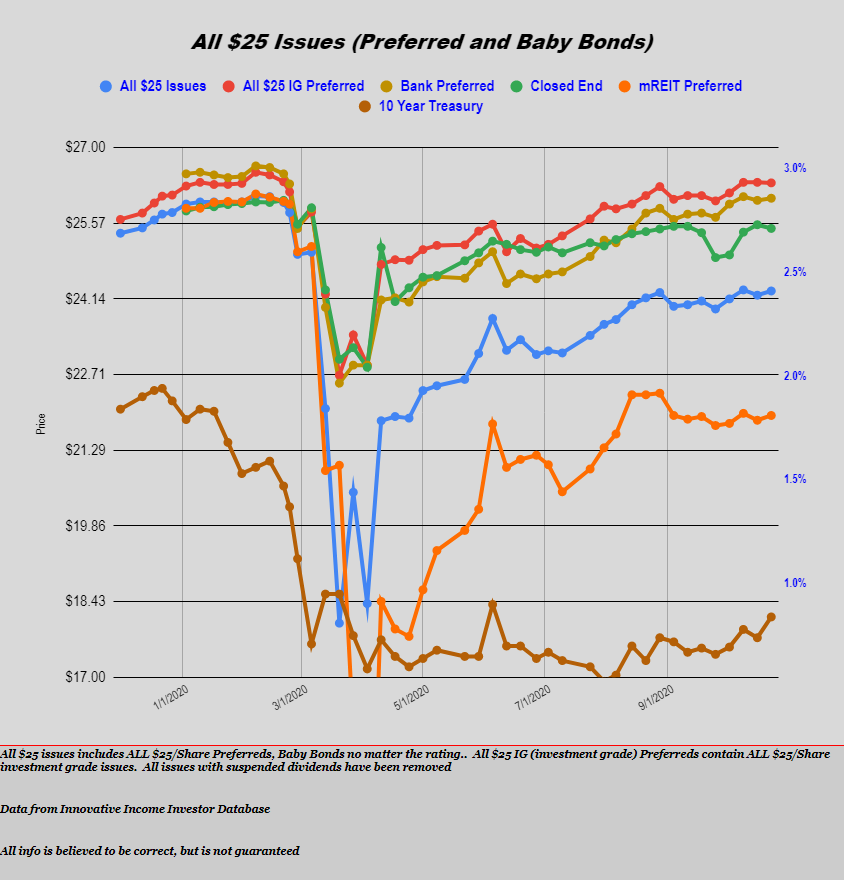

The pressure has been on common shares all week and through yesterday the general market downdraft had pulled preferred shares an baby bonds down by about 15 cents on the week.

Right now the average share price is down by 29 cents on the week and while investment grade issues sometimes hold up better than the general issue population that isn’t true right now. Investment grade issues are off 30 cents on the week.

For the last 2 weeks I have been watching the lodging REIT preferreds–this is the sector that has been beaten up quite a bit–I show shares off about 4-6% in recent trading. This includes those shares from the strongest REITs. For instance the RLJ Lodging Trust $1.95 issue is off 90 cents today. Other strong company’s have been taking it on the chin also–this includes the Sunstone Hotels and Pebblebrook Hotel issues. All the lodging REIT preferreds are here.

As always I am looking for bargains, but honestly a bargain is in the eyes of the beholder–I am not talking 25 or 50 cent lower bargains (although in some utility baby bonds and CEF preferreds 50 cents or a dollar lower might make bargains)–I’m mostly talking in dollars and I am not expecting to see those right now.

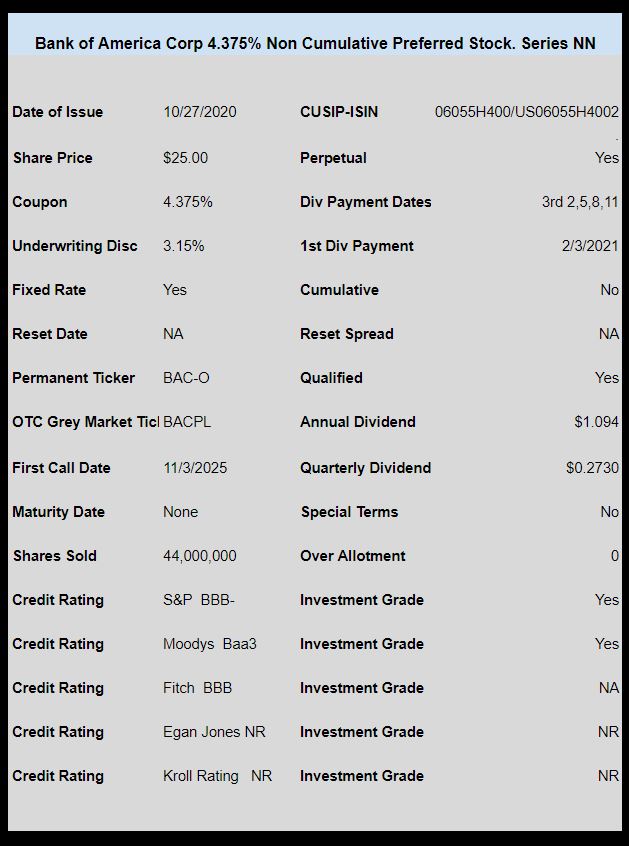

Banker Bank of America (BAC) priced the new issue of preferred stock with the coupon a little lower than ‘yield talk’.

The issue priced at 4.375%. The issue is low investment grade.

The company is selling a giant 44 million shares, and as many people pointed out yesterday, the banker will likely redeem their 6.2% issue (BAC-C) when it becomes redeemable in January. The C issue is 40 million shares so it will require most of the proceeds from this issue.

The issue trades immediately under OTC grey market ticker BACPL.

Giant banker Bank of America (BAC) has announced that they will be selling a new issue of preferred stock.

The company has 11 current preferred issues outstanding ($25/share issues) and 5 are currently redeemable–BUT these 5 are low coupon floaters with current rates of either 3% or 4% so I would be surprised to see these called. The company may well redeem some of their untraded issues or $1,000/share issues.

I mention this (and own it) because it is trading at $25.04-$25.06 and has 2 interest payments until maturity (January and April) for about 41 cents each.

Ready Capital (RC) actually has a 7% convertible note due in 2023 trading around $23.79 which has a better yield, but obviously is 2 1/2 years further out in maturity so has more risk built in.

Assuming financial markets don’t totally implode this seems like a good short term yielder.

Investors should do their due diligence to see if this might be right for you.

The Bank of New York Mellon (BK) will be selling a $1,000/share preferred issue. No listing of these shares will occur. The preliminary prospectus is here.

The bank will be redeeming their series C 5.20% $25/share issue which can be seen here. This issue has been redeemable since 2017–it is likely the redemption date will be 12/20/2020 as it must be redeemed on a dividend payment date.

It is surprising that a bank with a credit rating this high Baa1 and BBB took this long to redeem these shares–investors were lulled to sleep as shares closed last Friday at $25.87 so will take about a 50 cent loss on the redemption.

The S&P500 had a low last week of 3420 and a high of 3502 (just 2.5% from a 52 week high) before closing the week at 3465 which is a loss of about 1/2% on the week–on a relative basis, a quiet week, as investors play the stimulus and election guessing game.

The 10 year treasury continued to creep slowly higher hitting a weekly high of .87% on Friday before backing off a bit to close the week at .84%. Back in June the rate had a spike high in the .90% area so certainly we could see rates bust through this area soon. The range for the week was .76% to .87%.

For some of us this is a bit of a dicey time–low coupon issues would be hurt the most if we were to see rates move above 1%. Remember that ‘speed kills’–a move higher, which is slow–a few basis points a day (or some such move) would be better tolerated that a spike of 10-15 basis points in a day. We don’t ever know the tolerance of income investors for higher rates–but these fast moves can set off some selling. Additionally, it is my understanding that there is a lot of speculation in the interest rates markets based on potential outcomes of the elections–these trades can always be reversed to send rates higher or lower.

The Fed balance sheet grew once again last week with assets expanding by $26 billion after growing by $18 billion the week before–the balance sheet is now at a record high of $7.177 trillion –the previous high of $7.168 trillion was back in early June, before assets dipped down to $6.920 trillion in early July.

The average $25 preferred stock and baby bond rose by 8 cents last week. CEF preferreds were off 7 cents, utility issues were up 11 cents, banks up 4 cents and investment grade were up 9 cents–no giant sector movers last week.

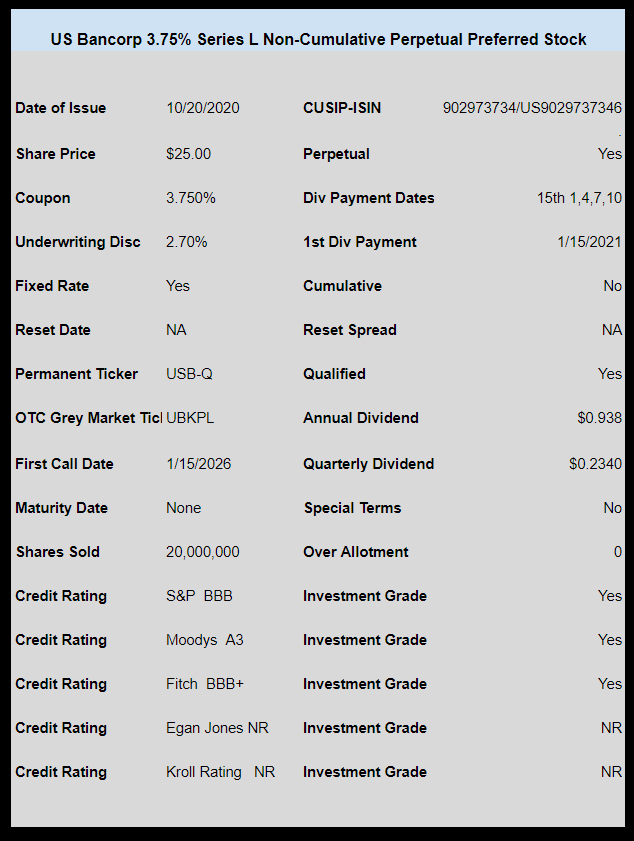

Quality banker U.S. Bancorp (UBS) sold a 3.75% non cumulative preferred which is now trading under OTC ticker UBKPL and closed last week at $24.68.

Banker Wells Fargo & Company (WFC) priced their new issue of preferred stock at 4.70%. The issue is trading under OTC ticker WFCCL and closed the week at $25.17.

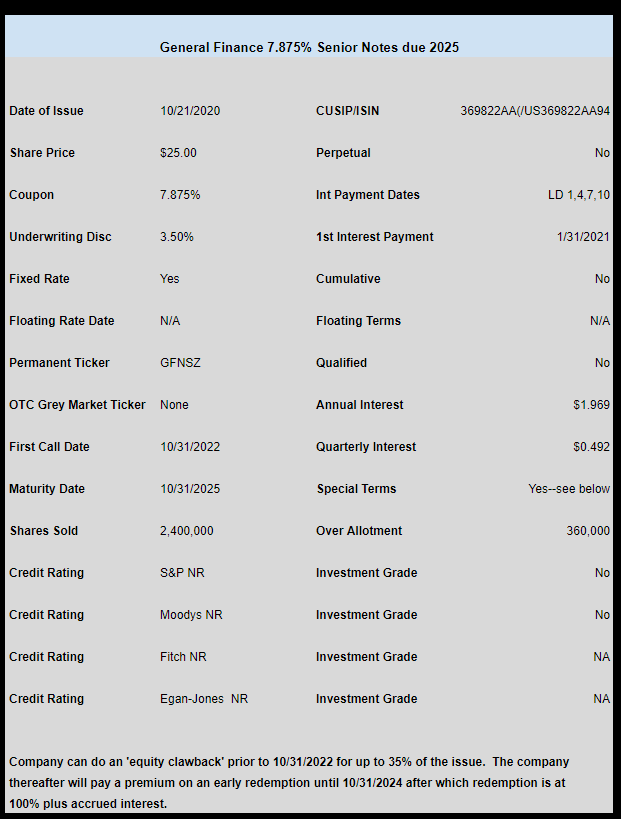

Leasing company General Finance (GFN) sold a new issue of baby bonds to refinance an old issue. The issue priced at 7.875% and as of yet it hasn’t traded.

Pennnsylvania banker Fulton Financial (FULT) sold a low investment grade issue with a coupon of 5.125%. This is the star new issue of the week as it came out of the gate hot hitting a high of $25.70 on the 1st day of trading before closing at $25.67. Shares are trading on the OTC grey market under temporary ticker FULPP.

Nobody is really excited about the plethora of low coupon preferred’s being issued lately, although I see a few folks are buying them–including me.

As I always have to do–I just can’t help myself, I have bought a couple issues lately that I normally probably wouldn’t buy–and I did it as a test–can I squeeze at least 1-1.5% flip profit out of the issues. Right now the answer is not totally known, but of the 2 I have bought 1 has been sold for about a 1.5% flip profit.

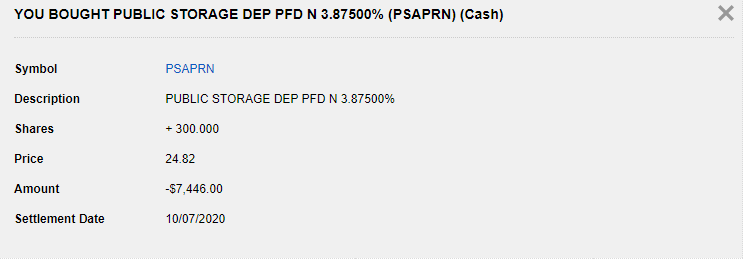

1st off I bought 300 shares of the Public Storage 3.875% (PSA-N) issue on 10/05/2020 for $24.82–the issue had traded as low as $24.70. I fully planned to sell these shares when I hit my target of 1.5%.

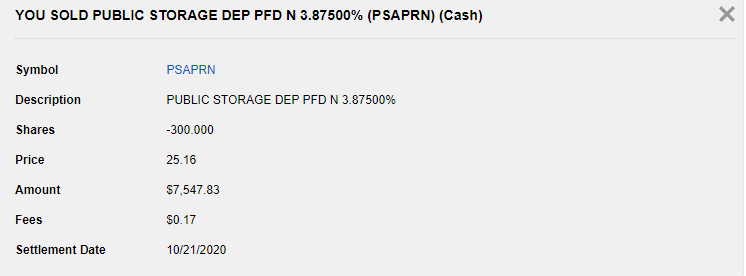

I then sold the issue on 10/19/20 for $25.16 which gave me my 1.5% profit (slightly less actually). That is a ‘steak dinner’ trade, so I am satisfied with my meager profit. I did notice the shares plunged down to $24.85 today for whatever reason.

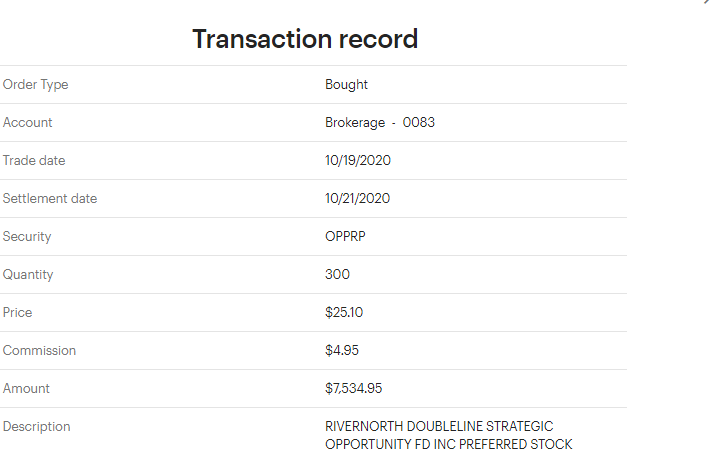

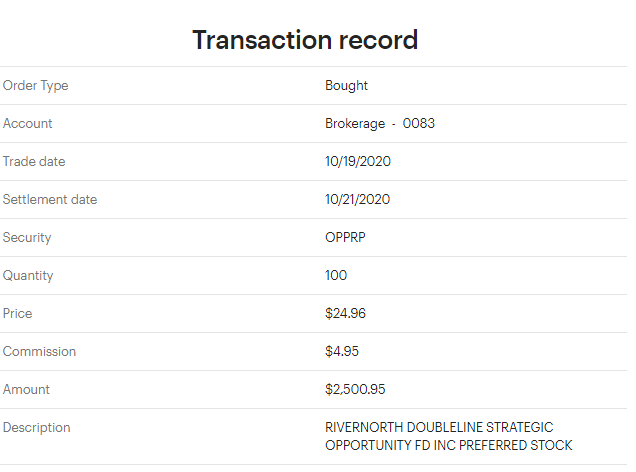

On Monday of this week I began to buy shares in the new RiverNorth/DoubleLine Strategic Opportunity Fund 4.375% preferred. This is a high quality issue and I was too ‘excited’ to jump and buy. I started with a 300 share purchase on Monday for $25.10 and followed it up on Monday afternoon with another 100 shares at $24.96. Should have been more patient.

I now wait to see my next move–it closed at $24.95 today. If it falls from here I will buy a couple hundred more shares. The quality of this issue at a reasonable coupon (in my eyes anyway) means I would be willing to go to 600-1000 shares or maybe higher. I am confident I can squeeze out a 1% flip profit, but likely I want to hold some of this issue long term so I will determine later what I want to hold long term.

So assuming there is not an interest rate spike while I hold these issues it looks like it is probable one can get 1-1.5% quick flip

I am not recommending anyone fiddle around like this–I mean really a short term $100 profit is meaningless in the big picture and I would rather have holdings that are long term. This was a test and a boredom trade.

NOTE–I post the brokerage clips above to display the actual transaction–the top clips are from Fidelity and the bottom from eTrade (also note that eTrade charges $4.95 on the OTC trades.

Pennsylvania banker Fulton Financial Corp (FULT) has announced the intention to sell a new issue of non cumulative preferred stock.

The regional banker, with $24 billion in assets, will sell a $25/share issue with typical terms–non-cumulative, qualified and optionally redeemable in just over 5 years (1/2026).

‘Yield talk’ is in the 5.375% area with a low investment grade from Moody’s.

The issue will trade under FULTP when it hits the NASDAQ.