Nobody is really excited about the plethora of low coupon preferred’s being issued lately, although I see a few folks are buying them–including me.

As I always have to do–I just can’t help myself, I have bought a couple issues lately that I normally probably wouldn’t buy–and I did it as a test–can I squeeze at least 1-1.5% flip profit out of the issues. Right now the answer is not totally known, but of the 2 I have bought 1 has been sold for about a 1.5% flip profit.

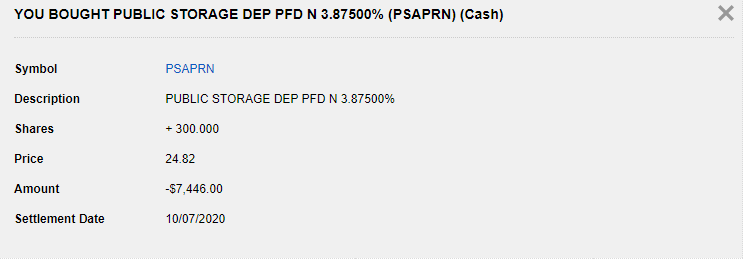

1st off I bought 300 shares of the Public Storage 3.875% (PSA-N) issue on 10/05/2020 for $24.82–the issue had traded as low as $24.70. I fully planned to sell these shares when I hit my target of 1.5%.

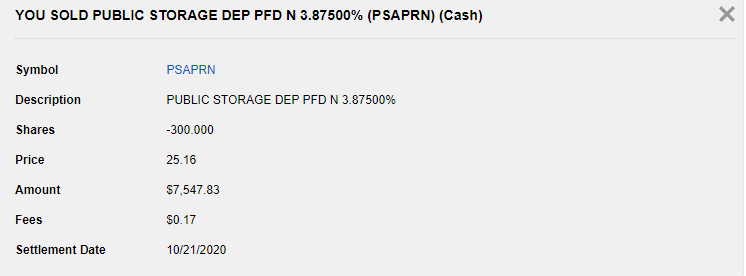

I then sold the issue on 10/19/20 for $25.16 which gave me my 1.5% profit (slightly less actually). That is a ‘steak dinner’ trade, so I am satisfied with my meager profit. I did notice the shares plunged down to $24.85 today for whatever reason.

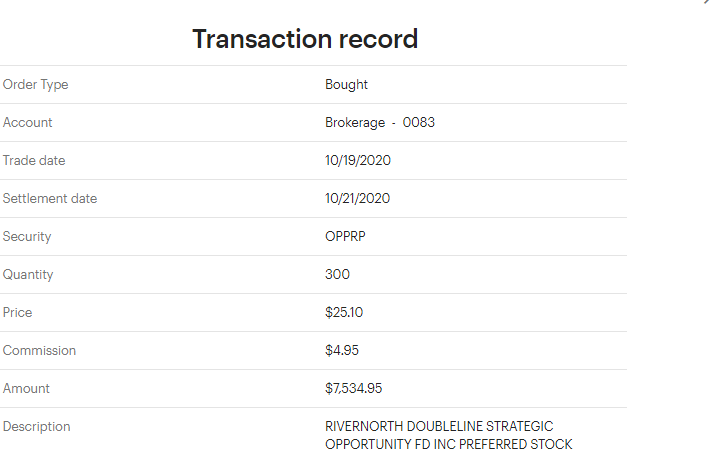

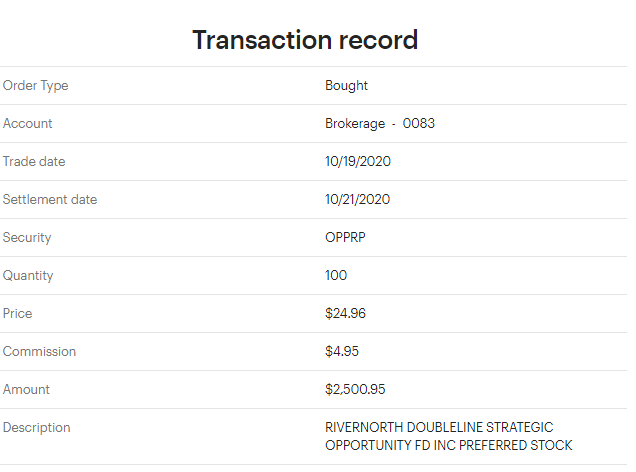

On Monday of this week I began to buy shares in the new RiverNorth/DoubleLine Strategic Opportunity Fund 4.375% preferred. This is a high quality issue and I was too ‘excited’ to jump and buy. I started with a 300 share purchase on Monday for $25.10 and followed it up on Monday afternoon with another 100 shares at $24.96. Should have been more patient.

I now wait to see my next move–it closed at $24.95 today. If it falls from here I will buy a couple hundred more shares. The quality of this issue at a reasonable coupon (in my eyes anyway) means I would be willing to go to 600-1000 shares or maybe higher. I am confident I can squeeze out a 1% flip profit, but likely I want to hold some of this issue long term so I will determine later what I want to hold long term.

So assuming there is not an interest rate spike while I hold these issues it looks like it is probable one can get 1-1.5% quick flip

I am not recommending anyone fiddle around like this–I mean really a short term $100 profit is meaningless in the big picture and I would rather have holdings that are long term. This was a test and a boredom trade.

NOTE–I post the brokerage clips above to display the actual transaction–the top clips are from Fidelity and the bottom from eTrade (also note that eTrade charges $4.95 on the OTC trades.

i think this is exactly why it’s a dangerous time in the preferred markets. Sub 4% issues are going near par, 4-5% issues are considerably above par and anything with a higher coupon than that usually has a poor company behind it so it doesn’t fit a conservative investing style. Meanwhile the S&P 500 index has already returned more than 8% this year and while yes, that can change i’m (partially) an income investor who doesn’t want to be stuck with these near 4% preferreds in a few years when we are likely to see higher rates and inflation. If you’re holding forever you’ll be fine, but if not, those share prices are going to plummet and good luck getting rid of illiquids at that point (if you need to). I think the better play now is cutting back on preferreds and picking up some high quality stocks for their dividends. When the market crashed i picked up Coca Cola for a 4% yield as one example, AVGO above 4% as another. Blue chips with low payout ratios and capital appreciation. It’s just my opinion/view but I’m very leery of the preferred market right now and as some of my issues are getting called i see no preferreds to reinvest them in.

Up until now, increases in the ten year rate are generally viewed as bullish even for preferreds because it signals expectations for recovery. At what level of ten year rates does the traditional inverse relationship begin to control? 100 125 basis points? Given that so many issues trade above liquidation or stated value, the risk/reward for increases seems to have greatly shifted.

Does anyone else find it strange that ten year rates in Europe are jumping in the mid of the “hockey stick” jump in daily covid cases? Ten year rates have doubled in Britain in the last ten days despite the onset of high numbers in the UK.

I’m just not buying at these coupon levels. I feel they are “zombie” issues that will never be redeemed, the cost of capital is so low and when interest rates inevitably rise their value drops pretty sharply. Market shocks seem to happen every 12-24 months, I would for the next one and then look for values.

I understand that if you are a “buy and never sell” investor and these coupon rates get you what you are looking for, the risk to value doesn’t matter, and I respect that point of view.

Tim—I agree with you that interest rate shocks seem to come around every year or two. I want to have some cash available to take advantage when it occurs. I guess I’m willing to earn nothing on that cash in the meantime. I just don’t want to be locked into issues yielding under 5% when interest rates spike—and they eventually will. The question is—when? Since I’m in my 70’s, I might have gone through “the door” by then, but who knows?

Not buying many of these I don’t want to catch a falling knife trying to make a small profit. Forcing me to look at issues slightly above par that essentially have a floor under the price they are already held down by call risk.

read with interest all the discussions on low coupon issues. I went thru the same thought process a while back on 2 psa’s I bought then at 4.70 & 4.9% which I considered marginal at the time. Not being a flipper I had to be satisfied with the coupon and possible loss of principle “for the duration” as calls are not baked in, even though that’s PSA’s history. Politcal and Fed policy change, not to mention if the crap hits the fan, sure makes Draft Kings or something the like it “the new normal”.

mike–I prefer to hold long term–just a test, partially from boredom. I’m not a flipper either except on occasion. My preference is buy and hold for a long time.

Martin G–I’m not buying much, but testing the waters for a little flip profit–but the risk reward is not very good.

I had a friend grinding me about the low mm acct rate. It was like 0.10%. He’s a mouthy type who doesn’t mince words or shy away for telling you how he feels.

So we bough a slug of 1 pfd. Sold it six weeks later net 4.2%……..if he held it it kept going but that’s irrelevant. I called him and said “You just made 42 years of mm interest in six weeks now shut the F up”

If you Prefer–all about the risk/reward and we all know you can’t live off mm rates.

Tim, it is fine to flip issues like these but we need to make sure less experienced investors understand the risks of very low coupons like PSA-N @ 3.875%. If interest rates increase in the next five years before it is callable, it will drop more than issues with higher coupon rates. It is simply the math of fixed income investments and is not a knock on PSA. Stated differently if you buy PSA-N with the intent of holding it long term, you have implicitly bet that interest rates will not increase. And yes if you do not care about what it is trading for, the dividend is highly secure. Just don’t try to sell it or you might lose more than you made in five years of interest.

Tex–that is why I mention ‘assuming no interest rate spike’. All depends on goals and needs. The risk reward is not good on these for a ‘flipper’–make $100 but risk an interest rate increase while held–not really a big enough reward.

I think you need to consider one important factor….are you an investor looking for return or are you an income investor looking for yield and consistent income?

If you are an income investor with capital preservation as one of your top priorities, an A rated, 3.875% coupon looks pretty darn good and a definite buy and hold for the next five years of zero or negative interest rates.

Richard–correct–that is why I will hold some of the OPP issue for a long , long, time.

Tim,

We have no idea where rates are going over the long term. Myself I don’t like the mm rates being offered so I took a different tack.

Recently they called a portion of CTZ I took what I considered a risk and bought 200 shares @ 24.95 with the thought that it might be a while before they call the rest. Even if they did call it I bought below par. Friday I was notified Qwest is calling the balance at 25.19 on Oct 26th.

So I got a whole .24 or 48.00 for about 1 month. Here that might be a chicken dinner, Ha. Now it leaves me looking for a new preferred, which I think is going to be another one close to call.

That is going to be my solution to my boredom

Consider MNR-C, callable 9-2021, ex-div 11-13, 4 divvies til first call, a dime under par.

Timdman….Shushs .Not so loud! Almost my largest position and considering adding more as I expect MNR to come out with a follow-on preferred some time in the Spring to cover calling the C series as they have done in the past.

I have been buying MNR-C for this precise reason. I also feel they will issue a lower coupon preferred sometime in the near future, and call in MNR-C.

Besides, buying this below par takes away any call risk, and one enjoys a good yield in the meantime.

Their largest customer Fedex, is not going away any time soon, their ongoing and future business outlook remains strong.

Charles – For probably a shorter term spec on being called, how about BRG-A 8.25%? It closed at 25.20 and has about .17 of accrued. They already called about 25% of the issue on 10/21 and have a 30 day call notice rule so it will remain outstanding at least until 11/26 however I suspect that given their 10/21 call, these will remain out until sometime early 2021, but that’s my pure speculative assumption… As far as pinned to par type cushion, compare to BRG-C = 7.625% that closed at 25.60 with 7/19/21 call and BRG-D 7.125% with 10/13/21 closed at 25.41. So A is certainly trading in anticipation of a call but still seems cheap with no downside risk as a short term money mkt alternative. The other two might work too….They might not offer as juicy a return as your CTZ score but still something to consider..

It is worth checking out Quantum Online for the differences between BRG-A and BRG-C on the one hand and BRG-D on the other. The A and C issues each have dates (10/22 and 7/23 respectively) after which they start to pay a 2% higher penalty rate if not called, and holders of those issues are able to put their shares back to the company for $25. BRG-D doesn’t have those features, so I imagine it is likely to remain outstanding the longest of the three.

I have also been adding to long positions in BRG-A and BRG-C.

Mike – Actually it’s worth checking out the prospectuses given the headsup QOL gives you… lol.. I agree… I only pay attention to A and A because of this feature but mentioned D as an indicator of how much of a cushion is provided in the mkt price of A right now vs what “par” might be were they to issue a new series… Both A and C represent great examples of pinned to par securities that can provide mm alternatives with minimal risk…. As far as security risk itself, I take even more solace in knowing BRG was in the market buying BRG-A when the fan was getting stained brown.