All too often I forget that so many of the visitors to the website are new to investing in baby bonds and preferred stocks. Many of us have favorite sectors that we like to invest in–maybe banks, REITs, utilities, business development companies (BDC’s) or maybe it is in the closed end fund (CEF) arena.

Myself I pretty much go wherever I can attain my modest 6-7% goal of total return. I can and do invest in almost every sector, although it has been a long time since I have owned any of the shippers.

But now I want to review in a relatively brief way the Specialty Finance companies—which are closed end funds that hold primarily Level 3 assets. Most of you you know that Level 3 assets are defined as ‘value cannot be determined by readily observable inputs or measurements’. There is no marketplace where these assets are traded so value is estimated. I like to call these ‘trust me’ values—‘trust me’ because the company is telling you what their assets are worth based upon estimates and models–you have to simply trust them.

The company’s that I am talking about here are primarily the owners of CLO’s (collateralized loan obligations). CLO’s are Level 3 assets. Holding only Level 3 assets means that there is a higher level of risk to the investor. If a closed end fund holds only Level 1 assets (i.e. stocks) we can look at a firm number everyday and know what their assets are worth–this is why the preferred stock and baby bonds of issuers like Gabelli are investment grade rated.

In particular Eagle Point Credit Company (ECC), Eagle Point Income Company (EIC), Oxford Lane Capital (OXLC), Priority Income Fund (not publicly traded), OFS Credit Company (OCCI) and to a lesser degree XAI Octagon Floating Rate and Alternative Income Term Trust (XFLT) are what I call the Specialty Finance companies.

DISCLOSURE–I hold preferreds and baby bonds from ALL of the above company’s–excepting Eagle Point Income which currently has no baby bonds or preferreds outstanding.

Here is what I look for in investing in these specialty finance CEF’s.

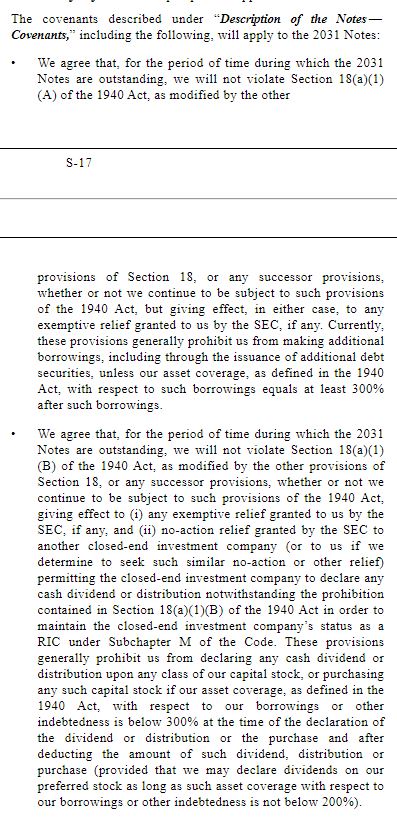

Leverage–these companies all use leverage–they sell preferred stocks or baby bonds to raise more money which they then invest in more CLO’s–obviously they intend to make a return in excess of their cost of capital. These companies must have asset coverage ratios of 300% for debt and 200% for preferred stocks–these are minimums. For example here is a ‘snip’ from a prospectus for a issue of Eagle Point Credit Company baby bonds.

You can see that it spells out that the asset coverage must be at least 300%. If the asset coverage falls below this level they may not pay common stock dividends. These companies exist to pay high dividends so you can be certain they take this very seriously. Note that the preferred stock dividends can still be paid as long as the asset coverage ratio is above 200%.

Why is this important to me? I want maximum coverage–I want to sleep at night–I don’t want to hold the common stock–I want the ‘senior securities’ (preferreds or baby bonds) that have a claim on the assets before the common holders. Of course the baby bonds have 1st claim with the preferred holders 2nd–and then the lowly common holders. Let the common shareholders take the mega risk.

The leverage level is important to me because I don’t always trust management to have their Level 3 assets valued correctly–but if there are $3 or $4 of assets for every $1 of senior securities (preferred or baby bonds) there is an implied level of safety in liquidation.

Ability to Raise Capital–I want the company to have the ability to continually sell common shares. These company’s burn through a lot of cash–normally paying huge dividends to common holders. They also have substantial bad loans–CLO’s are packages of lowly rated loans which pay high interest rates and with high rates high risk is implied. I want the total assets of the company to grow–I don’t care so much about the net asset value/share–I just want the total asset base to grow based on fund raising by selling common stock–this keeps the leverage ratio up. If the NAV/share falls that is the common shareholders problem–not mine–the NAV can fall while at the same time the coverage ratio can increase.

An Example

From my observation Oxford Lane Capital Corporation (OXCL) is extremely good at raising funds. For the quarter ending 6/30/2021 they sold 7.6 million common shares with net proceeds of $53.8 million. The company now has 108 million common shares outstanding. I looked back to 4 years ago—9/30/2017 and the company had 25 million shares outstanding at that time. They are really good at selling common shares–every quarter.

Here is a chart of the Oxford Lane Capital Corporation common shares going back 10 years.

This charts shows 2 things–1st that the share price has fallen by around $15/share in the 10 year period and 2ndly that the trading volume goes up and up–as they raise more capital by selling common shares trading volume follows. Do I care that the share price is falling? Not so much, although if it went up it would be better for the common shareholders as a senior security holder I care about the asset coverage ratio which currently stands at around 237% (last time I calculated it). Now it needs to be understood that OXLC pays a dividend to common holders of around 10% so the total return on the common is not as bad as it looks on the chart and in order to remain qualified as a Registered Investment Company (RIC) they must pay out at least 90% of their investment company taxable income each year.

Notice that nowhere above did I mention reviewing the financials (i.e. income statement and balance sheet) of the company. The asset coverage ratio pretty much outlines how the company is doing, but just the same you need to minimally review the updates each company publishes. Here is a link to the most recent Oxford Lane update on 7/30/2021. To try to go into the income statement and balance sheet of these companies is pretty fruitless for most folks–but certainly if one has the accounting abilities these financial statements should be scrutinized.

I would not own the common shares of any of these company’s–honestly even with a 10% dividend the total return is pretty poor.

Would I own these preferreds and baby bonds if we were heading toward a steep recession or depression? Because of the marginal quality of the underlying companies I would avoid these if I though we were heading toward poor economic times, but the government seeming to bailout everyone the risk has been minimized recently.

Would I recommend anyone in particular buy the preferred stocks and/or baby bonds of the Specialty Finance company’s? NO because I never recommend anything to anyone because I have no knowledge of the ‘suitability’ of any given investment for anyone.

MG:

CDO ,read D’s , Debt, were the major factor in 2008.

There is a very good article, prob easy to find, by Steve Bavaria, prob on SA regarding CLOs and CDOs. Made an impression on me to know the distinction. Nice to have electronic media as an investor’s tool for research these days. I’m too lazy to go an find it to post the link here.

Caveat: Steve B is controversial regarding his high income methods, but the article is pertinent: Jan 2021:

https://seekingalpha.com/article/4399934-clos-for-dummies

OK Alot of people have helped me here at III so I went and got the link.

ChinChin

MG:

I dug myself a hole by being lazy. I just rescanned that article I linked above. Apparently, that is NOT the one that compares and contrasts CLO/CDOs. I have a hard time with instant recall on that stuff. I went to a general search and ended up on Investopedia, which DOES give a nice recap of the derivitive build up into 08-09 with CDO’s.

https://www.investopedia.com/terms/c/cdo.asp

Both are prob worth time if in those instruments.

All the Best, JA

Thanks Joel – yes Steve B isn’t for me–but to each his own. But the article is good.

Tim, Thank you for posting. Re: “These companies must have asset coverage ratios of 300% for debt and 200% for preferred stocks”. Where would I be able locate where the company stands in terms of the coverage or how would I calculate ?

Take a look at https://innovativeincomeinvestor.com/closed-end-fund-asset-coverage-determination/ (thanks Tim!)

” the company is telling you what their assets are worth based upon estimates and models–you have to simply trust them.”

Is that only true of the monthly estimates company’s provide? I thought the quarterly 10-Q NAV would have to be verified by a “third party” (which isn’t as independent as it suggests but better than company estimates).

Landlord–in reading the various semi annual and annual reports it states that they have engaged a ‘third party’ which is just a portion of what goes into determination of the NAV. So they ‘consult’ with someone else. Whether there is a requirement or not it appears doubtful–to be certain I would have to read the entire 1940 act I guess.

Dug into the 1940 Act and it simply states that the board of directors is responsible for determination of the NAV when observable inputs are not available. I’m sure there are more (newer) rulings on this somewhere.

Tim:

Regarding your comment, “Ability to Raise Capital–I want the company to have the ability to continually sell common shares”

So how does an investor go about buying or selling shares in the actual Priority Income Fund? Does PRIF just use their broker affiliate to sell shares privately to investors like some of the private REITs?

Just trying to figure out what would happen to this fund (and its preferreds) if the CLO market tanks. Thanks!

Rob–they are sold primarily through advisors which deal in alternative assets investing. Priority is managed by Prospect Capital (PSEC). They do file normal reports with the SEC so you can review their data–here is the latest annual report from 6/30/2021.

https://www.sec.gov/Archives/edgar/data/0001554625/000155462521000164/pris2021q4n-csr.htm

This is very much a ‘trust me’ company–like most of the CLO companies. If one can depend on their financials they have done better than most of the others.

CLO’s were a major factor in the 2008 housing crisis. A once in a lifetime event because housing prices never drop 40%. Until they do.

We haven’t solved the problem of CLO’s. Now we’re in another housing bubble. This time we have inflation which could prevent housing price from dropping much even in a downturn. If not, then look out below.

Martin G,

Back in 1989, I had a mortgage from Weyerhouser the plywood company.

It was for 10.5% on a loan of 150k

Brand new custom built home was $179k.

It now is worth 560k on Zillow.

The point I haven’t made yet is, When interest rates go up, the purchase price comes down. I expect a lot of seller financed homes will be the answer for many.

I thought CDOs were the primary cause of the 2008 housing crisis, not CLOs.

That was CDOs not CLOs that were behind the 2008 bust. CDOs are mortgage securities while CLOs are corporate loans and CLOs performed okay in 2008. CLOs are considered to be significantly more diversified in their economic exposure than CDOs.

As others noted,CDOs were the problem. Other authors have stated many times that CLOs came thru pretty well.

Also- other authors have said that CLOs have have had relatively low losses- contrary to what Tim is saying- as far as risk.

Steven Bavaria has a good grasp of them- and several articles.

Gary–losses are low is a relative statement. For now we do not know how they will act in a long ranging and deeper recession as we have had artificail stimulus to the economy (i.e. bailouts) for more than 10 years now and most of these companies are only 10 – 12 years old.

Agreed.

Some further info:

Some did quite well in ’08+, and opportunity in sell-offs – as in 2020 :

https://seekingalpha.com/article/4439462-ecc-continues-to-ride-upward-momentum-in-clo-market

Possible 10 yr low in defaults:

https://www.trepp.com/trepptalk/the-sustained-growth-of-the-global-clos-market-and-the-1-trillion-milestone?utm_campaign=TreppTalk%20Subscription&utm_medium=email&_hsmi=139050217&_hsenc=p2ANqtz-_EdsrXxc4eD_HiiUe7T-nb2qA2uS-NvLNYgfcDP4KcbD_bdbnKRlJX61VA5GdfjGDb6gHHXY47dBn4MbAXHlHiqlBiPw&utm_content=139050217&utm_source=hs_email

Gary–Eagle Point seems to be the brightest of the bunch. Reviewing OXLC they took some giant ‘realized’ losses. While I can’t cover everything in a short article we should all be reminded that most of these companies hold ‘equity’ tranches of the CLO’s–the 1st to take losses and highest risk. That is one reason I have been anxious for Eagle Point Income (EIC) to come out with the term preferred previously announced as they hold mostly ‘debt’ tranches of the CLO’s—how does the market value a term preferred from a CEF holding mostly ‘debt’ tranches versus the ‘equity’ tranches.

Like the BDC’s I am quite anxious to see how these companies perform in a ‘real recession’–one in which not everyone is getting PPP money etc. Maybe we will never know (in our lifetime) if bailouts become the norm.

Tim,

Not enough time in the day to do the day job and the research, but I did read Steve B’s article over on SA and the comments. Seems while the CEF stock can vary in price and distribution the preferred holds up better on price and recovered faster plus the dividend didn’t change unless its suspended.

But if interest rates rise ( yes I know one camp says overall debt is too high to allow interest rates to rise ) Then a preferred stock can drop in value.

The recent uptick in 10yr got people excited, but it passed.

Personally I am good with the return I am getting on my FF CUBI-PE and PF even if I am 5 to 10 cents underwater and the volume is very low so not a lot of sellers.

I still remember the early 80’s rates spiked and unemployment went up and economy stalled, but people still had to eat, keep the roof from leaking and in general floods, tornadoes and hurricanes and freezes kept a good number of people employed

“Also- other authors have said that CLOs have have had relatively low losses-”

In the Covid Crash, AAA rated CLOs were trading at 90 cents on the dollar. That implies that most CLOs were worthless. Perhaps the market was totally wrong about the amount of risk in those securities at that time or perhaps they were headed to doom were it not for the bailout. I can understand not wanting to stick around to see the answer to that question.

Another point is that CLOs are comprised of sr loans and they don’t make sr loans like they used to. Back in 2008, sr loans came with covenants, more cushion from subordinated capital, and stronger underwriting (the underwriting hanky panky was in mortgages). Today sr loans are riskier and comparisons with the past not necessarily valid.

CDOs on the other hand, backed by hard residential real estate, are possibly the safer bet at this time. Mortgage industry is once bitten, twice shy.

Thank you.