The S&P500 moved higher again last week–but just by the smallest of amounts–1.5 S&P points. The entire range for the week was only about 2% which is a pretty tight range. With only somewhat minor economic news being released and with earnings season over there simply was no stimulating data.

The 10-year treasury closed the week at 4.47% which was up from a close of 4.42% the previous Friday. The interest rate moved in a 19 basis point range on the week. We did have bunches and bunches of Fed yakkers last week, but at least their messages have been somewhat consistent–higher for longer and data driven.

Last week we had the S&P Purchasing Managers Index (PMI) come in somewhat hot, while 1st time unemployment claims continued to show relatively strong employment as claims were under forecast and under the last reading.

This week we are likely to have more active markets–at least at the end of the week as we have the personal consumption expenditures (PCE) data being released on Friday–we could see sizable reactions in both equity and interest rate markets.

The Fed balance sheet moved lower last week by $5 billion. We are not likely to see large weekly drops now that the ‘runoff’ rate set by the Fed is $60 billion/month versus the previous $95 billion/month.

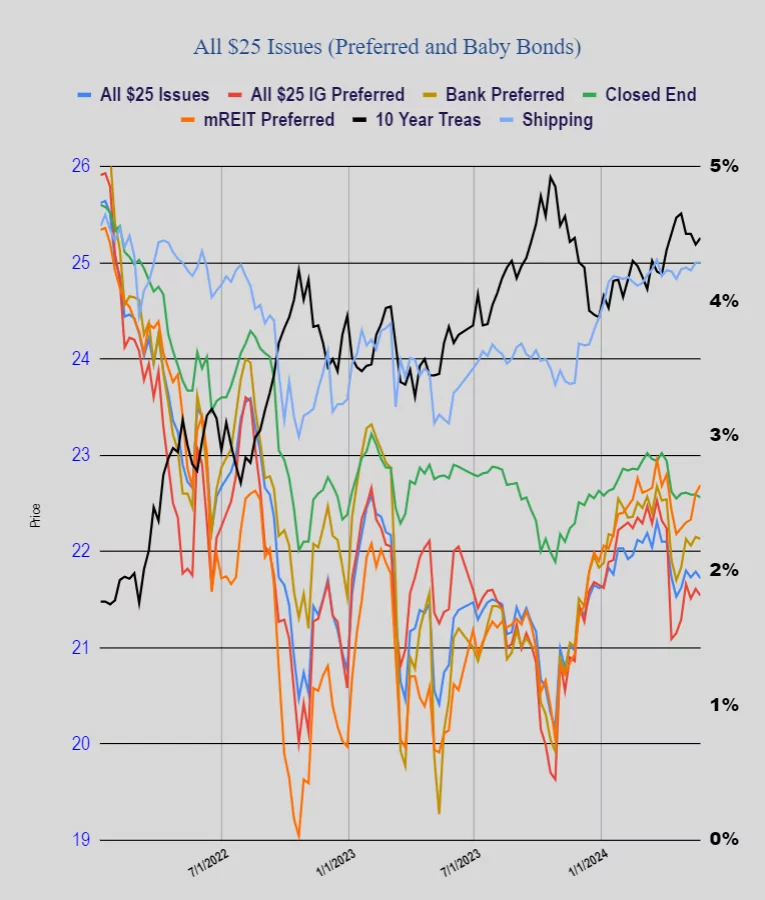

The average $25/share preferred stock and baby bond barely moved last week, but did end up down by 7 cents. Investment grade issues fell by 7 cents, banks were off 2 cents and mREIT preferreds moved higher by 9 cents. All in all a very quiet week.

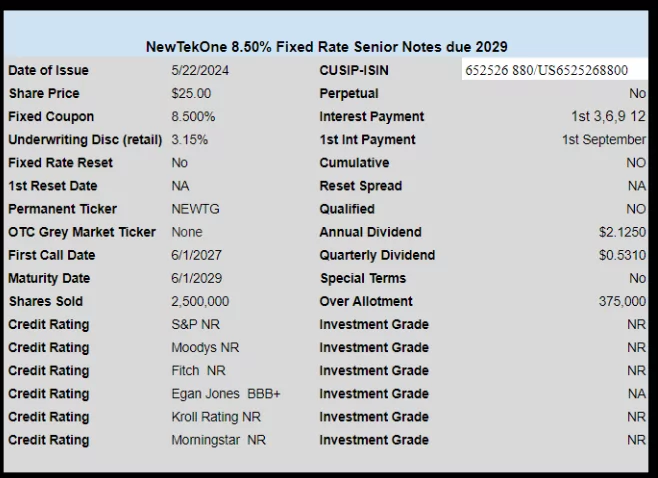

Last week we had 1 new income issue priced as NewTekOne priced a baby bond with a coupon of 8.50%. The issue may trade later this week.

I have a nice sized 5.2% CD maturing tomorrow. Was contemplating putting those funds to work in a preferred or BB but might just roll to a 5.5% CD. It looks less likely interest rates come down any time soon and, in fact, some are suggesting another small hike. We shall see.

CFG D called in full July 8th.

CIMN 9% trading today. Last $24.69

9% coupon yet still falls quite a bit under par. People are definitely not rushing to pick this one up. Lets see what it does over the next several days.

So Tmobile makes a spectrum move with USM. TDS trades down in news. Shows you how dumb wall street can be, seeing TDS owns usm. Cash injection a big positive.

Now the ftc stands in the way. Without the cash usm and TDS were not long for the world.

Did my portfolio analysis this long weekend; cash mostly in SGOV 47% down from 53%; pfds 20% up from 15% in April; stocks 7% up from 5%; Energy 13% up from 10%; gold miners/royalty co’s; 13% down from 15% (took some profits here in the big runup.)

Cash has fluctuated from 45-58% last few years; I would allocate more to energy at the right price and pfds. All the income coming in monthly/quarterly w/b reinvested and allocated; also dump the SS pmts into SGOV and pfds 7-8% yielders when the price is right; booking to capital and preserving it is rule 1 for me and then trying for 8% yr. GLTA this short week. Bea