Well finally we get by the holidays for a while – with all the market players getting back to work we will likely soon see more wild moves in the market. Santa made December a very good month for most all sectors–will January take away some of those gains.

The S&P500 moved 1/3% higher last week over the previous Friday–the low was 4736 with the high around 4793–closing around 4770. It isn’t that often that we seen stocks trade in a range of just over 1%.

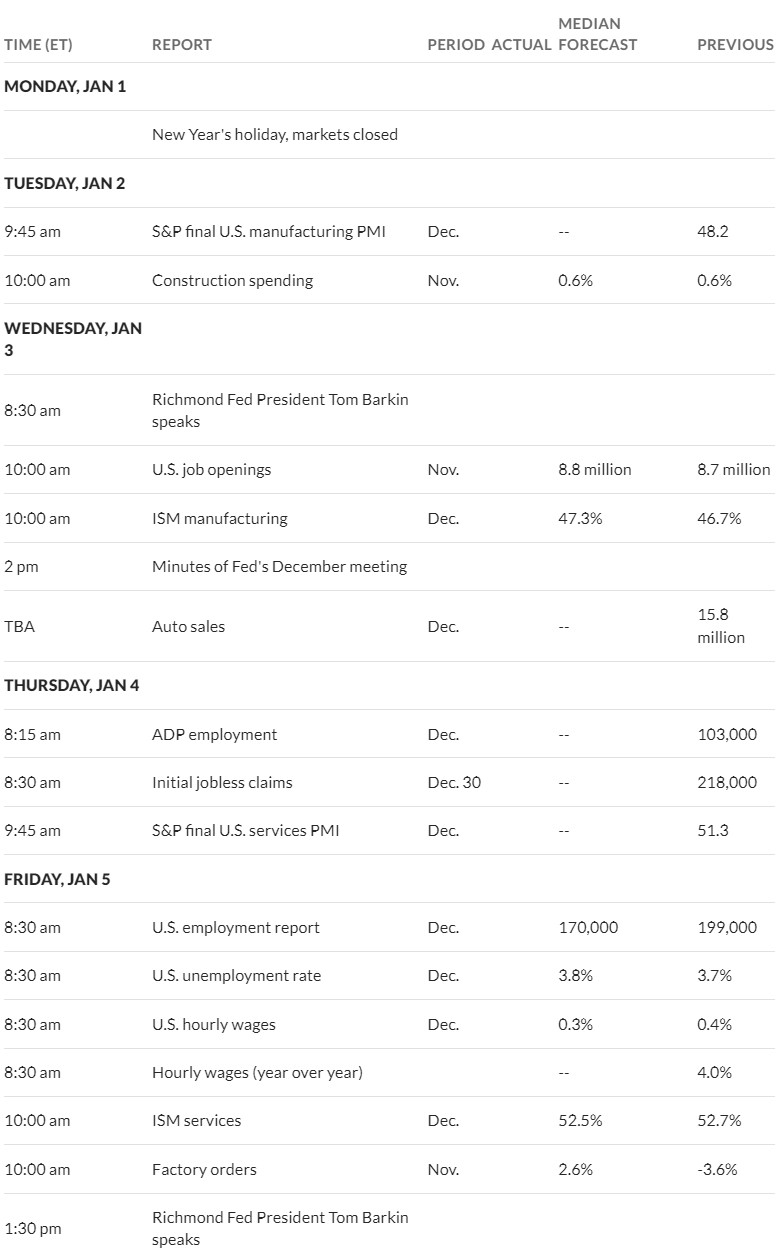

The 10 year treasury moved in a range of 3.79% to 3.91%–closing at 3.87% which was 3 basis points lower than the close the previous Friday. Just like stocks we may be in for more wild action in the coming weeks–we do have the job openings and turnover report on Wednesday along with the ADP employment report (seemingly now being taken as ‘important’)–also the minutes from the Feds December meeting. Then on Friday we have the ‘official’ government jobs report which will be heavily scrutinized.

The Federal Reserves balance sheet fell by $11 billion–that makes a fall of just $25 billion in December–we will see a big swoosh down in the next 2 weeks and the run off plays catchup to the $95 billion monthly target.

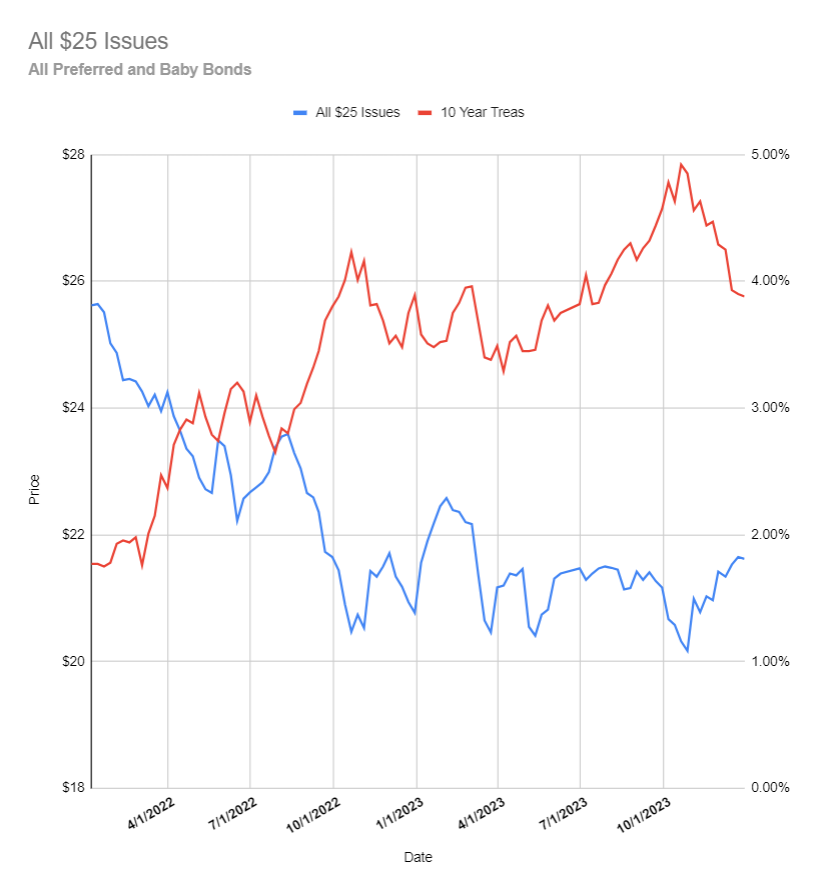

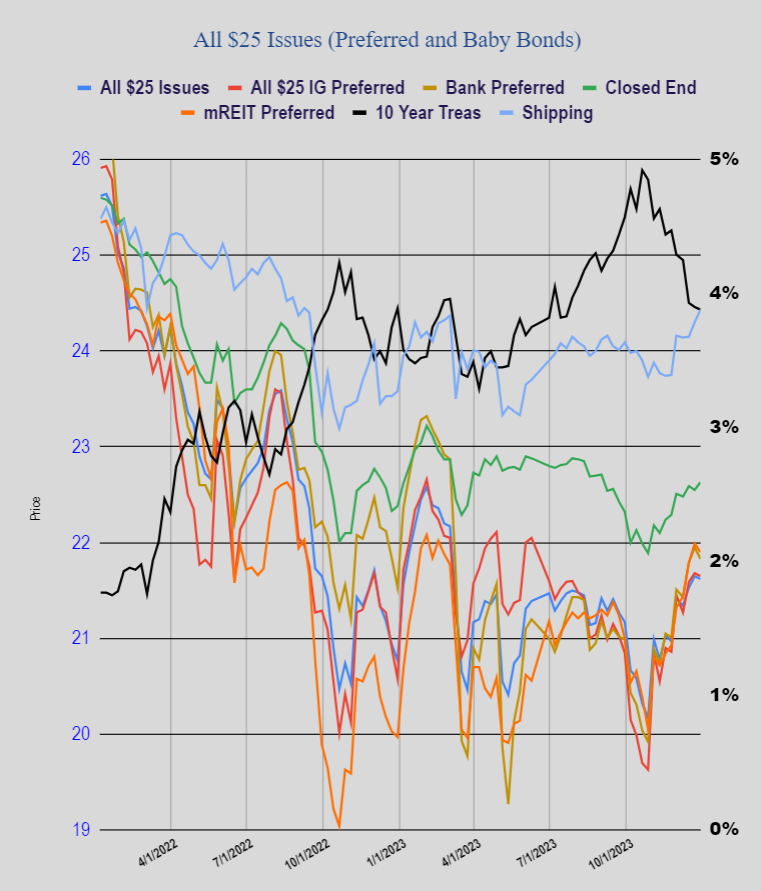

The average $25/share preferred and baby bond moved little last week–down 5 cents. Investment grade moved 3 cents lower with banks down 12 cents. mREITs were off 9 cents while shippers seemed to be one of the few ‘green’ sectors and were up 13 cents.

I present the data in 2 charts–the 1st showing the average share against the 10 year treasury. The second chart showing various sectors against the average share and the 10 year treasury.

Last week we had no new income issues priced.

Below is where recent new issues ended 12/29/2023.

I am becoming increasingly concerned about the Chinese and Kingdom of Saud’s relationship and the US companies pulling out of oil projects internationally:

Chinese private refiner Rongsheng and Saudi Aramco (TADAWUL:2222) are in talks to buy 50% stakes in each other’s refining units, the Saudi-run SASREF and the Rongsheng-operated Ningbo Zhongjin Petrochemical company.

– US oil major ExxonMobil (NYSE:XOM) has formally exited the West Qurna-1 oil field in Iraq and transferred its 22.7% stake to BOC and Pertamina, as well as handing over operatorship to China’s state-owned oil firm PetroChina.

US Oil Output Starts to Decline. According to EIA figures, US crude oil production fell to 13.248 million b/d in October, the first monthly decline since April even if the month-on-month change was a mere 4,000 b/d, with all tight oil plays posting increases expect North Dakota.

ADNOC Eyes First LNG Supply Deal. ADNOC, the national oil firm of UAE, and China’s utility major ENN (SHA:600803) are close to signing a preliminary deal for the supply of 1 million tonnes LNG per year for 15 years, the first deal from ADNOC’s Ruwais LNG project, expected to be launched in 2028.

Mexico Orders Pemex to Take Over Hydrogen Plant. Mexico’s government has mandated that the national oil company Pemex take temporary control over Air Liquide’s hydrogen plant located within the confines of the Tula refinery, calling stable hydrogen supply a “matter of public interest”.

Thanks for the article AB. Saudi Arabia among 4 other nations has now officially joined BRICS. Another 20 nations are in line to join sometime in 2024. Despite US continued arrogance involving the hegemony of the US dollar as the worldwide reserve currency, I have definite concerns also. Were Powells recent dovish remarks a way to merely lower US borrowing costs while he still could ?

Hi Pete, here is an interesting write up about the US Dollar is the world reserve currency https://wolfstreet.com/2024/01/01/status-of-us-dollar-as-global-reserve-currency-and-usd-exchange-rates-long-slow-uneven-decline-continues/

I am very long/overweight metal/Bitcoin and oil at hedge the dollar

All the very best for profitable investing, A

Thanks for another good read. It was particularly interesting to read some of the comments such as:

The dollar is backed up by the full faith and credit of America’s nuclear arsenal and America’s system of laws. Russia and China have a lot of nukes, but corruption is so rampant, only a fool would have any faith in their currencies. We also have corruption, but we are wearing the least dirty shirt.” And

“The “least dirty shirts” might be gold, Bitcoin, real estate, commodities, and other alternative assets. All we know for sure is the USD will lose at least 2% purchasing power per year, maybe 9% in bad years, as recent years have clearly shown.

In my opinion, it’s prudent to allocate a percentage to alternative assets given the Fed’s past eagerness to artificially stimulate markets. In the near term, the Fed might reduce interest rates, reduce pace of QT, extend bank emergency lending lines, or initiate other maneuvers as part of its misguided attempt to achieve a no-recession landing. Such dovish posturing on its own could reignite inflation expectations.

I am probably 63% in real estate, 35% UST and CD, 1.5% precious , and .5% misc. I have avoided Bitcoin simply because I do not understand it. AB would you care to expound more on Bitcoin? I would like more precious metal but the price has run away from my comfort zone

Pete,

I understand bitcoin reasonably well (a couple of my colleagues and I used to lecture at universities in several countries on blockchain and cryptocurrencies for about a decade pre-pandemic ) and we won’t own bitcoin or other cryptos.

I would feel a lot more confident giving my money to Gridbird to gamble at the sports betting window than to put it in crypto long term.

Ha, Private. It was great cleaning up at the window for about $1500 on the Cotton Bowl and a nice little $125 win on Michigan last night. But the NE Patriots smoked me for $1250 on a 6.5 season win over total bet. That was a stinker, but I hope to get most of that back if Atlanta Falcons dont make the playoffs. If they do there is another loss….Up and down, sounds just like bitcoin doesnt it, ha.

I have never invested in the Bitcoin Beanie Babies, but freely admit I could be missing out bigly. But doubt I ever do participate, as you probably have forgot more about blockchain/crypto than I ever learned or comprehended to begin with.

Cryptos are pretty bizarre, Gridbird.

they only have value because a group of people believe they are valuable. There is absolutely nothing backing them – no assets, no “full faith and credit” – (pay no attention to the man behind the curtain).

To me, timing the key to playing cryptos, just as it is in playing in a ponzi scheme: figure out the real game being played, get in early, ride it up hard, then get the hell out before everyone else figures it out.

But, as you well know, I have been wrong before about a lot of things, a lot of times and I could be completely wrong about this too.

A couple of years ago, a big player in crypto tried to recruit a good friend of mine as their CTO. He talked to a bunch of people, including some real technical experts and I helped him talk to some professors I know.

His observation was that most of the folks he talked to fell into one of two camps:

-the academics, who generally scratched their heads about the hype around cryptocurrencies, and

-the true-believers who carry on about crypto like it is a new cult.

Not a lot of middle ground.

He ended up doing some consulting for the company that tried to recruit him, but he ultimately took a job with a fin-tech company.

Wasn’t part of the original premise behind bitcoin that somehow or other, no matter what the value of a single bitcoin might be, you would be able to walk into your neighborhood 7-11 and buy a pack of gum with it? That sure hasn’t happened, so it is just no more than as you describe – something of value because seom people say that it is… So how does that differ from those NFT pieces of virtual property the Biebs and Jimmy Fallon among other bot at the Bored Ape Yacht Club…. That worked out well, didn’t it – https://beincrypto.com/2022-paris-hilton-jimmy-fallon-nft-cringe-bayc/. Hey I’m just trying to prove I know about as much about bitcoin as Private does…

Cryptocurrencies “only have value because a group of people believe they are valuable” — which is equally true of every currency.

I don’t dabble in the stuff but it seems to me the difference is that the governments debasing the fiat currencies can declare alternate currencies illegal anytime they like to close the escape hatch. That mitigates against widespread adoption as the risk becomes too great.

‘ they only have value because a group of people believe they are valuable. There is absolutely nothing backing them”

That’s not exactly true, although this is a subtle point. Bitcoin’s value is in its scarcity, a protocol that doesn’t allow more than a modest finite number to exist. While dollars are back by full faith and credit (and nukes and IRS agents with guns…), the number of dollars is a rapidly moving target ever since the central bankers were put in charge and we’ve been inflating ever since to the detriment of savers everywhere.

“To me, timing the key to playing cryptos, just as it is in playing in a ponzi scheme: figure out the real game being played, get in early, ride it up hard, then get the hell out before everyone else figures it out.“

Yes, but stocks and the whole market are very much like this, driven by sentiment a lot more than fundamentals most of the time. It’s only a weighing machine in the long term, and may well be a voting machine for longer than your time horizon.

Combining these two points, Bitcoin is some weird hybrid of digital gold (scarcities, defensive) and a hyped up meme stock (volatile, sentiment driven).

I don’t own any, but I wouldn’t write off crypto quite so quickly.

xerty, Well said about the market. That is an observation that most people don’t get, the part about sentiment compared to fundamentals. Combining the two is an art or a craft. Two sides to investing. Timing and holding for the long term. I think a lot of people here combine the two.

My favorite beanie baby story:

We’re standing in line at a Rite Aid during the back-slope of the beanie mania. There was a pile of beanie babies near the checkout line. They were marked with a “sale” notice. Remember we are in a retail business. Seeing the beanie babies, one customer walked to them, picked one up and said to their shopping pal, “Wow! Look at this! This is an amazing deal! Do you know what this is worth!?” hahahaha.

Probably about as much as a tulip bulb.

Wondering if in future we have a financial disaster… I am hoping that I could by some diet coke for a couple of beanie babies.

Pete, I be glad to answer any specific questions you have about Bitcoin. Bitcoin is a form of digital currency that aims to eliminate the need for central authorities such as banks or governments. Instead, Bitcoin uses blockchain technology to support peer-to-peer transactions between users on a decentralized network. NO ONE and NO GOVERNMENT CONTROLS BITCOIN (it is decentralized) and that’s what appeals to me and many many other investment professionals and investors. Anything that Jamie Dimon claims to hate, must be good for all of us; as JP Morgan Chase is unable to manipulate that asset. BTW, just do a search for JP Morgan silver manipulation (they control the SLV , the largest silver ETF) through millions of ounces of naked shorts on the commodity exchanges (too much to write).

One of my institutional clients (from Vietnam) asked me many years ago to look into Bitcoin (and other cryptos for his corporation and personally). After my research, I personally have been buying Bitcoin since about May, 2017 when the price was around $2000. The entire country of El Salvador 🇸🇻 uses Bitcoin (there will be many others) as legal tender. I have no intent to sell any Bitcoin (just like most of my precious metals) and hold 95% of my Bitcoins in a cold wallet.

Lastly, as of Dec. 18, 2023, 19.57 million Bitcoins have been mined, leaving about 1.45 million bitcoins to release. The total lifetime Bitcoin supply is capped at 21 million. Unlike the US Dollar and all other currencies that “unlimited” can be issued http://www.usdebtclock.org

Again, I’d be glad to answer any questions anyone here may have. I am skiing in Telluride, Colorado (no new snow today) and may not be as timely with my answers.

The ground beneath you is shifting, and either you get sucked in by holding on to old ways, or you take a giant step forward by taking some risks and seeing what happens.

Thanks to all who replied and made excellent comments for and against Bitcoin. This simple discussion reinforces what little I know of Bitcoin (scarcity, uncontrollability by governments,

people searching for alternatives to world fiat money systems, value simply because people say it has value) I hold some physical gold since it has been a wealth holding vessel for thousands of years. Why is it valuable? Limited supply and because people view it as valuable, but the government has in the past and probably can in the future if needed take it away from individuals (ha, they gotta find it first) I don’t look at Bitcoin as an investment but rather another way to diversify and possibly insure the wealth of my estate.

I do believe that the dollar is still the cleanest dirty shirt in the dirty clothes bin, but the world seems to be becoming more and more discontent with our abuse of it as the world’s reserve currency through literal weaponization and our continued exportation of US inflation due to our ridiculous out of control government spending.

Nice, I owned one time, 10 bitcoins at avg price around $1250/per and almost 100 Ethereum at under $50 each. Alas I sold at $9000 and $200 avg, respectively. I made a ton but what might have been – woulda, shoulda, coulda. I have a friend that mined his own way back when and has upwards of 130 BTC that he got for FREE, but he did buy more when it was under $1000 – his avg is in the $20 range! So investment was time plus maybe $4000 total and he owns almost $6,000,000 worth at today’s prices – he sells very little.

I worry about the seedy side of the digital currency community – no gov’t control can be a double edged sword in that regard – the seedy side can manipulate and use it for nefarious means. I have been out since 2018 and reluctant to re-enter. Plus, for the avg Joe, it can be complex to buy and store – In don’t trust the on-line repositories as they are like banks in the wild west. You need your own physical digital wallet (I have a trezor) and that is a bit scary holding hundreds of thousands of BTC at home or where ever! And the volatility – It’s still a very embryonic and crazy community

I have owned 10s of thousands of BTC as I mined during the early days of using a CPU as well as video cards. I also mined LTC. I treated it all like a business as I had access to a datacenter, free electricity, and everything an ISP had to offer. I ran a semi popular LTC mining pool website. I sold as I mined. I got fully out of mining around the time ASICS came out because I got tired of the game. I sold everything when BTC spiked to approx ~10K. I have no regrets and no longer care. It was a profitable business model right up until it was not due to Chinese ASIC vendors being shady as “heck”. I would not even know the price of BTC if financial websites did not plaster it on the main page like it was the DOW.

The one thing I missed out on was creating a gambling website when you could still get away with it in the early days. I am also thankful I stopped using any exchange that had to start reporting to the IRS. Got out before that as well.

In the end I would not buy any crypto. It is useless for the original intention it was created for. It has warped into something it was not meant to be. Like a store of wealth instead of a circulating currency. So they twist a total failure into something else which is a bad sign. Also the people still getting ripped off on coinbase via hacking makes me chuckle. Coinbase does not care. Crypto has attracted the worst of society to it’s ecosystem. From almost day one and continues to this day. Should I be included in that statement? Maybe? I just saw the opportunity. Cost of goods needed to mine and what I could sell it for. Mining pools taking a cut of every block found. As time went on though you quickly realized the people in the industry were off somehow. Scams everywhere.

great info and story – thanks for sharing!

Oh the stories continue. On bitcointalk.org a random user needed help with his bitcoin wallet. It was borked. He was in a panic almost. So I just offered the basic advice of a -rescan of the blockchain at the command line for the wallet. He gave me 100 BTC as a thank you for being the first to offer the correct advice. Was worth approx 1000 dollars back then.

The person ended up being:

“Ross William Ulbricht is an American serving life imprisonment for creating and operating the darknet market website Silk Road from 2011 until his arrest in 2013. The site operated as a hidden service on the Tor network and facilitated the sale of narcotics and other illegal products and services”

It was a pretty goofy time as crazy thing after crazy thing kept taking place. I was pretty careful so I was just watching the “damage joy” happening on a weekly basis.

And yes.. bitcoin can be hacked and was. They roll back the blockchain to fix it. Other bugs have been discovered which could have had the same result.

Thanks for the article, AB

RMB will continue to drop as a global currency as China continues to struggle. You may have seen that the Chinese central gov. authorized new bonds starting last half of 2023 to help local governments with their debt burdens.

Deloitte published reports recently showing that local gov. debt (~35Trillion RMB) exceeds central gov. debt (~26T RMB), so we can look at that as a published baseline.

Based on conversations with some of our friends in China in the last months, local gov. off-book “hidden debt” appears to be dramatically higher (at least an additional 10-15T RMB). It will likely take China several more years to (a) come clean and (b) get it moving toward resolution.

Until then, Government Participation as a contributor to China’s growth numbers will continue to be badly overstated (and will be negative rather than positive).

Coupled with China’s slowing growth, the real estate bubble, aging population, failing ‘road and belt’ strategy, their debt woes (incl. this hidden local gov. debt) will make other countries’ desire to hold the Chinese Yuan continue to drop (IMHO).

Private I appreciate your posts regarding China (as well as other topics) I have read that businesses from the West are decoupling from China at a pretty brisk pace. Is this true? And what could the ramifications be to the dollar if decoupling happens too quickly?

Yes, Pete, China is seeing negative foreign investment. Lots of companies reducing their exposure / pulling out. The Chinese economy isn’t recovering from the pandemic-triggered mess, and companies are trying to diversify away from being so reliant on China.

In our China practice, we are seeing far more interest from non-Chinese companies looking to reduce their reliance on China and of Chinese companies trying to go abroad than we are seeing foreign companies trying to move into China.

Unemployment in China (esp. among the under-30 “youth”) is huge (incl. massive underemployment where college graduates are delivering fast food, etc). The real estate bubble is straining the economy. government debt is hurting the economy too, both because it is huge, but also because so much is hidden “off books”. The fact that the Chinese population is actually shrinking (and has been for some time) underlies a lot of the problems – everyone was told by the government to plan on population growth (esp. in real estate) when it was actually shrinking. A lot of the fundamental problems are driven by the central Gov. not being truthful in their economic data reporting over many years.

We have a running joke that the worst job in China has to be the poor bastard who is responsible for tracking of all the made-up data in gov. reports so that it all appears to be consistent. We see data reported in Chinese regional press that is rapidly withdrawn and re-released to match data in the narrative being reported by Beijing.

I don’t think the dollar will be at much risk from the mess in China. For better or worse, the Yuan is tied to the dollar, despite protests by the Chinese gov. that it isn’t (although the gov. can make it move a bit, it is too tied to the dollar to move very much or very long IMHO), so as their economy weakens, I think the dollar will strengthen against the Yuan.

To put China’s economic woes in perspective, I think you have to take a step back and look at where all that foreign investment/economic activity is going. Global business isn’t evaporating, it is just moving away from China. Other countries are seeing growth that will offset reductions in China.

This creates a huge challenge for Mr Xi because he no longer has the huge economic growth engine to drive his global ambitions while looming domestic economic crises will continue to dog him. I think this is a big part of why China is “flexing its muscles” internationally – to create “Foreign enemy” distractions to divert the domestic population’s attention.

Apologies if this all seems disjointed. this is just my mushy thoughts as I wait for a call from a client after too many hours working problems on far too little sleep.

Ha that’s pretty good stuff for mushy thoughts! Thanks so much for your time and in depth response!

Private, one thing China can do with the problem is build up the military. Age old solution to the problem of unemployment and economic growth. When I start to hear that more and more young people are being pushed into military service like North Korea, Russia, Iran and I suspect Venezuela then I will be worried.

The Chinese military has been shrinking its troop count pretty significantly in recent years so it can focus on having more highly trained, better equipped soldiers rather than just big numbers of people in uniform. They hope it will help get better results from their defense spending.

You are probably right, however, that if they start inducting lots of “cannon fodder” we should all watch out.

It is interesting that China has been pushing military units into the general economy for years to make them help pay for themselves. For example, for many years, we have seen major construction projects being bid by companies with strange names like “643 construction company.” Turns out, it is actually the 643rd engineering battalion of the people’s liberation army. Caused a little panic among foreign investors to learn that their IP sensitive construction projects were being built by the Chinese army…

Bitcoin is for the streets. Reminds me of playing Three-card monte. At the start of 2023 no brainer arbitrage of the grayscale bitcoin trust was available. Due to the locked in fund nature, it was trading at -40 to -50% to NAV. Logically if the discount narrows by 50%. I would receive my best lifetime return outside of options/derivatives markets.

Have been disturbed by golds obvious double top. Makes me believe a short term top is being put in place. Fearing a lost decade 1980s to 2001 period could happen. Leaving 20 years of lost investment returns on the table would be foolish.

Oil trade really happened in 2022. 2023 went long TLT and TLT $100 Calls.

The TLT trade should pay for my 3rd divorce easily.

Still not a normal week. This will be just a 4 day week with some people still being off due to vacation and the weather. Next week we will be back to normal.

Normal?

https://youtu.be/C9Pw0xX4DXI?si=JJfy6R1YUlVBqpdE