For years I have watched as the specialty finance company’s (CLO owners) have sold millions of shares of common stock in ‘follow on’ ‘at the market’ offerings.

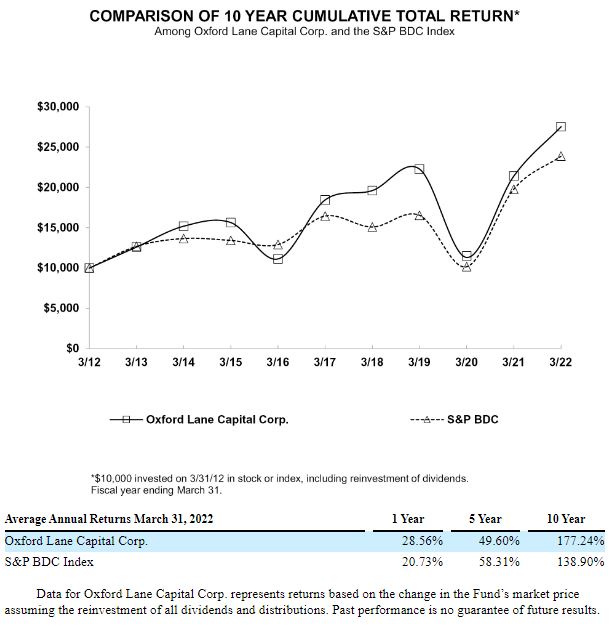

These company’s (Oxford Lane Capital (OXLC), Eagle Point Credit (ECC) etc) pay huge dividends to there shareholders and generally the net asset values per share fall–over time. Some folks like to refer to these as ‘ponzi schemes’, although they are obviously legal and the financials are transparent–and the total returns have been good for Oxford Lane–

The reason I watch these offerings is because I hold substantial positions in the ‘term preferreds’ and as a holder of ‘senior securities’ I like to see them sell all the common shares possible because each dollar that comes in helps to protect my personal position since they must maintain a 200% coverage of the ‘senior securities’.

In the case of Oxford Lane Capital (OXLC) on 8/31/2021 they had 115 million shares outstanding–on 7/31/2022 they had 151.6 million shares outstanding. The net asset value (NAV) fell from $6.69/share to a current estimate of $5.36/share–BUT total net assets rose from the $820 million area to $947 million. The NAV per common share is not nearly as important as the growth in total net assets which is what protects the ‘senior security’ holders.

Thank God the SEC requires 200% asset coverage! Any time there is a concern the CEF just issues new shares at the “offering” to it’s shareholders and bingo all is well! Seems to good to be true but apparently it is.

Hi!

I don’t understand how the issuance of more common stock is to the advantage of the preferred owners. I would have thought the opposite: The higher the value of common which is out – relative to a given value of preferred – the farther it can fall and the worse things can get before the company has to do something to protect the preferred holders.

Could someone please explain?

Thanks.

David–the preferred shareholders have a claim on 100% of the equity (after debt is paid which is minimal) before the common shareholders get 1 red cent in a liqudation. This isn’t about share price of the common, but is about total net asset value. The company will do a reverse split on the common shares when it gets too low (under 5?).

Tim, thanks for the information. I hold some OXCLM shares, so this is good news. I plan to hold them until the maturity date in 2024. I bought them last summer at 23.50, so a little bit of a capital gain. Another nice feature is this issue pays monthly.

Bill – I hold a couple of the term preferrds as well and plan to hold to maturity. I like the oxlcm issue because of the 2024 redemption–keeps the share price steady.

OXLCM is past its call date as well which should help keep it stable until redemption in 2024.

Tim, With these types of preferred, is the strategy to buy-hold til callable date, collect the dividends and move to the next one, or are you taking profits and pruning positions as price goes up above purchase and buying back when it dips? Great site.

Goldpilot–for me I own the nearest maturities and plan to hold till redemption. OXLCM is a 6.75% term preferred with mandatory redemption in 2024 and the short maturity date holds the share price steady. The further one goes out (for instance the 2029 issues) the more volatility one adds.