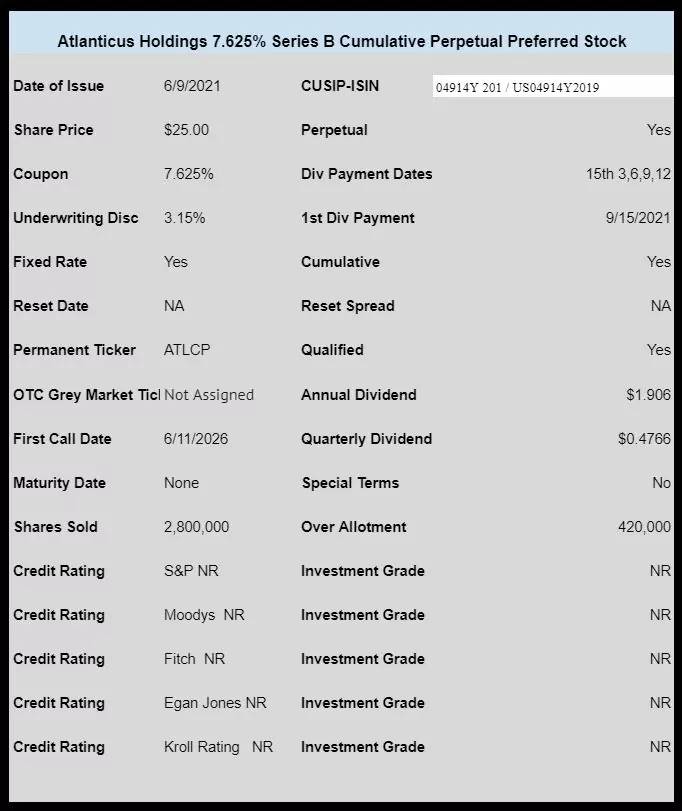

Specialty consumer lender Atlanticus Holdings (ATLC) is selling a new issue of high yield preferred stock.

ATLC is a lender to higher credit risk consumers–make sure to do plenty of due diligence before moving forward with any investment.

The new issue has been priced at 7.625% and is cumulative and qualified–the issue is unrated. NOTE that the actual ‘trade’ on this new issue doesn’t take place until tomorrow so NO OTC grey market symbol has been assigned yet. I will post the ticker when known.

The preliminary prospectus can be read here.

The pricing term sheet is here.

EarlyBird was on top of this one.

not yet on schwab

thx

Just checked Fidelity again, not on there yet.

Insiders own the majority of interest and control this company. The Series B preferred is below the Series A in the stack. The Series A was a private placement sold to insiders. Don’t know how good or bad all this is, but makes me a little uneasy. Opinions?

In my opinion, several red flags. Not for me.

Usually better than external management unless they abuse it.

C. That balance sheet is kinda nasty. Though cash flow is great now. It will probably run to $26 also, but Im gonna pass. I have hit my limit on these types.

FWIW, Here is some color on those issues from SA. The writer of article of this comment wrote this. He is a bull on the company’s common.

We read that the $40 million Series A is convertible at a rate equivalent to $10 / common share so we think it’s safe to assume these convert (perhaps shortly in connection with the share repurchase). We understand that these were issued to affiliates of the insiders to refinance certain loans that were maturing. We note that we include the 4 million shares in our diluted share count as does Atlanticus. We observe that the $99.4 million of Series B you see on the 3/31/2021 balance sheet results from $100.5 million of preferred issued to an institutional investor that, from reviewing the exhibits to the company’s public filings, we believe to be Towerbrook (large hedge fund). We read that these were issued by a wholly-owned subsidiary (thus the “issued to noncontrolling interests” designation) of Atlanticus to help finance investments in loans and, presumably, provide additional equity / junior capital in securitizations and other financings. We note that these preferreds carry a dividend rate of 16%, of which 6% is payable in kind (we don’t believe the company has every used the PIK feature – which we like). We note that we (and the company) calculate EPS and we calculate Level Free Cash Flow per share after these dividends (which appear to be deductible for tax as treated as debt for tax purposes). It also appears to us that these preferreds have put / call features that limit the life of these securities so, given that and the above, we view these more like junior debt (likely structured as equity for GAAP purposes to facilitate the company’s secured borrowings and securitizations) when the company did not have the same access to capital (or earnings / retained earnings) that it does now (and this much higher rate made sense, although issued by a subsidiary, which we would expect to command a higher rate in any case). We anticipate that, now that the company’s position has changed, these will be redeemed (and provide some additional earnings and cash flow upside). Hope this helps answer your questions.