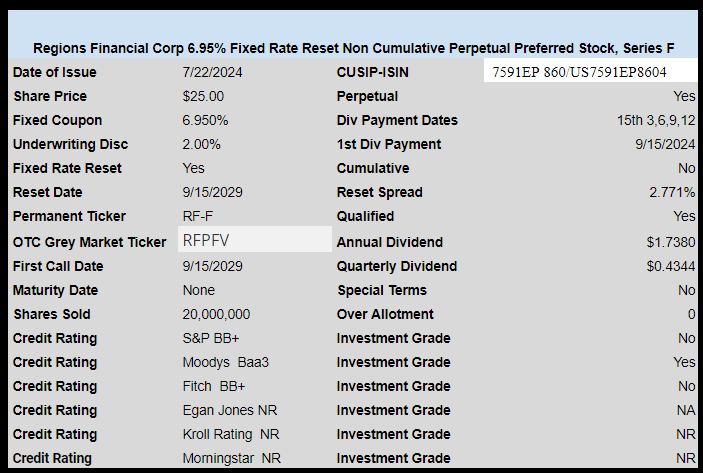

Regions Financial (RF) has priced their new fixed rate reset preferred with an initial coupon (for about 5 years) of 6.95%. After 9/15/2029 the coupon will reset at the 5 year treasury plus a spread of 2.771% and will reset every 5 year thereafter.

As noted earlier the proceeds will be used to redeem their RF-B 6.375% issue which was slated to being floating on 9/15/2024—likely at a coupon above 8%.

The new issue is split investment grade with Moodys giving the lower investment grade rating of Baa3, while S&P and Fitch are a notch lower.

The pricing term sheet for the new issue can be found here.

RF trading around par. I saw the MS 6 5/8 was at 25.80

7/29 @9:40. Vanguard will not allow trades.

I confirmed that schwab will allow trades. I purchased initially when on the pink market

IBKR has it as RFPFL now

I have a lot of exposure to RF B and moving from a 6 3/8 to a 6.95 isn’t so bad! I expect will be able to get under 25 in near future with current pressures.

BUT the handwriting is all the wall. The new issues coming to market seem to indicate some desks just making their moves now rather than hoping long term yields will drop along with short rates….I see 1 yr CDs are falling thru the floor……

Was able to purchase today at Schwab( to my surprise)

Yesterday at 7AM I couldn’t place an order at Etrade. At 9:15AM I was able to place an order and the system accepted it. At 9:45AM my order hadn’t executed (even though based on the price, it should have), so I called the Etrade trading desk. They told me that because it was a new issue, my order was kind of hung (my words). They did something to get it to execute. They told me that if this ever happens again, I should call them. For new issues, at Etrade, I’ve had orders not accepted and orders accepted and executed. This is the first time I’ve had an order accepted but then hung up in their system somehow.

first time in awhile that schwab accepted an order for a grey market issue. it executed without my calling

It’s actually showing as pink – current information now:

https://www.otcmarkets.com/stock/RFPFV/overview

i guess that is why they accepted it. I expected a change in symbol when it went pink.

Schwab is handling this differently. It did not settle last night. I still have the cash in my account. RFPFV is in my account for the right number of shares at $0. it shows up in History for the right price and shares but again a history transaction of $0. The description on the preferred is REGIONS FINL 6.95% PFDWIWHEN ISSUED. It looks like they have reserved the shares.

Not buying it. Normally i might grab a few shares to stay in the game but now there are so many other things that pique my interest.

While no one knows where rates are going to be in 5 years and having said that Iam not liking that “reset rate”. Probably will take a pass on it.

Chuck I agree with you on your reasoning. The reset of 5yr plus 2.77% doesn’t seem like enough for the unknown of 5yrs from now. I personally would prefer a hold and not worry stock and I think you might too. Look at all the bank preferred on Tim’s fixed to floating list. 2yrs ago, the TBTF banks had preferred that paid 3% to 4% minimum before they floated and people were happy in a zero interest rate environment. Then rates went up and their prices went down because 3% didn’t seem so great anymore. Now that they have floated the yield is still not that great at 6.50% and they still haven’t recovered to par. If rates go down it’s possible these old preferred are going to show a capital loss.

Now look at this new one and extrapolate. At first, if rates go down this will increase in value the first couple of years then as we get closer to the reset date it may be more volatile. If the opposite happens and rates go back up next year or in a couple years then this one is going to be like those old floaters and lose value. Win win for the bank.

The odds are this is not a long term hold, but a flip trade over the next year. I play the game but I tire of it the older I get and would prefer to just buy and hold as much as possible. Why I like market panics when I can buy and get a cushion to just hold and collect the dividend..

Charles M; I think you and I have quite a bit in common. I was actually somewhat excited about this issue until I say that “reset rate” and it just got me to thinking its fine for a “trade” but I don’t want to hold it till it resets as there’s a pretty decent chance it might sink. Do you or anyone happen to remember what the “reset rate” is on MTB+J??? I’m trying to look it up but can’t find it for some crazy reason. Always good to hear from you.

Chuck—there is no reset rate on mtb-j

Chuck, MTB -H is a floater but doesn’t float until almost 2-1/2 yrs from now. It will be 3 month CME term SOFR Plus .26161 adjustment and 4.02% so if it reset today it would be about 9.56% but who knows in a couple years. Right now it’s paying 5.65% not enough over a CD to make it worth it. As a matter of fact compared to the MTB J the H should be a lot lower in cost to bring it in line with the yield of the J

Hello Whidbey Islander; A big Thank You goes out to you. Maybe thats why I was having so much trouble finding it—LOL.

If you don’t like 7% or if you don’t like the credit I would stay away from this as well. However, your interest rate scenarios are not a good reason to buy, plus I don’t think they are completely accurate. Also, the bank does not benefit at all from how the issue trades in the secondary market. I bot some.

While I hate resets they are in vogue and better than fixed for life IMO…….PS NEW DEAL COMING……………………

IP , I don’t mind if they have a cushion of say T-bill plus 4% but this one with just 2.771% doesn’t seem that great long term.

Floaters are far more desirable to me. The one chance in five years to reset means much less certainty then a continuous adjustment.

We’ve seen those with VA five year high water marks….

Floaters are good for rising rates, or now in the aftermath of a rising rate environment there are some good ones. If you believe there will be multiple rate cuts it may be time to switch to fixed rate issues. Personally I have no clue so I do some of each. Pinned to par floaters are some of the best current deals for straight income no capital gain.

With perpetual securities I’d far rather have an interest ‘escape’ structure then a fixed rate. Especially w a short call

What’s interesting to me about pinned to par floaters is that they give you such a current yield advantage over yields on fixed rate that if cap gains is not your focus, even a downturn in interest rates will not hurt your principal as your income comes down. So you will most likely maintain your advantage over the fixed rate alternative…. And if your fixed rate alternative is close to par anyway when interest rates come down, it too is going to become pinned to par thus limiting your cap gain potential as well. So like you say, “best current deals for straight income no capital gain.”

2WR & Martin, do you have a good example of a “pinned to par” floater?

Easiest ones for me to think of are the two CUBI’s E and F and also ALL-B.

Martin:

“If you believe there will be multiple rate cuts it may be time to switch to fixed rate issues. ”

That is the big issue now. Bloomberg did a piece last week that the Fed will likely hold this month, but could surprise with a 50 basis point cut in September. Bill Dudley (former President of NY Fed) put out a Bloomberg piece today that he changed his mind and feels the Fed needs to cut rates now and not even wait until September.

This is Dudley’s big argument:

“Most troubling, the three-month average unemployment rate is up 0.43 percentage point from its low point in the prior 12 months — very close to the 0.5 threshold that, as identified by the Sahm Rule, has invariably signaled a US recession.”

Personally, I have sold nearly all my live quarterly floaters….only have SLMBP and C-N now due to their truly monster yields near 10%. Finding value in some of the quality property REIT perpetuals that Bea has mentioned like BFS-D and CSR-C.

GLTA.

Tim,

Expected S&P rating = BB+ (not BB).

Expected Security Ratings (Moody’s/S&P/Fitch):*

Baa3 / BB+ / BB+ (Negative/Stable/Stable)

mbg

Thanks mbg–will correct.

speaking of regional banks

https://www.youtube.com/watch?v=zRllxp96S5Q

While the video is long, it is very informative. Thanks for sharing.

Thats an outstanding YouTube piece!!!!

I see any early OTC quote at 25.04.

It looks to me like they priced it right at 6.95%

I would buy it here if I could get it at 25.04, but grandpa Vanguard will not let his grandkids buy preferred stocks OTC, even investment grade issues. “Too dangerous! Why, back in my day, a kid could lose a finger playing with those!”

I am going to guess you know this but we can buy OTC just fine. It is when they start on the “grey market” which is the problem. I have to wait until it becomes “pink” to buy. Never stops me from trying though. Ally will put in the order for me but it often sits doing nothing.