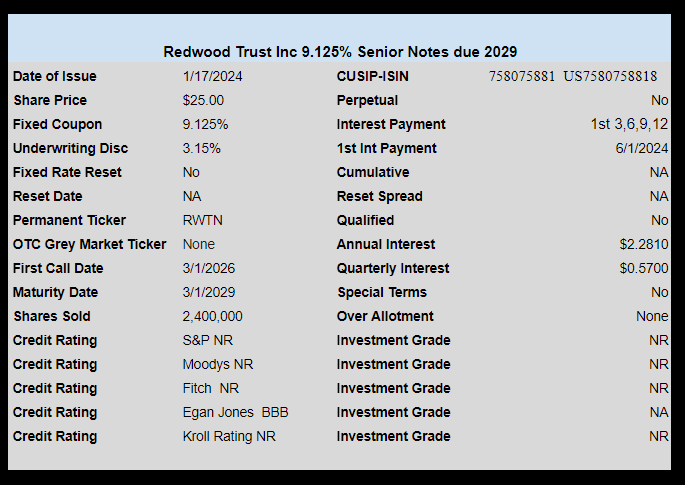

mREIT Redwood Trust (RWT) has priced the previously announced senior notes.

The notes price at 9.125%–right at the ‘yield talk’ number from Earlybird yesterday.

The issue will trade under ticker RWTN when it begins to trade on the NYSE. It is likely to be at least a week before trading begins. There will be no grey market trading, but if one calls their broker bond desk they may be able to buy shares prior to exchange trading–but there is little reason to buy early as there are low odds the share price will run up quickly.

The pricing term sheet is here.

Am i missing the preferreds from Redwood on the preferreds sheets? RWT-A? Can’t find them.

Hi Jimmy–I see it is missing on some of the sheets–will get it today. Thanks for noting that.

https://innovativeincomeinvestor.com/security/redwood-trust-inc-10-00-series-a-fixed-rate-reset-cumulative-redeemable-preferred-stock/

I have some 7.125% coupon Credit Suisse notes that got called this morning (I’ll miss those), and a RILY position that hit is profit objective.

It is great that ECCF, CCIA and MFAN, RWTN have all come to market at nearly the same time and 3 of the 4 will have preferred & baby bonds outstanding as comparison points. Need to see how all 4 of these trade as I will base decision on YTM or CY as the case may be. There are a couple of BDCs baby bonds that I will also consider in the mix.

I have to say I am not totally convinced an unsecured bond in a non agency focused mREIT really offers much protection given the $billions that both MFA and RWT have in secured debt. It is an advantage that the notes return par, however.

I would imagine that the CY on this mREIT notes should be pretty close to that of the associated fixed (or reset) coupon preferred.

August- I don’t disagree on your “extra protection” thesis. With that said, if the yield loss (from choosing the BB vs pref) is less than 1%, I will go BB all day. This includes the math when adjusting for YTC.

These widgets are different than other levered vehicles. Running a MREIT is like driving a car as a student driver. You have the added safety of the teacher hitting the brakes if you fail to do so when in danger. The repo/leverage providers will pump the brakes if you don’t, long before you are wiped out.

And the main distinction is that these MREITS generally hold liquid assets that can be sold.

Compare this to a levered business like Nustar. NSS really doesn’t have much more protection then the NS prefs. The company is highly levered and will likely NOT be able to quickly sell assets to reduce leverage in times of stress.

BTW, I am (currently) interested in MFAN and PMTU, but not the new RWT. The RWT portfolio is more levered and less liquid.

Thanks Maine,

Food for thought on the 100 bps yield pickup for preferred vs baby bonds on mREITS. It will be interesting to see if they trade that way.

The thing with RWT is that you have to buy off on the idea that banks are exiting the Jumbo market and that RWT will pickup meaningful share from that. You also have a preference jumbos and BPLs and tolerate pet projects like blockchain etc.

Both MFA and RWT have meaningful BPL allocations, but MFA has more non qualifying loans. One can always debate about which is more liquid, but when it hits the fan (when you really are looking for protection of bonds vs preferred) my sense is that neither one of these portfolios would prove to be very liquid.

Thanks for your feedback!

It seems ages ago, but this discussion made me re-kindle the Covid crash. This article serves as a good reminder/ scare!

https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/margin-calls-shine-spotlight-on-mortgage-reit-liquidity-57756984

Maine, Good point. Reminds me that I read this last night on Quntum and the trouble some of the BDC’s had at the time too.

https://www.quantumonline.com/search.cfm?tickersymbol=PFX&sopt=symbol

I’m shocked this isn’t a AAA rating from Egan Jones. A hard NO from me 🫤 Swim at your own risk

Ab The state of California mandated that towns and cities had to build new housing and change building codes to allow for high density. I think mandating this is going to cause other problems. A lot of these multi family projects are just about finishing construction and a lot all at the same time. The construction loans have to be rolled over now into longer term loans.

https://www.northbaybusinessjournal.com/article/news/marin-county-governments-face-rezoning-deadline-for-california-housing-edic/

Charles,

Realizing that a large part of RWT’s book is business purpose bridge loans, does this article have a direct impact on RWT (IE are they involved in any of this financing?) or is this article more for general interest.

Both August, the current copy of the latest issue talks about recycling office and shopping to housing. Also if you’re planning a trip to wine country there is a lot of articles on that.

Lol

Thanks Charles. My wine country trips are pretty simple. We pretty much go to Inglenook, the Stags Leap area and Prager Portworks. The latter is my personal favorite.

Two different subjects. CA law is zoning change. Potential future building. These will only get built if they pencil out. Other subject: Recently constructed multi-family units where construction loans will need to be refinanced. Jury is still out on this one. I think it will be a nonevent. Bad projects will go to foreclosure. Good projects will get restructured with more equity from borrowers.

Just to add color to Charles’s post – we walked some of those new “forced multi-family housing” projects in the south bay (across the bay from Charles, but with the same crazy housing mandate). Most are very poor quality. they appear to be being built just to hit the mandates, not as long term, financially viable projects.

Not surprisingly, from the discussion at our visit, they are not finding a lot of paying tenants, but the county is starting to put a lot of “housing voucher” clients in.

Putting on my Karnak the great hat, I foresee the counties taking over more and more of these projects when they fail financially. The counties here have no skill managing housing, but they are getting into it anyway. If that happens, the counties will end up bailing out the current operators/lenders (if those folks have greased the right palms). Time will tell.

Private I don’t know where the money is going to come from. Latest on the news is San Francisco still looking at almost a 30% vacancy rate. The city is projected to have a 1 billion budget deficit by 2028 if they don’t cut. Property taxes are down due to commercial RE. The recent shopping mall the owner turned in the keys is on the market for 750 million less than when it was bought in 2016. They are spending 2 to 1 more on programs, projects, salaries, retirement then they are taking in.

What’s happening in CA is that localities are required to legalize multifamily housing. They are not required to build any housing. That will be up to builders to decide whether they want to make that investment.

That said, with all pent-up demand for housing in CA, if you legalize more housing, builders will certainly build it.

The problem will be if too much supply hits the market at once which will increase lease-up timelines. Then, if credit markets freeze at the same time when these bridge loans need to be refinanced into permanent loans, it will be a problem for lenders like RWT.

Frankly, I’d be more concerned in low barrier to entry markets like Texas. It’s much easier to build housing in TX than CA and as a result, that’s where a lot more of the new supply is going to hit. However, TX also has more population and economic growth, so even if there is a temporary issue, it’s easier for demand to grow into any excess supply.

the converts look cheaper