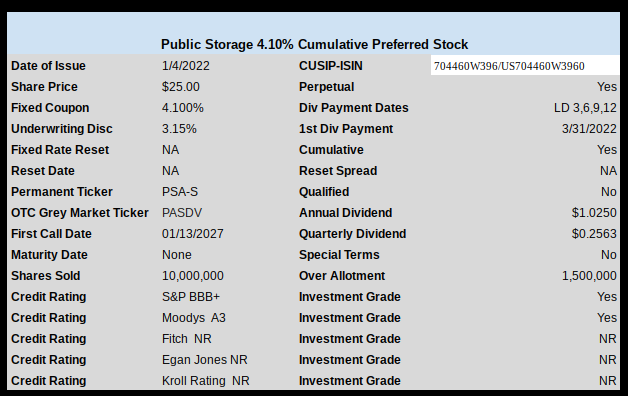

Self storage giant Public Storage (PSA) has priced their new preferred stock offering.

The issue prices at 4.10% and is cumulative and non qualified.

This coupon is about as expected as their previous new issues were at 3.95% (PSA-Q) and 4.00% (PSA-R).

The issue trades immediately under OTC temporary ticker (PASDV).

The pricing term sheet can be found here.

Hi Tim,

Just picked up a 200-share starter position at $24.84.

Folks can complain about the 4.13%, but it out-competes BAC @ BBB-, and the GS & MS @ BB+. It beats current returns on IG senior debt, and helps to anchor down the riskier preferreds we’ve ALL been picking up over the past 6 mos. I happily take walks and singles, to balance out my home runs and triples in this income space.

The grey market symbol I bought at is PASDL.

Corrected CUSIP is minus the first 0: 74460W396.

Thanks much Tim, appreciate the work.

The banks have qualified divs. Might matter to some people. Reits are taxed as regular income.

Thanks for all the input, there are definitely a few angles I hadn’t thought through carefully enough.

As an income investor with a perspective that interest rates, in spite of the hype will never go up meaningfully and if they do get to half of what the historical neutral rate was….they will quickly be brought back down to zero or close to it.

When I look at the total failure of negative rates in Europe and Japan and the inability of their Central Banks to reverse course and the talk but little action at the BOE, BOC, RBA and the New Zealand Central Bank it indicates to me that we are permanently in a low rate almost zero environment for as far as the eye can see.

And so….in almost every asset category I invest in, I take a laddered approach allowing me to take advantage of rising rates in the future if I’m wrong and meet my immediate cash flow needs in the present.

I guess you can say…..not an ideal strategy…but what is an ideal strategy in these strange…..almost irrational times?

Two years out of the past 20 I made less than 4%. This one goes straight to the trash bin for me.

I seem to be in the minority but 4.1% and a par value of $25 so nothing to lose still sounds pretty darn good in a universe of rate suppression where everything has been terrible for 13 years.

Ten year secondary market CDs callable in 6 months 1.8%-1.9%

Average good quality big cap equity dividends 2%-3% or less

GSEs for 12-14 years (also callable) 2.5% or less

Investment grade Corporate Bonds at par any duration around 2.5% or less

And many things super expensive value traps.

So how is 4.1% not appealing except in our memories?

Richards–depends what your goal and mentality is for your circumstances. With 4.1% you are likely to lose capital when/if rates go higher since the issue is perpetual. On the other hand if all you are looking for is a solid 4.1% for immediate income it fits the bill. Everyone has different needs.

…add one more feature to the decision making process…

How much capital do you have? 4% on a portfolio of a large number may be good enough, esp if inheritors are ignored!

Perhaps a residual charity would be a happy beneficiary of the shares after their work is done for you.

I just saw that fc stated the same thing next post. There are inheritors who can and have ridden out generational debacles.

Maybe PSA and the brokers ain’t looking to retail small investors, but insurance and trusts.

Joel, throw in the insatiable preferred funds that always need to buy, also. If certain insurers etc. needed it, it could just be a private placement. The vast majoirty of preferreds are non traded private issues already that we never see or hear about…. So my nickel bet is the reason a tradeable ticker is slapped on it on an IPO is they need a few more fish to hook with the bait.

What Tim said plus.. unless you have a metric ton of cash to put into play you can do better then 4.1% today and it will probably be a qualified dividend instead of regular income. Some of the illiquids we discuss easily fit that bill. We would love to buy the ills > 5% but the going rate is 4.2-4.5% if you want to pay a going price close or below the call value. Now it might be Baa2 instead of A3 in some cases but I would not worry too much about an electric ute not paying.

Richard – Here’s something to think about – there’s a potential flaw in your premise which may or may not be important to you…You say, “4.1% and a par value of $25 so nothing to lose.” Well, it’s pretty close to true with a credit like PSA that you do have nothing to lose as far as that $25 par value is concerned in the realm of loss of principal from the company going bad, but what about what you have to lose in market value if interest rates change to the upside not even that dramatically? With a perpetual, you have no guarantee that the market will ever allow you to recoup your $25 should interest rates go up permanently… If interest rates in general cause PSA to have to offer their next preferred issue at 5% instead of 4.10%, your 4.10% perpetual should be worth approximately $20.50 in order to be competitive with the new issue.

That possibility is what the market is worried about now in general… If rates go up permanently, then sure, you’ll continue to receive your $1.025 every year with nothing to worry about (aka “lose”) but you will also have permanently lost your ability to reclaim your $25. If that is not important to you, as it isn’t for those who just want to know their income stream is safe and reliable, or if you are not a believer that the risk of higher interest rates is more real now than it has been recently, then you’re right, “nothing to lose.” Otherwise………….

Lets slap a bit more meat on your big bone of info and use your example…Lets stick with PSA… PSA-G which was issued at very end of July 2017 (and is still presently outstanding) at a 5.05% coupon. The 10 year was 2.21% then, so that isnt an impossible stretch to return to. And as 2WR stated it must drop to lower $20s to accommodate. Everything is based on ones assumptions, and nobody has a crystal ball. The biggest worry is one thinking he doesnt care about what the portfolio value says, just wanting the income, until it happens and then its too late for a mulligan.

That being said, I have to hit some low yielders myself just for portfolio set up. I dont like it, but I do. In fact I bought a small amount of a 3.4% YTM IG ute bond that doesnt mature until closer to end of decade, ugh. But it does mature well before I hit Medicare, ha.

What do you mean nobody has a crystal ball??? I do…. I used it to sell my last pure perpetual, AFINO, last week at an average price of 26.40 and it’s actually UP in price since then and even today – closed at 26.95… I probably sold to Martin and the div capture crowd I bet, ha, but it just proves I do have a crystal ball – problem is it’s a tad cloudy – permanently…….

Hi 2Whiteroses…once again…thank you for the thoughtful reply. By the way….I ended buying the Quebecor QBR.B.

I’m more then painfully aware that I know about 15% of what I should know to be engaged in this investment process I neither enjoy nor sought out. Since the death of the 5% CD and Money Market accounts in 2008 I’ve had no choice but to navigate my way through what I perceive to be this dangerous process that puts me and my money at risk because others were greedy, incompetent, not properly regulated and corrupt.

My brokerage accounts are large enough that I have one on one access to the resources the brokerage companies provide and though I enjoy spending an hour listening to these guys their approach never appeals to me and my approach seems to not register with them.

So I’m out here on my own, trying to not to loose money while not allowing my hunger for yield drive me any higher on the risk curve then I already am.

I’m a strong believer in free markets and capitalism and am in the Ayn Rand camp philosophically when it comes to self reliance…..but when investing turned into gambling and people’s life savings have to be put at risk to get through retirement…..it leaves me wondering how we got to this terrible place in our history. I guess that’s a rhetorical question because we all know the answer to that.

Richard – Believe me, we all feel as though we know about 15% of what we should know to be engaged in this investment process, so welcome to the fray. My guess is you know at least 16%, though, because you know to be here on III…. Heck who knows? Maybe some day you’ll end up seeking it out for enjoyment as well as for financial self preservation…..

Richard, I will date myself here ..but the problem to me started in the 1970’s when they eliminated 5% savings accounts guaranteed interest ( and the 5.5% guarantee you could get on 90day Passbook Savings) .. they started the attack on savers then and it is always one thing after another to make us juggle what we have to do as savers and investors.

I see this as one of the many that will be trading at 15-18$ in a few years..who is buying? ins co’s/pfd funds/pension funds etc.

Bea, and based on comments I see from neophytes buying these types on SA…If it does ever get to $18 they will be saying, “who cares, they will redeem it in 2027 and I will get all my principal back”. Those people think the word “perpetual” is synonymous with “call date”…. Ooops.

The dividends are Section 199A dividends, so in most cases, only 80% of the dividends are taxable as ordinary income.

Yikes, who would buy this? It has a negative real return.

I’m not eager, but consider this. I have some money (as do many others) in short term treasuries ( or short term CDs) paying < 1%. This offering has a four times higher yield and is tax advantaged. But if rates soar this is not going to look good.

this is not tax advantaged , “ordinary income”