UPDATE–The OTC grey market ticker is PEBBV (watch for any changes–lately they have made changes after the original announcement).

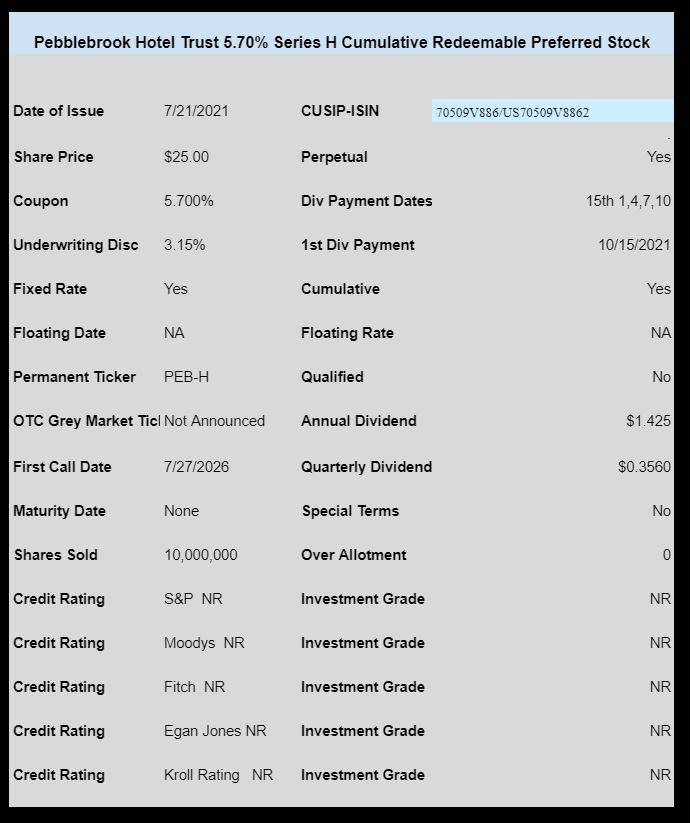

Pebblebrook Hotel Trust (PEB) has priced the previously announced new preferred issue.

The issue prices at 5.70%. They are selling 10 million shares. The issue is cumulative and non qualified.

The company intends to redeem the 6.50% PEB-C issue in full and some (or all) of the PEB-D or PEB-E issues. The 10 million shares sold is not enough to call all 3 issues unless they add cash from other sources.

The OTC grey market symbol has not been announced–although the issue will trade on the OTC prior to permanent exchange trading.

The pricing term sheet can be found here.

TDA has the quote for PEBBV AS 24.98 BID-24.99 ASK

LAST TRADE WAS IN “U” MEMBER EXCHANGE

I put in an order and it said Call the thinkorswim desk.

My trade was rejected.

Question: What’s the proper price range for a buy?

I realize it’s a low yield for a Reit.

Symbol changed to PEBBP

Thanks, EB

I did the math and I won’t pay above 25.00 for this.

One can find other REITS with higher yields.

I’ll pass on this Pebble

Figures–not certain why these changes keep occurring.

My understanding is that they trade with a “V” initially and switch to a “P” when they are trading T + 2

V -> when issued

Own both F and G – can anyone tell me why these two very similar fellows are trading 80 cents apart? G is v new, – still…

A randall – It’s the “pinned to par” aspect of F as it is currently callable where G is not callable until 2026. Knowing they did this series at 5.70 and used proceeds to call C and D seems to leave F in the clear for a call though for now.

Pebblebrook Hotel Trust (NYSE:PEB), a real estate investment trust, has acquired the Jekyll Island Club Resort in Georgia, US for $94M.

I assume that was cash.. and that means they just spent quite a bit. I wonder what that means for the other preferred… I am too lazy to try to figure out if there is an issue close to par that we thought might be redeemed but now will probably hang out for a while longer.

FC:

Likely wishful thinking. PEB had also raised $200 million via the offering of PEB+G back in May. Look for PEB+D and PEB+E to get redeemed with this massive raise of $250 million of PEB+H.

PEB has a very strong management team. They are way too smart to waste this opportunity to refinance old preferreds.

They are one of the few hotel REITs that have been trying to buy high quality hotels at lower prices during the pandemic. Also one of the few that never suspended their preferred dividends, even though they were burning $20 million/month when things were really bad.

PEBBV

Neither Fidelity nor Schwab accepting

What is issue with 4-day settlement – will broker adjust?

No. The settlement date is the 27th.