Well hoping you all had a good long weekend. We are having beautiful weather in Minnesota – “feels like fall” which is always a great season for me. Of course fall in Minnesota means we are just a few months from winter–ugh.

Equity trading was relatively quiet last week as we waited for the employment numbers all week long before seeing the extreme softness in hiring. The S&P500 traded in a range of 4513 to 4545 before closing the week at 4535 which is just short of a record closing high.

Interest rates moved in a range of 1.27% to 1.34% before closing at 1.32%–1 basis point higher than the previous Friday. The jobs report on Friday, which was very soft and should have been dovish on interest rates, turned out to not drive rates lower. When the soft jobs report was released the 10 year treasury moved lower to 1.27%, before pivoting and moving higher to 1.34% as wage gains were extremely strong in August. On Friday of this week we have PPI (producer prices) being released before seeing the Consumer Price Index (CPI) being released the following Tuesday.

The Fed balance sheet moved higher by $16 billion last week to a new record high of $8.439 trillion–no surprise of course.

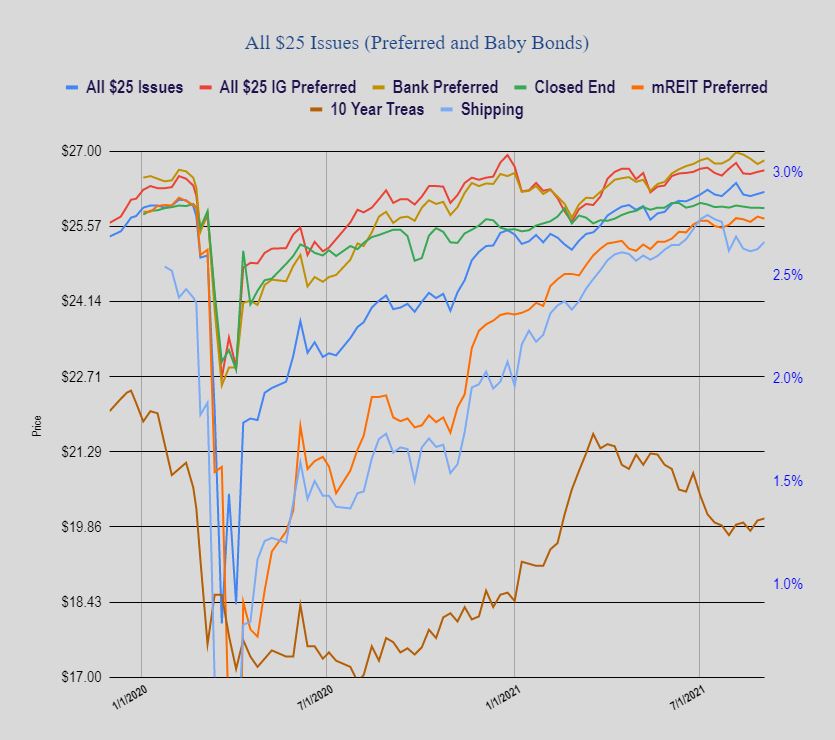

Last week the average $25/share preferred stock and baby bond rose by 4 cents. Like common shares last week it was quiet in this arena. Investment grade rose by 3 cents, bank preferreds by 7 cents, CEF preferreds lost a penny and mREIT preferreds lost 4 cents.

Last week we had NO income issues priced–unusually quiet.