Last week was a near flat week in stocks as the S&P500 traded in a range of 4443 to 4527–closing at 4464 which was 14 points lower than the previous Friday.

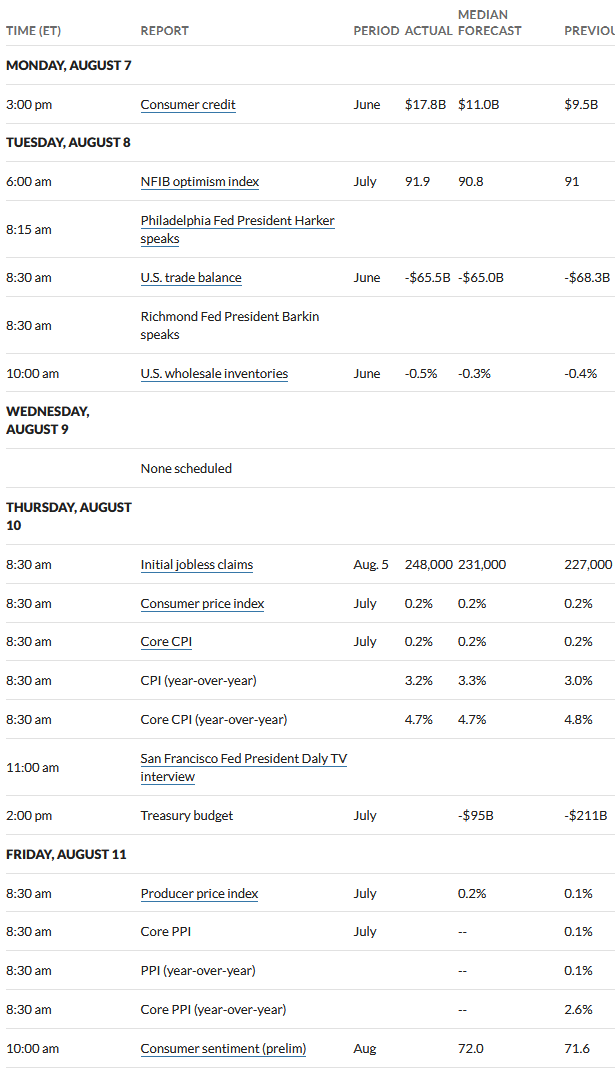

Interest rates moved in a about a 22 basis point range in the 10 year treasury (3.95-4.17) closing the week near the high at 4.16% which was 10 basis points higher than the close the previous Friday. Rates were buffeted by an on target consumer price index, but the next day rates were sent higher by a producer price index which came in hotter than anticipated.

This week we do not have the normal market moving economic numbers being released, but on Wednesday we have the FOMC meeting minutes from the July meeting which will be closely reviewed by all – of course it is all really old news, but the algo’s will send equities either sharply higher or sharply lower.

The Federal Reserve balance sheet grew by $2 billion last week – a rare increase in a downward trending balance sheet.

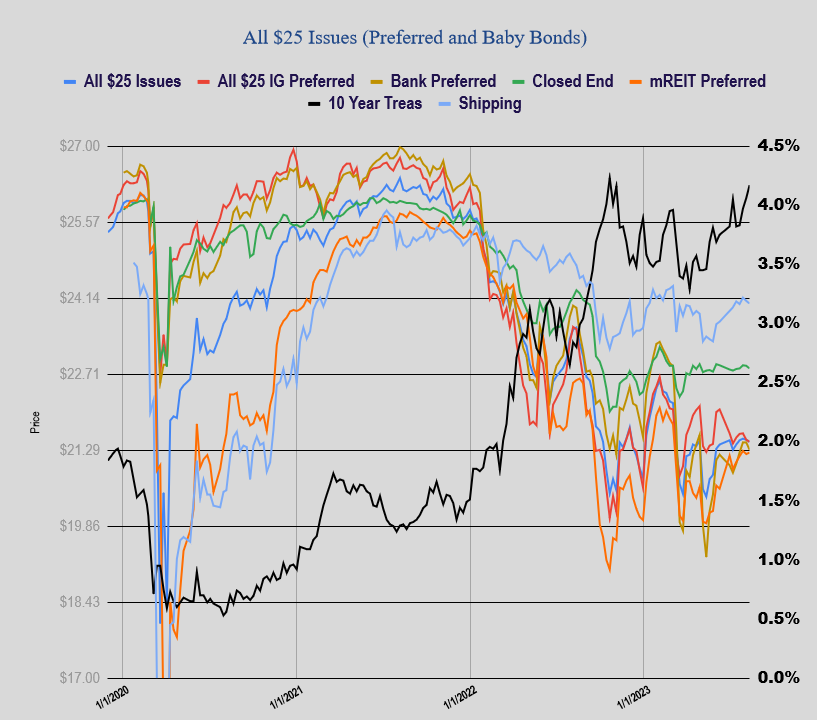

Last week–for the 8th week in a row $25 preferred stocks and baby bonds barely moved–the average share was 4 cents lower. In the last 8 weeks the average share has moved in a 21 cent range. Investment grade issues were 4 cents lower, banks were 12 cents lower, CEF preferreds were down 5 cents, mREIT issues moved 4 cents higher with shippers off a nickel.

Last week we had 1 new income issue priced as junky business development company Great Elm Capital (GECC) priced a new issue of baby bonds with a coupon of 8.75%–the issue is not yet trading, but look for it to trade this week.

Hi, Tim:

You used to have a sheet with Hi/Low volume (current day’s volume compared to average trading volume). Has that been elinimated? If so, is there any place on the site (or, if not, any other place that you know of) that lists preferred stocks by average daily trading volume? Thanks!

Hi Robert – I don’t remember that at least in recent times. The problem with something like that is Google quotes (and volumes) are so unreliable that I have to use workarounds for prices and can’t get volumes on many issues. I’ll look back through the spreadsheets and see if there is an old one with volumes on it.

Hi Tim,

Thank you for the response….If you Google, “hi low volume preferred stock trades” you will (hopefully!) see the first two entries that refer to III sheets. Those are what I was referring too. (Not sure how old they are.)

Robert

Franchise Group preferred FRGAP is expected to get redeemed this week as part of its go-private deal. Not my game, but the dimes-in-front-of-a-bulldozer crowd may want to take a look. It’s trading under par and will likely have a stub dividend. Just sayin’

Interesting – Looks like it’s “worth” about $25.24 or thereabouts when redeemed this Friday.

Bear and yazzer,

From what I see, FRG shareholders will vote on the proposed FRG merger on Aug 17. The redemption of FRGAP is contingent on the merger occurring.

I’ve no idea what the probability is of the FRG merger, but as of now it may be less than a 100% certainty.

You probably already know this, so I mentioned it in case some of us on III didn’t know this and are considering stacking a few nickels by buying FRGAP under par.

2WR and mbg – yeah I saw that – but it looks like that process is just a formality as the Board is recommending a passage and I did not see anything of a push to get the shareholders to not approve. That said, anything can certainly happen, We’ll see. If it drags a few days, like you said, it just accrues more interest.

If it indeed somehow does not get approved, the risk is a drop back down to ~$22 and I become a bagholder! You are correct, the stock is trading slightly lower than par in an oft chance it doesn’t get approved.

FWIW, my suspicion is that it is too optimistic to believe FRGAP gets called this week. The shareholder vote is Thursday and the the conditional call is for Friday – https://www.glowswire.com/news-release/2023/07/19/2707785/0/en/Franchise-Group-Inc-Announces-Redemption-of-7-50-Series-A-Cumulative-Perpetual-Preferred-Stock.html

However, I suspect the conditional call notice was issued for the purpose of satisfying the 30 day notice provision. Assuming approval on the 17th, usually the actual closing cannot happen the next day, so I’m guessing FRGAP will be outstanding a little while longer… However, if it is, you continue to get paid a little bit more each day, unlike the common shareholders… The real risk is that the deal does not go thru at all for whatever reason, but FRGAP shareholders continue to get more accruals every day it’s outstanding beyond the 18th.

Update – shareholders approved the merger/take private so it’s all done it seems. I ended up with 600 shares at $24.91 and looks like they are worth a minimum of $25.17 now and will accrue till the call executes. A few sheckels to keep. LOL.

Ended up getting some at $24.90. Their last ex-div date was 6/30, so 49 days to 8/18 redeem date. I calculate 25.17c in divvy and another 10c in equity pricing or 35.17c. That translates to +1.4% for a 4-day hold (127% annualized if that means anything here). What the heck – 1000 shares gets you a little over $350 in 4 days – a case of nice pinot noir. That’s if I did my calculations correctly.

Full disclosure, I did not go a full 1000 shares – just used that as a round number. I did pony up for 400 shares, however.

I believe accrued interest starts from the last coupon pay date of 07/15 (not from the last ex date) which would mean 33 days accrued interest on 08/18.

True but yaz got the math right….. was wondering why he mentioned x date at all…

Brain fart!

Looks like GS-J is a goner…

“We intend to use the net proceeds from the sale of the depositary shares representing interests in the Series W Preferred Stock to redeem all outstanding shares of the Series J Preferred Stock and any remainder of the net proceeds to provide additional funds for our operations and for other general corporate purposes, which may include, but is not limited to, repurchases or redemptions of other outstanding shares of our preferred stock and related depositary shares.”

https://www.sec.gov/Archives/edgar/data/886982/000119312523211536/d541724d424b2.htm

Makes you wonder how much conviction they really have in this call…

https://www.bloomberg.com/news/articles/2023-08-13/goldman-pencils-in-first-fed-rate-cut-for-second-quarter-of-2024

30 days notice is required?

1000 structure w price talk 7.875% area…

Thanks Dick

Any word on the new OCSL- symbol, trading etc?

Gary–wasn’t that a $1000 issue? I’ll look.

Tim, welcome back! I look forward to your morning commentary.

BTW. The FOMC meeting minutes are not necessiarly old news. To provide full transparency, the minutes are updated on a contiunal basis to reflect current FOMC thinking, some of which is in the news.

Cheers!

Thanks windyducat–I’ll quit referring to them as ‘old news’.

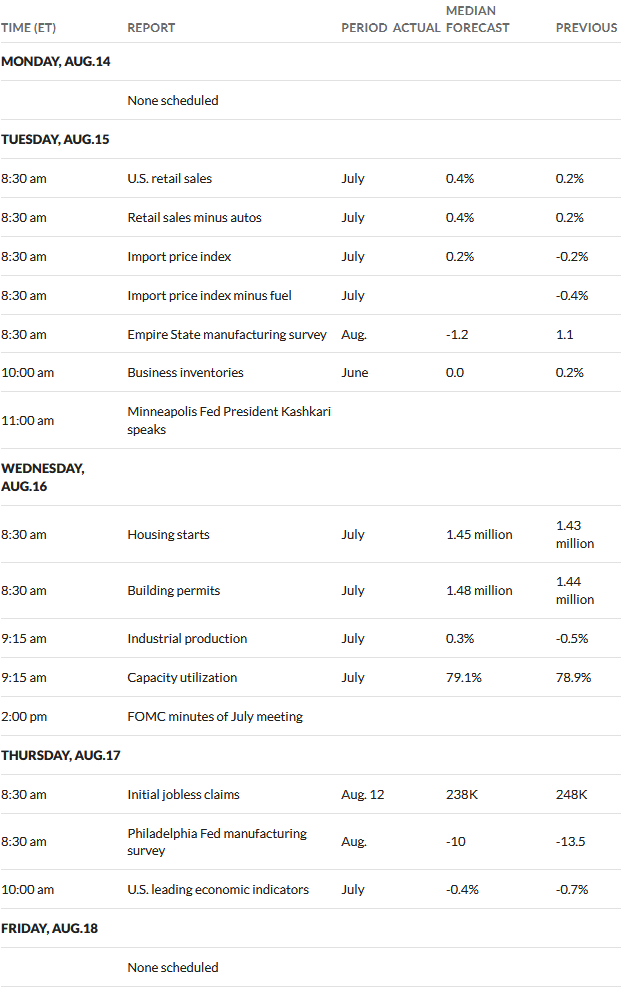

Wed for when the housing starts and building permits is of interest. Wish there was a report on transportation, volume of shipping of freight by trucking and rail. With Yellow closing down and liquidating ( yes, even though it’s chapter 11) will be interesting. Our Fedex driver told us they had been rotating driver layoff’s at his terminal so they will pickup business. Said the last time it happened most of the new business stuck around. We have a ad for a driver in our Southern Cal location and we saw a surge in applications but it’s not a class A position and not union. Gas was up again last week and will affect transport costs. I started buying Alfalfa for the winter, down to 24.00 a bale compared to 28.00 the kids load the pickup and I just have to unload and stack it up. So far 24 bales and 1 pickup load to go for winter.