It has been rare in the last few months, but last week the S&P500 fell. The Friday close was 4478 which was 104 points lower (-2.3%) than the previous Friday. The Fitch downgrade of U.S. debt gets the blame for the tumble as investors needed to find a reason to lock down some gains.

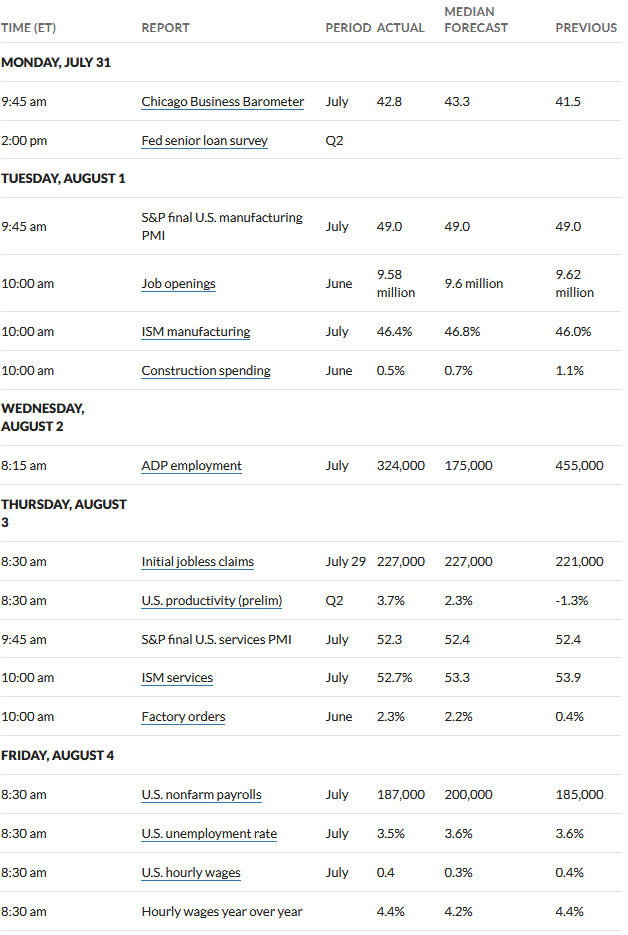

The 10 year treasury yield rose sharply to close the week at 4.06%, but had been as high as 4.20% earlier Friday. Rates moved off the high as the number of jobs created for July came in lower than the forecast – wages continue to grow at a high rate at +4.4% year over year.

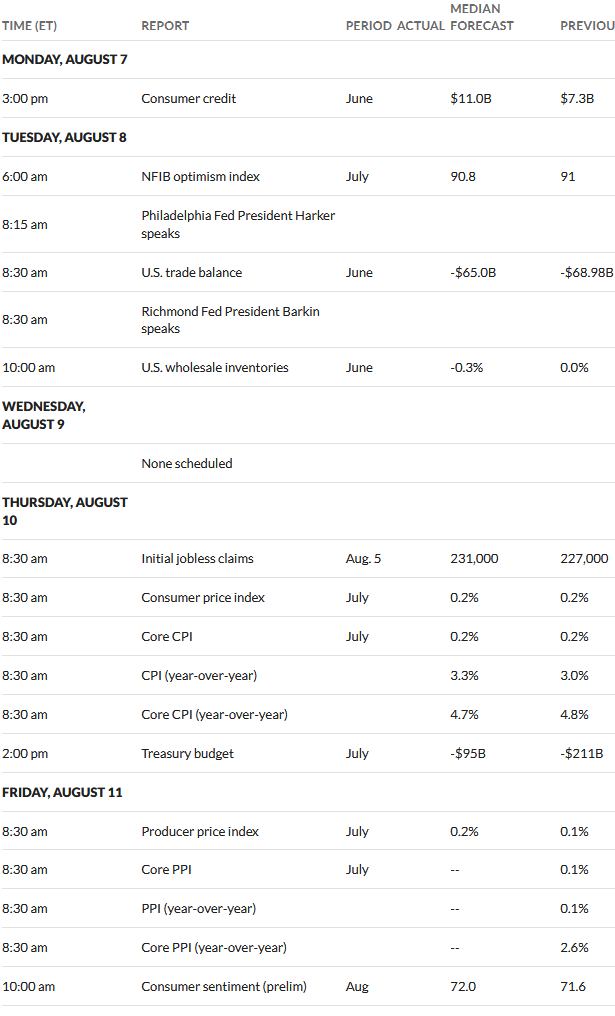

This week we have plenty of economic news with the consumer price index (CPI) and producer prices (PPI) being announced on Thursday and Friday. These have been relatively tame as of late–can it continue?

The Federal Reserve balance sheet assets fell by $37 billion – still at $8.2 trillion. I guess falling is better than rising, but the best thing one can say is that we are building potential balance sheet powder for the next black swan event–whatever and whenever that occurs.

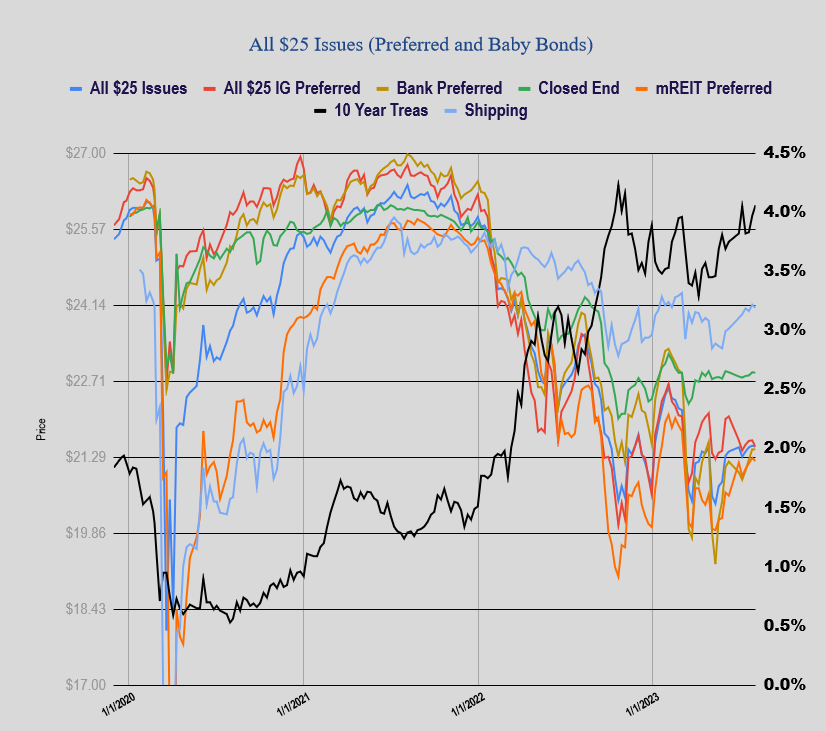

Talk about flat markets—the average $25/share preferred and baby bond was off 3 cents last week—so in the last month the average share has moved in a 10 cent range. Investment grade issues were off 12 cents–banks were dead flat, mREIT preferreds were off 6 cents and CEF preferreds were off 1 cent. Pretty tight trading considering the movements in interest rates.

Last week we had no new income issues price.