The S&P500 moved sharply higher last week closing at 4505 which was 107 points above the close from the previous Friday – about 2.4% higher. Honestly with the amount of liquidity that is out there it is pretty hard to keep equities lower. I suppose that one of these days we will see a ‘black swan’ but it sure hasn’t been recently. Equities are moving higher even though there are vast amounts of money hiding out in CDs, treasuries and other competing investment choices–when/if interest rates move lower we could see a crazy stampede into equities–the available ‘dry powder’ is massive.

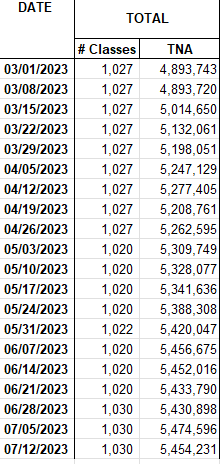

Here is a listing of how much is in money market funds for the last 20 weeks–lots of potential ‘dry powder’–$5.6 trillion is significant.

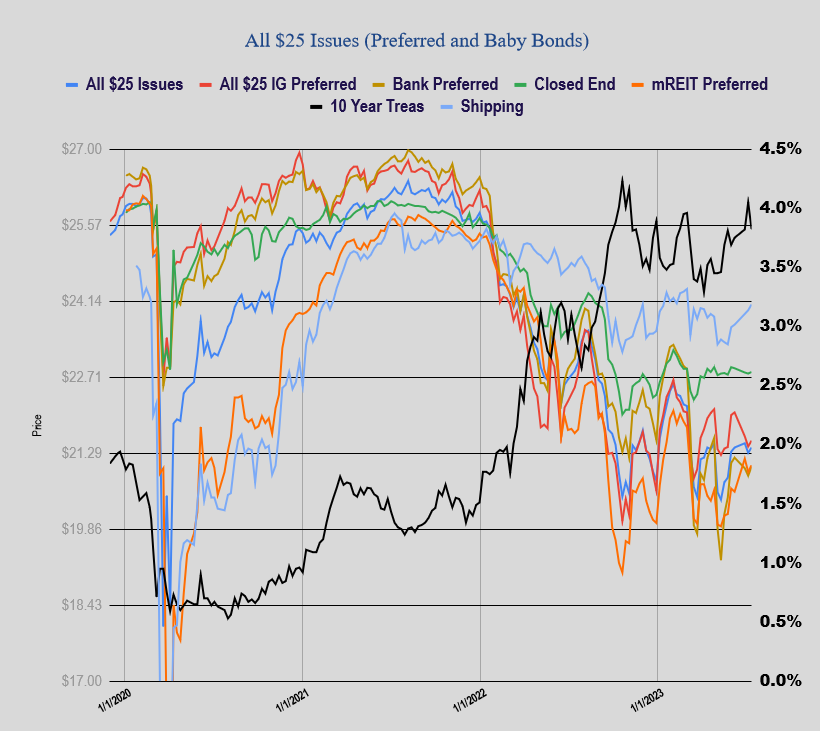

The 10 year treasury yield tumbled hard last week–closing at 3.82% which was 23 basis points below the yield from the previous Friday. Lower than expected consumer and producer prices opened the door to a bond rally.

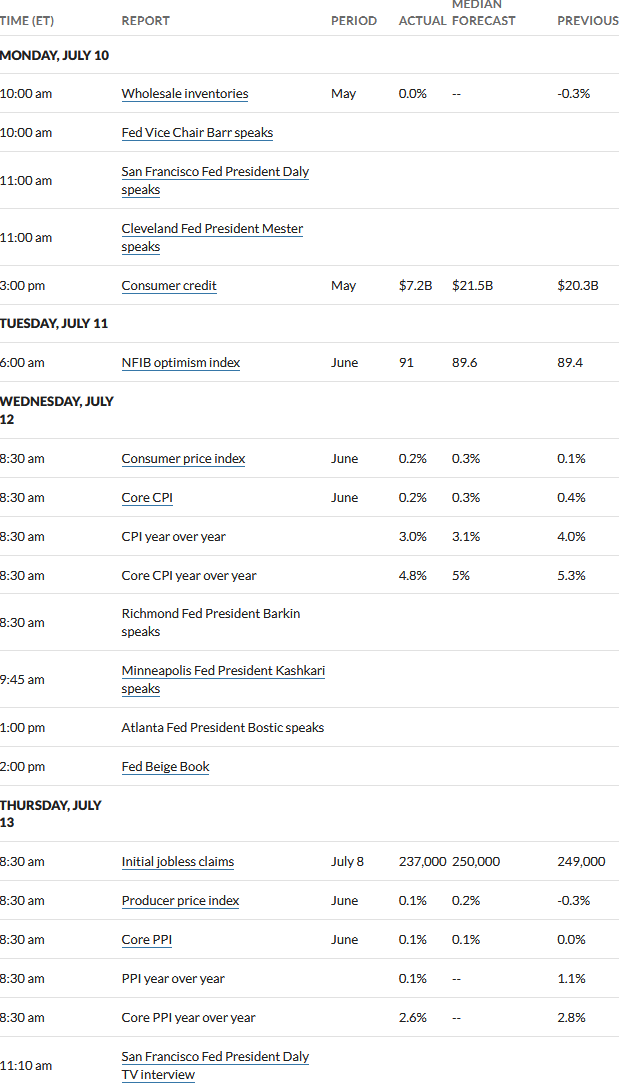

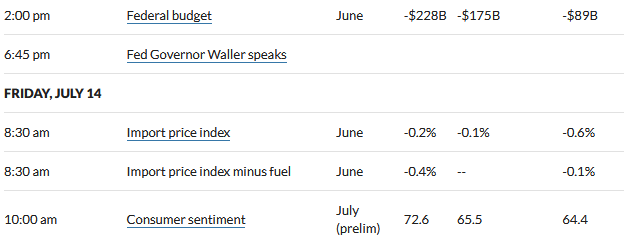

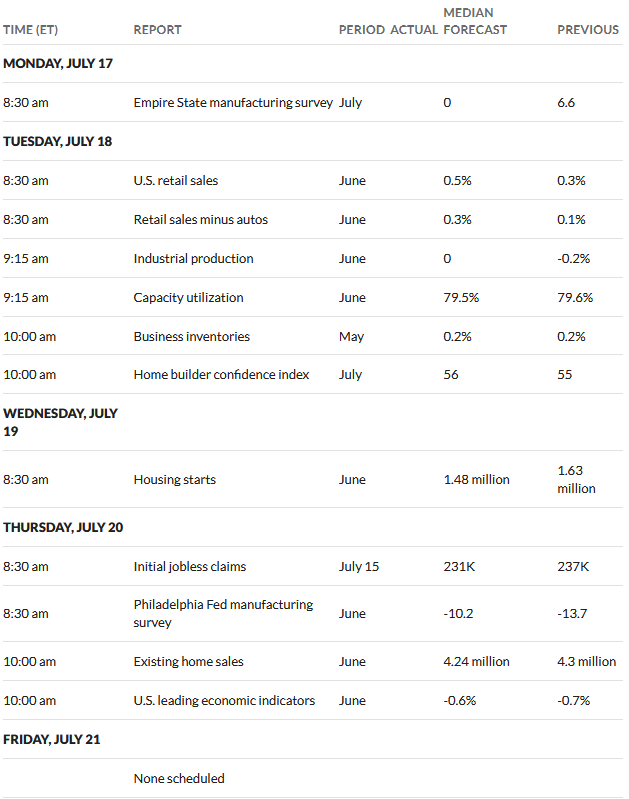

This week we have lots of housing related economic news shown below. None of the economic news on the week is what I would call ‘market moving’, but with the FOMC getting together next Tuesday everything has some level of meaning relative to interest rate decisions.

The Federal Reserve balance sheet fell by a measly 2 billion—just a pause because of runoff timing.

Last week we got a modest bounce in $25/share preferreds and baby bonds with the average share moving 10 cents higher. Investment grade moved 11 cents higher, banking issues 17 cents higher with CEF preferreds up 3 cents and mREITs up 13 cents and shippers up 11 cents.

Once again we had no new income issues priced last week.

Best estimate from the clever Wall Street prognosticators say October is the month all the $Covid$ liquidity money dries up….Humm..! They keep moving the goal post back a few yards every month?