The S&P500 fell by just over 1% last week in what was a holiday shortened trading week. At 4398 the index remains just over 1% off of a 52 week high.

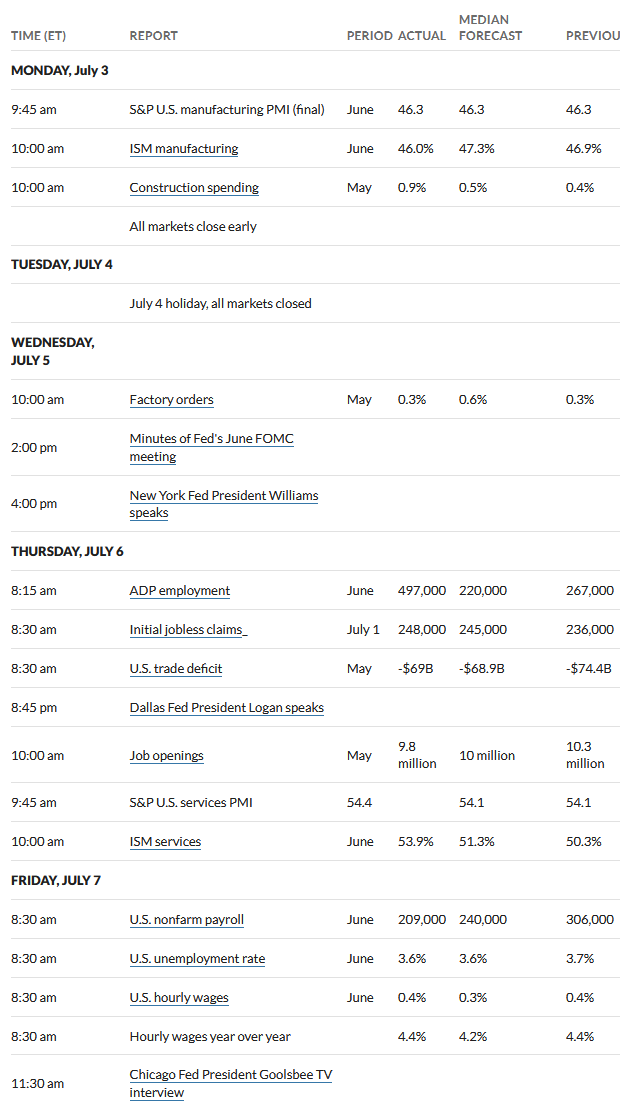

Interest rates closed at 4.05% (the 10 year treasury) which was a giant jump of 23 basis points from the previous Friday. Rates moved in response to employment number from ADP–which showed employment exploded higher. Of course the ‘official’ government employment report which was released on Friday showed a much more muted employment picture.

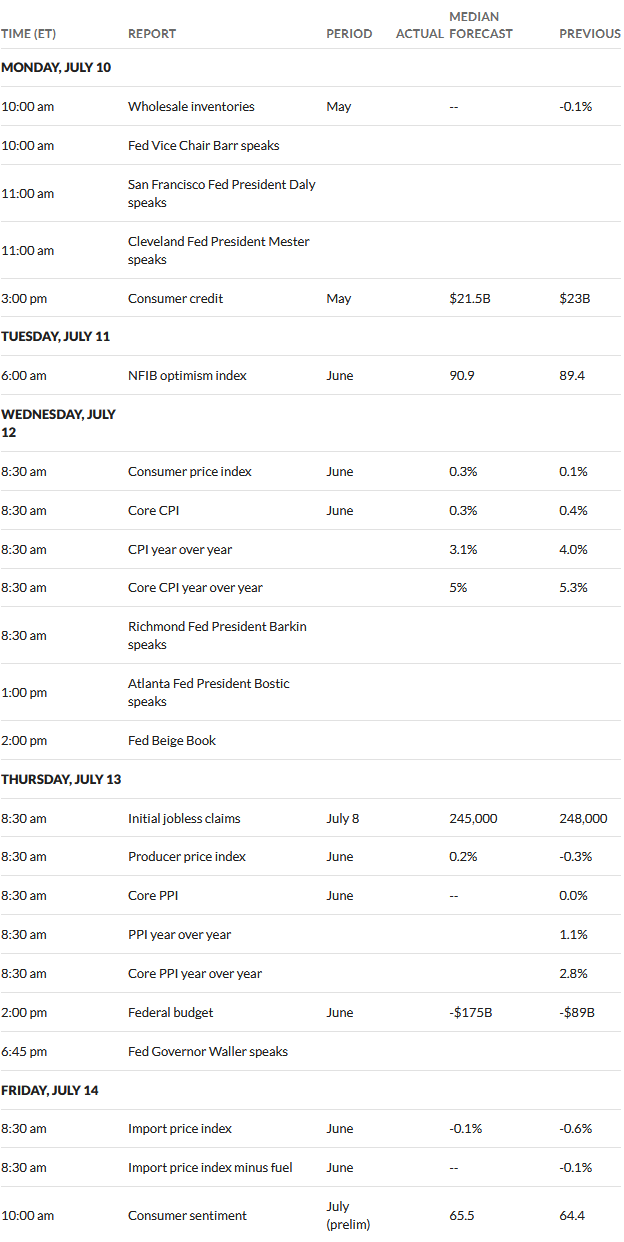

This week we have the consumer price index (CPI) being released on Wednesday and the producer price index (PPI) being released on Thursday. You know these will be important and will probably cement the 1/4% Fed Funds rate hike the end of the month (in my opinion).

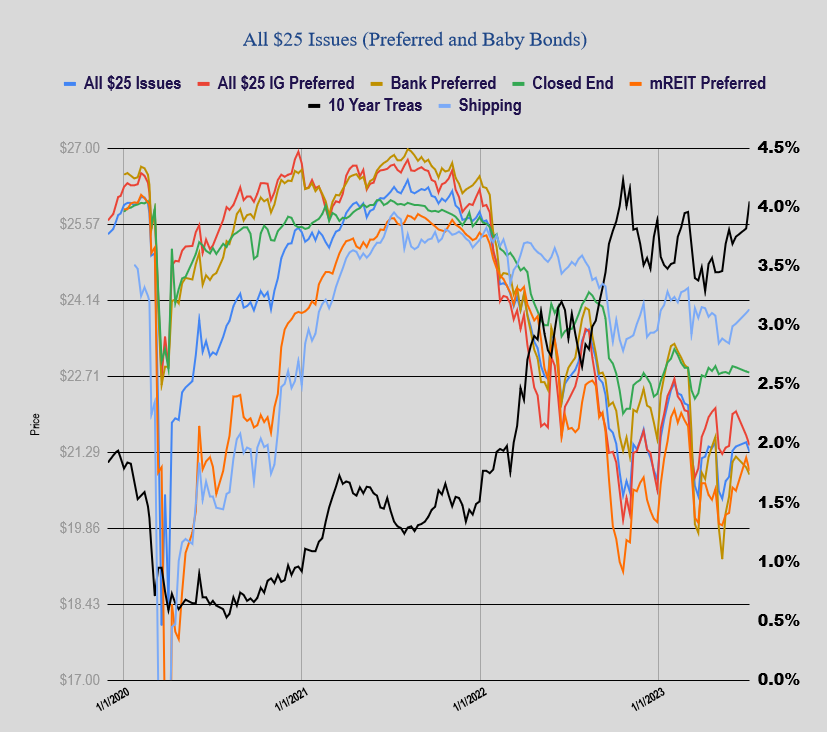

Last week the average $25/share preferred stock and baby bond fell by about 18 cents last week. Investment grade fell by 19 cents, banks by 14 cents and mREITs by 26 cents.

The Fed Balance sheet fell by a pretty large $42 billion last week–with that drop the balance sheet is now at a lower level than just before the ‘banking crisis’ in early March. With interest rates moving higher I question how long this reduction will continue.

Last week we had no new income issues priced.