Last week the S&P500 closed at 4105 which was just barely off from the previous Friday close of 4109–off course the week was a short week with the Good Friday holiday.

The 10 year treasury closed the week at 3.29% which was a full 20 basis points lower than the previous week, The employment report which was one of the important economic data points on the week was a mixed bag–softer than forecast new jobs created, but a lower unemployment rate.

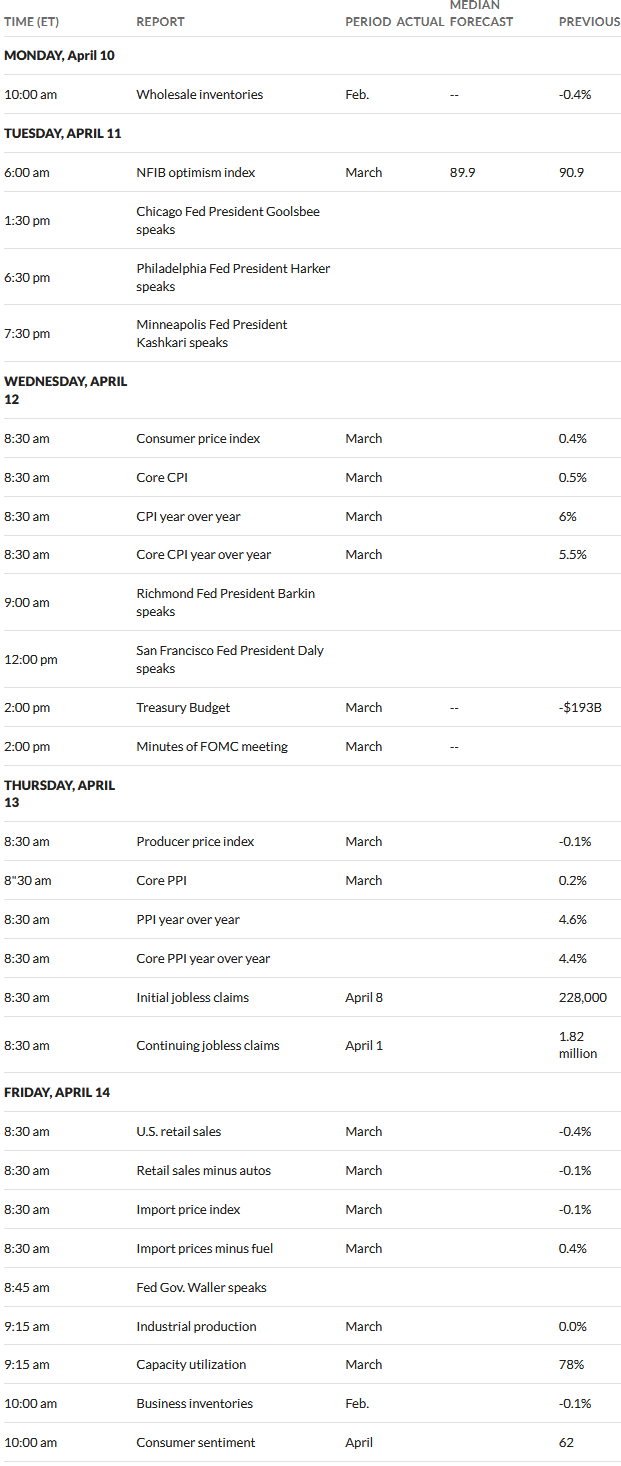

This week we have a number of important economic report–in particular the consumer price index (CPI) release on Wednesday. In addition to the actual data releases we have Fed Presidents talking almost daily–I think they will begin setting the path for a 1/4 point rate hike in May after the FOMC meeting.

After a giant $400 billion move higher in response to the banking crisis the Fed’s balance sheet fell for the second week in a row – down $74 billion on the week. The balance sheet is off $100 billion in 2 weeks.

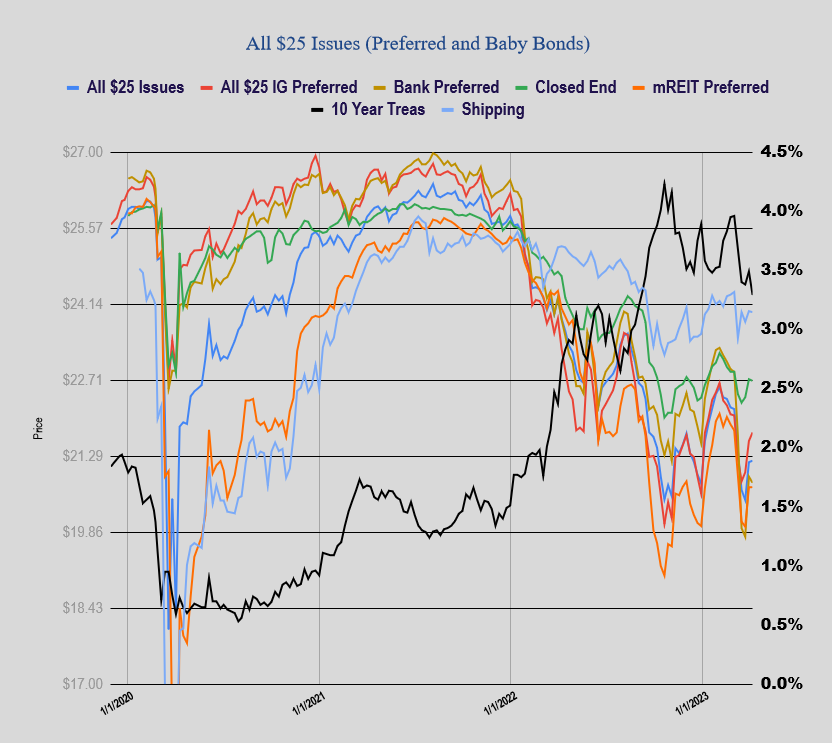

Last week surprisingly the average $25/share preferred and baby bond was virtually flat – plus 3 cents. Investment grade issues were up 16 cents, banks down 12 cents, mREITS dead flat and shipping issues down 2 cents.

Last week we had no new issues priced.

GLOPpA ,B ,C revisited ; GLOP was delisted back in August. who is responsible for paying the dividend on these preferred shares? if there is a Parent, I could not find it on Quantum ;

Shipping stocks are not sleep well at night holdings. There is money to be made but you can’t just watch one stock.

They are like oil extraction stocks. They are subject to boom and bust cycles as they over build on ships.

Some LNG shippers are using ships as floating storage in Europe and other places. Right now I think is good but 2024 & 2025 a lot of new build ships will be delivered.

Just for example another LNG shipper listed in Norway this past month listed on the NYSE

question on another issue; anyone own GLOP+A,B orC ? the parent GLOP is being taken over by the general partner GLOG and will no longer exist; question what happens to these preferreds ? they took a big hit this morning ; they could become preferreds of GLOG or worse case become orphans ; and may cease to trade at all ! any thoughts ; prospectus probably has it somewhere i’m going to try to find it

No, it’s not in the prospectus.

Thursday’s press release says they will continue to trade on the NYSE, so I’m surprised at the weakness today.

https://finance.yahoo.com/news/gaslog-ltd-gaslog-partners-lp-203900157.html

Directly from the press release; “ The preference units of the Partnership will remain outstanding and continue to trade on the New York Stock Exchange immediately following the completion of the Transaction. (..)”

Azure, David, Ted:

The language cited in the GLOG/GLOP PR is what Hoegh said, too, more or less, on two different stock exchanges:

“The Partnership’s 8.75% Series A Cumulative Redeemable Preferred Units (the “Series A Preferred Units”) will remain outstanding.”

https://www.hoeghlngpartners.com/announcements-and-press-releases/press-release-details/2022/Hegh-LNG-Partners-LP-Announces-Completion-of-its-Acquisition-by-Hegh-LNG-Holdings-Ltd/default.aspx

“The Partnership’s 8.75% Series A Cumulative Redeemable Preferred Units (the “Series A Preferred Units”) will remain outstanding. As a result of the completion of the acquisition, the Common Units will no longer be listed on any quotation system or exchange, including the New York Stock Exchange. The Partnership’s reporting obligations with respect to the outstanding Series A Preferred Units under the United States Securities Exchange Act of 1934, as amended, and the NYSE remain unchanged.”

https://newsweb.oslobors.no/message/571914

+++++

I’m simply trying to show how little these pre- and post-merger statements about continued listing really mean. They can say one thing one day and delist it the next. In the circumstances, it makes the Hoegh / HMLPF delisting seem a bit more pernicious in my view.

I disagree that the language is similar, since Hoegh didn’t say that HMLPF would continue to be listed.

Also, I note that GLOG-A is still listed.

Therefore, I tentatively concluded that GLOG/GLOP mean what they say, and I bought a little GLOP-B this morning. That was obviously poor timing 🙁

GLOP.B set to float this upcoming quarter resulting in coupon close to 11% (Plus 5.83 over 3ml) I have gtc bid at 21.50 fwiw

Hi David – I’m not saying you’re wrong, I’m saying it’s difficult to tell what will happen. Rather than looking at press releases, it’s probably a good idea to look at the terms of the merger deal. In the case of the GLOP preferred shares, the merger document says:

+++++

(e) Treatment of Preference Units. Each Preference Unit that is issued and outstanding as of immediately prior to the Effective Time will be unaffected by the Merger and shall be unchanged and remain issued and outstanding in the Surviving Entity, and no consideration shall be delivered in respect thereof in accordance with the Partnership Agreement.

…

(d) Notwithstanding anything to the contrary herein, during the period from the date of this Agreement until the Effective Time, if permitted by applicable Law, the Partnership shall declare and pay regular quarterly cash distributions to the holders of each of the Common Units, the Series A Preference Units, the Series B Preference Units and the Series C Preference Units, respectively, consistent with past practice; provided that in no event shall the regular quarterly cash distributions declared or paid by Partnership to the holders of Common Units be less than $0.01 per Common Unit.

https://www.sec.gov/Archives/edgar/data/1598655/000110465923042971/tm2311977d2_ex2-1.htm , page 4 and page 18

+++++

Sounds pretty good, right? But compare that language with similar “deal document” language from ATCO, which made continued preferred shared listing an explicit part of the deal:

+++++

Section 8.11 Continued Listing of Preferred Stock. From and after the Effective Time, Parent shall cause the Company to continue to cause the Designated Company Preferred Shares (other than the Series J Preferred Shares) to be listed on the NYSE.

https://www.sec.gov/Archives/edgar/data/1794846/000119312523004976/d313377dex99a1.htm , page A-64.

+++++

“From and after ….” All things considered, I prefer the stronger language like that included by ATCO – an ongoing, continuing obligation – not language with temporal limitation weasel words, such as “immediately following the completion of the Transaction” as the GLOP PR phrased it.

I agree that the fact the GLOG-A shares are still listed and SEC-compliant is a good sign for the GLOP preferred shares. Perhaps (like Tex the 2nd says a lot) “this is one of those unknowables”.

Back to the GLOG / GLOP merger discussion and the potential delisting of the various preferred shares … Also of note is that Chairman Peter Livanos has over the last couple of years purchased 201,457 shares of $GLOG.PA shares, even paying over “par” for them:

2022 purchases: 119,741 shares

https://www.sec.gov/ix?doc=/Archives/edgar/data/1534126/000110465923028175/glog-20221231x20f.htm#ITEM16EPURCHASESOFEQUITYSECURITIESBYTHEI

2021 purchases: 81,716 shares

https://www.sec.gov/ix?doc=/Archives/edgar/data/1534126/000110465922032040/glog-20211231x20f.htm#ITEM16EPURCHASESOFEQUITYSECURITIESBYTHEI

+++++

No guarantee that the GasLog shares will continue to be listed and financials filed with the SEC, but pretty strong evidence the GLOG-A shares will continue to be paid, I’d say … 😉

FRC – suspending dividends on all preferreds. Will be interesting to see how badly that hurts the banking preferred sector this AM

There is trouble brewing in the financial sector and those banking preferred shares are noncumulative which means missed dividends are not going to be repaid.

I’d be careful to throw every regional bank in the same bucket. There’s likely money to be made by knowing the difference between a bank like FRC and FCNCA.

FCNCA has paid dividends on it’s common for the last 33 consecutive years. A lot of scary things have happened in the last 33 years folks. The current yield of FCNCP is around 6.5%.

Some trade on NGS , other OTC – strange.