Last week continued to show us plunging stock prices with a loss last week of 3.3% for the S&P500. Of course Friday was a painful grinding lower day for the index. I suspect this will continue, but there will be days with bounces.

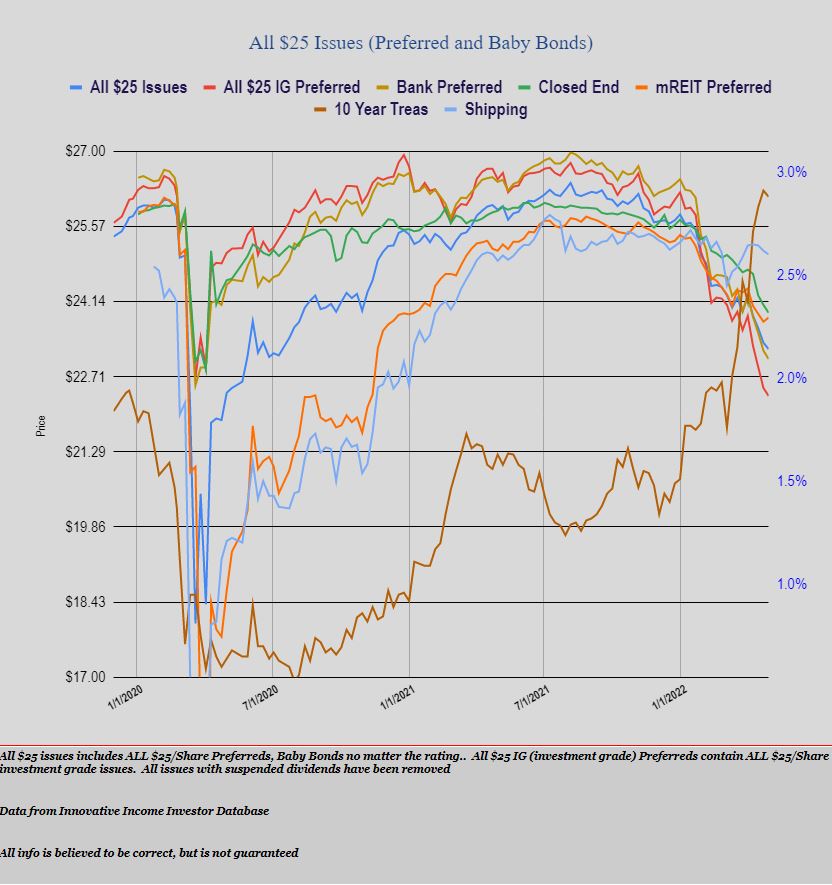

The 10 year treasury traded as low as 2.72% last week and as high as 2.93% before closing the week at 2.88% which was 2 basis points below the close the previous week. This week we have the FOMC meeting starting Tuesday with a Fed Funds rate increase announcement on Wednesday–likely a 50 basis point hike. A 75 basis point hike would likely be very upsetting to the markets.

The Fed balance sheet fell by $17 billion..

Last week the average $25/share preferred stock and baby bond fell by 12 cents. Investment grade issues fell by 15 cents. Banking issues fell by 16 cents with mREIT issues rising by 8 cents. Shipping issues fell by 7 cents.

Last week we had no new $25/share income issues priced–no surprise in these days of rising interest rates.

Is it safe to start buying preferreds yet? Talk about wealth destruction 😬

Tropical, Are you refering to the IG perpetual preferreds? As many that are not those are still positive past 12 months and YTD including dividends. The key has been to avoid those. Higher yielding adjustables such as NSS and CUBI-E have held strongly and high yielding higher quality issues like CEQP- have done well too.

Those lower yielding IG ones, its a tough call. Prudence would be to be patient still, but who knows.

I didn’t do a large intensive search but when ATT and banks started hitting 6%+ my interest in buying perked up. Who knows 5 to 6 under par may become 7 to 8…

Tim–This is the first time I’ve posted–but I visit the website religiously. Thank you for the service! A while back you had mentioned CTBB and CTDD in the second part of the 7% articles. How are you feeling about them now? The yield on CTDD is 7.62%. I realize that it could still go higher.. Thanks in advance for your time.

Hi everyone, new to the site here, but very interested in ETDs. I am currently tracking all the Brooksfield issues (BIPH, BEPH, BAMH), the mother company is very solid and the issues are relatively new and therefore get beaten down more when rates rise.

My question to you, that have more experience with these instruments, if rates keep rising are we likely to see more downside on the ETDs or do you expect them to stop falling after a while? (all other things being equal: i.e no company troubles)

Those preferreds will move with both equities and bonds. If both stocks and bonds keep falling, they’ll fall further. If stocks go up and bonds fall, they might stabilize. If stocks and bonds go up, they’ll bounce a lot.

They shouldn’t move much with stocks in theory but from experience, they just do.

End of day rally manufactured two straight days. Is it time to start playing for it?

Martin G – I don’t think the market is that predictable. Just when you’re trying to play it, it will play you into the red. Consider this instead.

Here’s a game I love to play with the market. Take SBUX today, at $74.20 as I write. SBUX is 40% off it’s 52-wk high. It has an $1170 1/19/24 premium, with a $75 strike price. Has a safe $1.96 per share dividend (2.63%). I’m willing to purchase 100 shares ($7420) and if I conceptually divide that premium into 2 years (1170/2) I get $585/yr. Add that $585 to the $196 annual dividend (div not at risk) = $781. Divide $781/$7420 cost basis = 10.53% dividend equivalent for each of the next 2 years. If I want to conceptualize that premium out to the next four years, I divide the premium by 4 yrs (1170/4) = $293, add to the annual div $196 = $489/$7420 cost basis = 6.59% guaranteed for each of the next 4 years. But of course, when the covered call expires on 1/19/24, I’ll sell/write another LEAP covered call so that 6.59% guaranteed dividend equivalent over the next 4 years is actually a floor. And, if the shares are called away I’ll make north of 10% annually ROI – depending on when the shares are exercised.

So, b/c I’m willing to buy 100 shares, I like to start by purchasing just 3 shares. If they go up, fine, I take a 100bp profit minimum. If they go down a 100-150 bp, I’ll buy another 3 shares. If it keeps going down I’ll purchase the bulk of the 100 shares at some point and write the CC. It can’t outrun me. It might sound silly taking $3 profits, but over the past 3 years I averaged $1831/yr on it (and it was fun) AND where the price went down, I wound up with much better entries on the 100 shares/CC.

But more importantly and excuse my language, it’s nice to have the market by the balls so to speak. I, in my mind, give the ultimatum to the market – either you give me a small profit, or you decline in price (which is what I really want) and give me a bigger profit when I finally purchase the balance of the 100 shares and write the covered call.

Time for spring cleaning. Sold off the riff-raff for losses, consolidated into one issue where I had multiple issues from one company. Picked up some short-term senior bonds, as well as some beaten-down blue-chip equities with covered calls.

The benefits are increased portfolio quality, better diversification.

Treasury rates up > 3.5% today – yowzer. What changed today?

They track interest rates generally … Bonds are lower this am.

Just a little historical perspective on interest rates…..the 10yr Treasury had a low on 3.90 in 1963…ultimately climbed to 15 or so in 1981….now if you apply TA(technical analysis)…support becomes resistance…the support of 3.90 was broken in 1982….now 3.90 has become resistance…..we seem to be heading in that direction.

I developed a small tracker list of preferreds issued last year that have been taken to the woodshed. Still watching and thankfully because not only have they been dragged behind the woodshed, there was a second woodshed just built to beat them again even harder behind it today. Many these are taking 3%-4% haircuts just today, wow. But still logical none the less.

Yep, last time inflation was this high it took a lot more than a few tepid interest rate increases to tame it.

If it takes raising rates 5-6% we should all get in the woodshed supply business!

I am sitting on a huge cash position now, and what is invested is term, floating, or locked up to where I couldn’t trade out of it.

Im trying to stay at the end of the woodshed beating line, but I have started the initial dabbling as I bought a few hundred more of SJIJ at $17.05, keep averaging down in small lots. Im not finding anything that agencies are going to tongue lash like they did PSB. The SJI bond market sister subordinate debt still ignoring it all with a 5.5% ish 2031 maturity. Its in the same boat, but SJIJ is the one that will pay the price liquidity wise and price loss…. When does the falling knife stop falling? Toed gently in for a few hundred of CMS-C at $17.95. Would love this one to spill under $17… My worst beating stock I own is the EIX 5.375% reset. And the lower it goes the more compelling it becomes. If it can drop a bit more to $900, that 4.69% reset plus 5 yr., suddenly becomes a 5.21% reset plus 5 year.

If and buts were candy and nuts… But a $900 handle with a 4.69% plus say a current 3% 5 year come 2026 reset time makes this a bloated 8.54% QDI at reset. Im really trying to dislodge myself from all my issues that are trading firm and roll into these or roached out issues to benefit from the counter wave. But Im staying patient mostly and holding cash too.

Gridbird

How concerned are you about SJI going private with respect to the baby bond of SJIJ?

David, Im not worried because it is happening. They clearly spent an entire paragraph in merger discussing they will be private will reveal no financials and will not report any. And the company acquiring will directly pocket all the money saved over time from not complying. This was meant that the rate payers wont get any of it.

So yes I perceive worst case scenario. At 8.20% that is a nice annuity. But I will limit my purchase scope because of what will likely happen.

Grid, SJIJ with a current yield of 8.25%; if I told you just’s couple months ago that is where this 5.625% coupon Junior Subordinated Notes due 9/16/2079 would trade here, you would think I was insane. I will definitely be buying this bond 🥳

Grid, thanks so much for identifying this jewel. I quickly cancelled DSX-B, currently safe but with some call risk and bought SJIJ. I also picked up the same in my other accounts with all the money from SB-C partial call. Bought quite a few shares of ATCO-H. Old Seaspan got the largest container ships. However, one of their ships sailing to Singapore was refused disembarkation because the goods apparently were to be sent to Russia. Their common stock seem to ignore the news (which actually showed up in DLNG (Sold all my DLNG B). Your old FATBY came back alive. I did not re enter. Who knows if the issuer could also issue preferreds and commons at will, as the old busted GMLP common and its grandpa, trashing GMLP common ending in the pink sheet GMLPF. The Barrons call Jeff Gundlach the new Bond King. I lost lots of money in buying and buy more the now defunct GMLP and its father. They should give you the title. Ha Ha.

Was SB-C another one of those ‘lottery’ situations?

I had about 65% taken from my TDA account and nothing so far from Fidelity.

It is rated bullish at Fidelity with their compusta as SAFE

Leverage is low because owners of the public company has another private company which the two Greek brothers are the sole owners. They have started to finance new custom made large scale ships manufactured in Japan and spent tons of money get most of them certified meeting the European climate change regulations (not fully enforced to my knowledge), meeting the US Coast Guard standards. About 5 years ago, SB was deemed the first shipping company mostly likely to file for bankruptcy. Dividends to its preferred share holders were never suspended. After they finance the ships themselves from their private company and then lease it back at fair market value, EBITDA climbs steadily. Now, with GAAP earnings and they started paying $0.05 to it common shareholders. The two Greek brothers have at least 20% of common and preferreds. Potential risks: resumption of trade war. Current charter and daily shipping rates is positive to my knowledge. Mixed bag. I do not recommend their preferreds at this time. Fully valued or perhaps overvalued. My cost basis is all near par, most of them BELOW par.

Yes, 8% plus is very nice, but it has to be assumed worst case scenerio its going to experts market. So it really needs to be assumed it will be private debt annuity payments. If anything else more positive comes out of it, that would be a bonus.

The sister subordinated SJI 2031 debt on bond market keeps trading around a modest 5.6% yield unaffected by procedings.

https://finra-markets.morningstar.com/BondCenter/BondDetail.jsp?ticker=C969426&symbol=SJI5156685

I try to balance things so I bought a decent amount of KTH at 29.80-4 today. That is a modest but 2028 term dated ute issue that will net a 5.4% YTC at that price.

Thank you for this, I had lost my interest for preferreds for a while but started to look again recently.

Took a look at SJIJ which at first sight seems just shocking. Trying to dig a bit into this now. One thing I’ve noticed is they do have the right to defer the payment of interest for 10 years it seems (first page of the prospectus). I don’t believe this to be the case for the 5.02 2031 similar bond you are looking at. So that’d be one difference possibly explaining the huge apparent arbitrage there. I don’t know if it’s current but I see S&P rates SJIJ BB+ vs BBB- for the 5.02 one, also a slight difference.

Best

Nick, the arbitrage isnt the deferral, that was known at issuance. That is fairly standard language for baby bond subordinated debt. The notch difference is assumed to be deferral feature, but they are both same cap stack. And in a bankruptcy proceeding they would get the same amount…likely nothing being its bottom rung unsecured debt. I dont see any arbitrage at all. I see a trading market knowing already as stated by acquiring company itself, that the issue is going straight to experts market. And that means loss of capital from fleece trading. This is being delisted and deregistered and that is the reason.

…….Our common stock is currently registered under the Exchange Act and trades on the NYSE under the symbol “SJI.” Additionally, our subordinated notes are currently registered under the Exchange Act and trade on the NYSE under the symbol “SJIJ” and our corporate units are also currently registered under the Exchange Act and trade on the NYSE under the symbol “SJIV.” Following the consummation of the Merger, shares of common stock, subordinated notes and corporate units will no longer be traded on the NYSE or any other public market. In addition, the registration of the common stock, subordinated notes and corporate units under the Exchange Act will be terminated, and the Company will no longer be required to file periodic and other reports with the SEC with respect to the common stock or otherwise.

Following termination of registration of the common stock under the Exchange Act, the Company will no longer be required to furnish the information to the Company shareholders and the SEC, and the provisions of the Exchange Act, such as the requirement to file annual and quarterly reports pursuant to Section 13(a) or 15(d) of the Exchange Act, the short-swing trading provisions of Section 16(b) of the Exchange Act and the requirement to furnish a proxy statement in connection with shareholders’ meetings pursuant to Section 14(a) of the Exchange Act, will become inapplicable to the Company. Parent will become the beneficiary of the cost savings associated with the Company no longer being subject to the reporting requirements under the federal securities laws.

What do you mean by “experts market”, do you mean the same as typical corporate bonds like the 5.02 bond? I personally wouldn’t mind, I can trade them fine at interactive brokers. Maybe not as easily but if the opportunity is big enough it’s totally doable.

The arbitrage would be to short the 5.02 bond and buy SJIJ, collect the yield differential risk free until yields converge again.

My only fear here is that the deferral option is actually more critical for a non public company than a public one. So some of the selloff might be justified. Seems way overdone still though, I just don’t see myself going all in on this for that reason.

Nick, the “experts market” is a market that most brokerages have dissallowed retail customers from buying. You can only be a seller into a market where very few buyers exist. No bid or ask pricing is allowed to be quoted. This was originated by SEC last fall and it presently is where stocks go to die. Any entity that does not report financials now falls into this category. I would become fimiliar with this before buying anything potentially being jettisoned there.

The deferal clause will not be the immediate issue, though going private is in part, as that is the direct problem that sends it to the unbuyable experts market. Remember preferred stocks in general have a built in de facto deferal clause in them from issuance.

I see. Thanks for the heads up. In that case I guess I’ll buy 100 shares and hope to learn something.

I’m keeping an eye on SBNYP and SYF-A among others.

If things take the end of 2018 turn, preferreds will keep dropping along equities even as rates stabilize. They should get real cheap then. Or the fed actually moderates its speech a bit today and we get a much needed relief.

Markets pricing fed fund at 3.13% at the end of the year already now! 10 and half 25bps more hikes this year. And the way preferreds are trading lately, things are really just escalating to one of those self fulfilling, panic drops. Crazy times.

Nick, I own it, been buying on way down got more at lower $17s, obviously didnt look today as it was heading back up. I just wanted you to make sure the purchase aligned with your strategy. If it bounces I may sell and look again lower. Otherwise I will hold through the dark side as a modest purchase of an 8% annuity.

Hey Grid, I believe I read here that someone said they were not able to buy KTBA. When this Structured Products CorTS, BellSouth Debentures, 7.00% Certificates was issues 2/23/2007 there was a provision that to be initially issued they had to be a AAA rated security (how the mighty have fallen). Is there any issue with buying this debt? Isn’t it backed by AT&T (or what is left of T)? Thoughts would be greatly appreciated.

It is during our darkest moments that we must focus to see the light, Azure

Hey Azure. Yes the experts market snagged it because although the issue is T debt obligation it is structured inside a trust. The brokerage delisted the trust after Bell South was bought out by T. There is no ownership in terms of reporting the financials to keep it off the experts, even though T’s financials are clearly reported to SEC. T’s debt is inside the trust but they nor Bell South at the time, had anything to do with this. It was basically a synthetic baby bond created by a brokerage.

T’s unsecured debt is BBB, so I suspect this is the rating it has.

Grid, thank you so much for the explanation. I called Vanguard yesterday and their “head corporate bond trader” told me they would not let me or any of their clients buy the T backed bond; that is outrageous. When I told him I was a retired instructional trader and that I am familiar with the expert market, he asked me if I’d like to apply for a job because they need “multiple bond traders that have experience” and “can’t find good candidates”. He still wouldn’t let me buy KTBA 🤬 and that is an insult to all of us. Be well, A

Azure, isnt it great they protect us from ourselves? Wanting plus 7% lower IG debt for income that has paid religiously since issued in late 1990s? No! That is too dangerous for you! But hey, why dont you buy all the “safe” Freddie Mac decade long suspended nearly worthless preferreds and a slug of Wheeler preferreds. The govt says its A OK to buy all you want of them for a happy retirement.

I’m going to call Merrill Edge tomorrow and see if they will “let” this neophyte buy “high risk IG” KTBA. I came across this article today and understand the risk on appetite of what the major retail brokerage firms desperately want their client to buy because of their incredibly high fees. Since the SEC does virtually nothing to protect the average investor they just talk a good game and pat themselves on the booty https://wolfstreet.com/2022/05/04/uber-lost-5-5-billion-on-four-spac-ipo-stocks-grab-didi-aurora-zomato-how-it-ended-up-with-them-and-how-they-imploded/

is it my imagination, but it seems like a lot of REIT’s are getting crushed today.

Anybody know the catalyst?

I would assume that interest rates rising have finally caught up to some of those over priced pigs. REITS are mostly bought for a share of the income yet many were treating them like ?growth? stocks well beyond the amount they actually grow. Or perhaps they thought it would be a hedge against inflation since they own property. Take MAA for example. At a certain stage in the recent past the yield was below 2%. Historically greater then 3% would be much more acceptable for it. When you can buy investment grade preferred or BBs paying 3 times as much right now why hold on to REITs? Everything seemed over priced just a few months ago and the dip buyers ran out of cash I suppose.

There is similarity between eREIT and Preferreds IMHO. eREIT has pro forma dividend yield vs. Preferreds coupon. There are some SA writers who insists retained earnings etc.. To me, SHOW ME the money. These are not BRK/B which Warren Buffett keeps all the “juice” without paying any dividends. Hence, the BUY point and SELL point become very tricky. I usually do not sell unless some God awful collection of small eREITs full of hazard from Rida Morwa, i.e. KBWY. In retrospect, Rida was 2 or 3 years too early. KBWY is doing fine. My best bet is so far IRM, bought 2 years or so before Jussi Askola said BUY. Askola has left Rida long ago and has a West Point early retiree helping him. Earlier, that West Point man seems to have good idea. These days, they just want to sell subscriptions. Some SA writers claim IRM is bound to decline with electronic documents (IRM has also gone into that biz). A few months back, MPW was deemed as best of senior care. Apparently some downgrade by analysts. Sharp draw down. OHI was considered bad, then some claim that they can sustain the high yield, not to follow the bankrupt Mall issues. I have SBRA, bought at ridiculous price following Dane Bowler. Tried a few times buy and quickly selling DEA following article by Brad Thomas. I was lucky that I did not lose money. Had I “stayed”, fastest way to have unrealized loss. SBRA pays very “generous” dividends. Most analysts claim sustainable. WPC is one of my largest holdings from Rida’s days and added more shares. It pays decent pro forma dividends. So far, most of my unrealized gains come from IRM. I kind of like eREIT, they are substantially less headache than having real residential rental property. Commercial real estate leasing is typically substantially more volatile reacting quickly to supply vs. demand. At this time, energy names rock. Then WTI keeps on dropping. I like EVA and have limited EPD in my retirement accounts. I bought a few more shares of EVA and small number of shares of XOM and VDE (EFT) I hesitate because the talking heads of CNBC keep on urging whatever sector or names bring IMMEDIATE “profit”. Yesterday Expedia was King, today, it is DOG! LOL.