Here we go–another week which will be full of ups and downs in equities and interest rates. On Tuesday the consumer price index (CPI) will be released and the forecast is an increase of 8.4% year over year. Also we have at least 5 speeches from FED folks including Lael Brainard on Tuesday.

Last week the S&P500 moved in a range of 4475 to 4593–a relatively tight range, before closing the week near the lows at 4488—down about 1 1/4% on the week.

The 10 year treasury started last week at 2.37% and ended on Friday at 2.71%–near the weekly high at 2.73%. At this moment (6 am central) it is trading at 2.75%. With FED officials speaking this week and the CPI release I suspect this is moving higher this week–but hope the rise is modest.

The FED balance sheet was absolutely flat last week at $8.937 trillion.

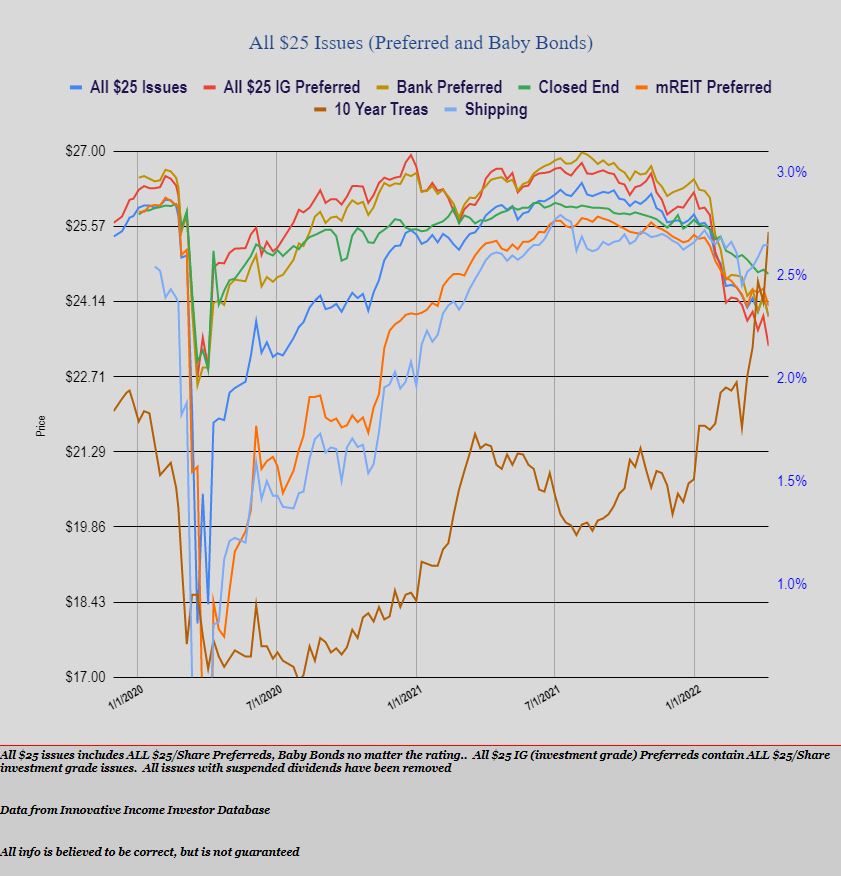

Last week we had quite a give back in $25/share baby bonds and preferred stocks with the average share price down 38 cents. Investment grade issues fell 57 cents, banking issues by 41 cents and mREIT issues fell 33 cents. Shipping issues were the strongest sector with a gain of 2 cents.

Last week we had 1 new income issue announced–although not priced. CEF Rivernorth Opportunity Fund (RIV) announced they will sell a new perpetual preferred. Until this point in time the fund has not priced the issue.

I know I Bonds have kind of gotten beaten to death around here, but I have another question. It’s related to when the new rate kicks in.

I’m looking at the table on TD and it says if I buy after April 1, my rate is fixed until Oct 1. May 1 to Nov 1 and so forth.

My question is: If I buy now (before May1), I lock in 7.12 % (3.56%) and my interest stays the same until Oct 1st. A new rate is declared May 1st, but I won’t start accruing at that rate until Oct 2nd? So, even though new rates are declared in May and November, I’ll always accrue on MY 6 month timeline? I won’t miss out on a rate change, or only get 1 month of a new rate?

So, when I go to redeem, I should be cognizant of when MY cycle ends and not pay attention to the May and November reset dates, lest I may give up my 3 months of a higher rate (unless I hold for 5 years)?

Yup. That’s my understanding.

Your automatic rate reset on an I Bond is every six months from the date of purchase. The I Bond rates change each May 1 and November 1, and your reset rate is whatever I Bond rate is then in effect.

If you buy in April, you will be paid 7.12% for six months, and then the rate will reset. The new I Bond rate effective May 1 has jumped to 9.62% and will be in effect until Nov 1 for new purchases and automatic rate resets during the period May 1 to November 1.

Isn’t it actually from the first day of the month you purchase, not the specific day of purchase? So in a way, it pays you to buy close to the end of any month because you’re credited with that full month’s interest.

Speaking of 8%+ rates, what is the opinion out there about investing in USDC, USDT etc crypto and holding it in an exchanges’ earn account?

As much as this 8%, tax advantaged, safe instrument gets me excited, I keep reminding myself that I am not getting richer here and I am NOT making any money (after inflation) here. I will just be preserving my money. It pays a lot because inflation is in the roof, and high inflation is bad for everybody. It is attractive, because the rest of your money will be loosing , unless you take enormous risks to try to make more than 8%.

So… it’s a bad time for people having money. Most likely we will be poorer when (and if) inflation comes back to normal.

In addition, if all the money you put in i-bonds is only a small % of your capital, then overall it will help very little to reduce our losses due to this crazy inflation.

Having said all this, I have maxed a few years i-bonds among family.

Your comment about it being such a small amount overall is why I did not bother send another payment to the IRS this year in an attempt to get another 5K of ibonds. People here gave solid advice how to do it but when your taxes are sitting in turbotax ready to submit versus jumping through some hoops to get another 5K.. I said.. eh.. fudge it. I hit submit.

DD, It definitely is overall an “is what is thing” in terms of ones portfolio. May not be worth the distraction of another account to monitor. It is for me, but Im not wealthy. Even at 8% my 30k of Ibonds is going to pay me less than half my pension cola alone is, but I am going to keep stacking those nickels!

Inflation is an odd and most individual creature. My bills have certainly not went up 8%. Its only really going up in the areas that are a relative small amount of my monthly budget. So for me, 8% Ibonds makes me real relative money.

Well. Eight days after my e-file was accepted, the cash portion of my tax refund hit my bank account.

It will be interesting to see how long it takes my paper I-bond to get here.

I filed return March 20th via TurboTax electronic filing, received refund in checking acct April 6th and received 5k ibond in my usps mail box today. 🙂

I agree. Will Ibonds make you rich, no. Will they move the needle for your retirement income – no. Are they a hell of a lot better alternative than a money market account paying .50% or a one year CD paying 1% – absolutely

So I put $10K in last Oct, another $10K this January. Had my wife do the same thing. This was money we had in money market accounts with no investing plans for nor short term need for.

At the same time, I decided it was not worth the hassle of overpaying my income taxes to get a $5K paper I-Bond.

And as of now, I haven’t been motivated enough to do the gifting option between my wife and I for 2023. I guess if the 1 year clock starts ticking on it as soon as you put it in your giftbox, it may make some sense. But the size isn’t enough to make a big difference so I have held off on that

Just all depends on one’s individual situation

FWIW, Maverick, the clock does start ticking the minute you buy in the gift box. Consider this viewpoint. If it was worth your time to set up your account to buy 20k of Ibonds, its worth your time to gift each other 10k more. This would count as next years contributions, which you could withdraw in 12 months. Its simply front loading next years purchase and snagging the 7.12% and 8% ish now.

It only takes a few minutes. And this is coming from a lazy guy who didnt mess with the paper Ibonds this time. But I easily found the energy to do the gift exchange….because it was easier, ha.

Grid – thanks for the info. The clock starting ticking the minute you buy in the gift box is beneficial. I may have to convince my wife tonight to do this

Grid – What are the logistics of the giftbox? Does it ask you for the person receiving the gifts Treasury Direct account number? Do you have to specify a date when it will be delivered (ie Jan 2023).

Just curious how and when the gift gets from my TD account to my wife’s TD account and vice versa. Thanks

Yes, it will ask you name and their account number. Its very straight forward. If you want to do the beneficiary thing, you need to do it at that time. I didnt but should have, whatever, I aint dying by next Jan!

You do not designate a time to gift it yet (at least I havent yet) If that person has not bought this year, you could send the gift in 5 days after the customary funds clearing process. If yields are still high come January, I will just hold the gifts, and buy 10k more and gift the following year.

Here is the basic Treasury Direct video to watch. Very simple and 97 seconds long…You can survive it, I promise! 🙂

https://www.youtube.com/watch?v=Z7wP44VaoMg

Grid – thanks much. One last question since you mentioned beneficiary. which I guess I never paid attention to on Treasury Direct. I realized I never even set that up for the bonds I purchased for myself. I found how to edit the registration but just want to be sure I have this right. Seems there are 3 options

Sole Owner – which would just be myself

Primary Owner – where you add a second I assume joint owner

Beneficiary – self explanatory

So for I-bonds I own myself, to have a beneficiary I would do a new registration selecting the third option , put me as the owner and say my wife as beneficiary – correct?

Now for a gift to do so with a beneficiary – I assume I still select the third option – Beneficiary. And the first name is the gift recipient (say my wife) and the second name is the beneficiary (could that be me even though I am the gift giver? or does it need to be a third person – say my daughter)

Thanks

Mav

Maverick, to be honest I was going to backtrack and put in my beneficiary stuff, somehow managed to lock my account up before I got there. Spent 40 min waiting for a TD rep to reach to get me unlocked. By then I was pissed and just never have been back in the account since.

But here are excellent directions from guy who knows a lot about it and also did the gift bond article to get me thinking.

https://thefinancebuff.com/i-bonds-add-joint-owner-change-beneficiary.html

Grid – thanks. Took a look at that link and some of his other links. Excellent stuff. Answered all my questions and then some.

Going to take advantage of the giftbox feature for my wife and I in the next few days as soon as my transferring of some money to do so is complete

Thanks

Comparing profit to Inflation s a sign of the times. But the real measure of an investment is comparing it to what you could have made if you invested in something else instead, or nothing. Often you can come out ahead of inflation sometimes you can’t, the game is always to maximize profits and minimize losses.

…. On Tuesday the consumer price index (CPI) will be released and the forecast is an increase of 8.4% year over year…. Will the last person in line who wants to buy any Ibonds and still hasnt, please turn off the light when you leave the room?

Over 7% return guaranteed with zero risk and tax advantaged, I wish I could buy more.

If I understand correctly, you can use the interest income on these iBonds towards educational expense like kids college tuition and pay ZERO federal or state tax.

Yep…

Rules for Using Savings Bonds for College

The interest earned on series EE and Series I bonds can be used tax-free for college if the following conditions are met:

The funds are used for qualified educational expenses for parent or dependent child. These include tuition and fees for courses that count toward a degree or certificate program. Books and room and board are not qualified expenses.

The expense occurs in the same tax year in which the bonds are redeemed.

Both the principal and the interest from the bonds are used.

The qualified education expenses have not already been covered by financial aid, scholarships, 529 accounts, Education Savings Accounts (ESAs), or other tax breaks.

Your filing status is not married filing separately.

Don’t forget your income can’t be too high during the year you cash the savings bonds and pay for the college expenses.

https://www.irs.gov/publications/p970#en_US_2021_publink100062398

“ You may be able to cash in qualified U.S. savings bonds without having to include in your income some or all of the interest earned on the bonds if you meet the following conditions.

1. You pay qualified education expenses for yourself, your spouse, or a dependent.

2. Your MAGI is less than $98,200 ($154,800 if married filing jointly).”

This has probably been covered, but it’s hard to search the threads…. And I don’t see on TD where they discuss how the fixed rate is calculated.

What determines the fixed rate? (currently 0%)

And then, the rest of my understanding…. Basically, regardless of when you buy the bond, you get the current rate. And then every 6 months the rate changes. As inflation gets tamed, or we go into a recession, the rate will fall. I guess when the rate gets to a low enough point, that’s when I should look at cashing in?

So, for everyone buying these and loading their gift boxes to the hilt, what is the plan for when inflation is back to historical norms? Dump them and lose 3 months interest? Or just keep holding and collect the 2 – 3%?

I’m having a hard time grasping the opportunity in these beyond a relatively short timeline (anything beyond current rampant inflation)

Yes. Whatever makes sense with the numbers at the time. I’ll probably hold to the 5 year mark, But if the rates are low and there are good opportunities elsewhere I may cash out, Low rate means low penalty. Also your tax situation is a factor since you’re taxed in the year you cash out.

Mark – Unquestionably it is the current amazing rate that you can get on these that got me into them, however, name another riskless investment with absolutely no downside possibility that you can set and forget and know that when the day comes that you cash out, your $1 invested today will be worth exactly what a USD is worth in the year you cash out? To me this is not so much a money making opportunity as a part of an emergency fund stash that just about everyone should have….. And if your emergency stash is large enough, if interest rates/inflation rates return to a more Fed targeted 2% level, then you will have the flexibility to let your IBonds ride for 3 months and then cash out after the 3 month penalty you incur (if cashing out in the first 5 years) is at a lower rate as it comes down… Also don’t forget that compounding by starting now at a high rate gives you that much more of an advantage going forward even if you’re assuming you’ll eventually cash out on a market rate decision (not an emergency use decision).

Mark, TD does not disclose it, because there is none. Obviously there are some factors they look at, but when the yield is above the other bonds in such a manner its a given its going to be zero.

… I’m having a hard time grasping the opportunity in these beyond a relatively short timeline (anything beyond current rampant inflation)…. That is precisely the intent for what my purchase is. Instead of reaching for yield, or getting gobsmacked on a perpetual in decline, this money will grow faster than any safe income issue and for me its 30k not depreciating if it was in the mattress.

You have to compare it to the context of its purpose. And that could vary person to person. Im in camp it will sit there until something of better relative value comes along.

Some people have gifted and bought out to 2025, knowing that if following cycle after next is 6.5%, then 0% until 2025 it still nets out to 3.94% return. What US govt bond pays 3.94% for 33 months? Some couples have bought cheap online trusts and have pumped 100k quickly into these. Some people will do a lot for income of high yield that is safe as it comes.

Thanks all. That helps a lot with my understanding of what other’s are thinking. I’m basically in agreement with all of the above points. I just haven’t been able to buy any yet. I just filed an extension and overpaid my estimated taxes, so I’ll get a paper bond in some amount, but if we are in a recession by the end of the year, then I won’t be looking at much of a return. But as 2WR pointed out, it may be a nice emergency stash if ever needed.

On another note, with the IRS being so far behind, what is the supposed time line for actually receiving the bond? Will my rate be fixed when I file my taxes and request the refund as an Ibond? Or will my rate be determined when they finally get around to issuing it?

Thanks again all, and thanks to Tim for the best address on the internet!!!

Mark I received my ibond today in mail. Filed return electronically 22 days ago.

Marc, I am another short term buyer. So that is the camp I belong in. I imagine in a couple of years these will be paying close to zero again. As for the 3 month penalty I just wait until the 6 month rate is pathetic and allow the 3 months to take place during that. Cash out and find something else. It just protects the original investment and allows some gains in a safe manner during these zany times. I did not go wild like others though. We are reaching the point the open market has some pretty good opportunities which may very well get better as the year goes on. I want some cash for that.

Just commit yourself to hold the I bonds for an additional 3 months at whatever the lower rate is at the time so the penalty will then be lower.Keep an eye out on future resets and decide.

I don’t follow ibonds closely but have been looking at it recently. Question -might the base rate increase above the current zero rate on May 1 when the govt resets ibonds for the next 6 months meaning that anyone that still hasn’t bought their 10k limit for 2022 should wait until May 1 to see what new ibond rate is (plus gets the March CPI rate being released tomorrow)?

Treasury if I am not mistaken doesnt disclose the fixed part until its too late. If you wait until May 1, you get the next cycle, and miss completely out on the juicy 7.12%. Personally if I wasnt buying the 7.12% now, I certainly wouldnt be waiting and buying the 8% as you have really lowered your total returns going forward missing out.

As far as a fixed component, I would suggest the fixed component has a less than zero percent chance of being above 0% next cycle.

Longhorn – Keep in mind that although the fed determined rate changes in May, what you get and when is determined based on the month you purchase…So despite buying now at the end of a 3.56% annualized rate (with it essentially guaranteed to be higher for the next 6 month period) you personally will get 3.56% for 6 months AND then whatever the new May rate becomes for another 6 months… So buying now (if possible under the wire) locks in what should be over 7.50% return for 12 months… Buy in May and you get the new rate for 6 months and you’re at risk of whatever the next rate change happens to be another 6 months out…. It’s like being able to buy with 20/20 hindsight on what’s happened inflation wise in the past 5 months.

Ever since ibonds became a hot topic the wisest advice has always been buy as soon as possible. Don’t wait. Waiting has resulted in missing out.