Well last week was another exciting week–although not in a good sort of way. I suspect we will once again have an up and down week in equities as folks continue to grapple with hot inflation and the correspondingly higher interest rates. On top of this the Russia/Ukraine tension just adds to the negative tenor of the markets.

The S&P500 fell by 1.8% last week, while the DJIA fell by just 1%. The S&P500 is now 8.3% off of the 52 week (and record) high. NASDAQ is off about 15% from the 52 week high.

The 10 year treasury, as everyone knows by now, spiked up to 1.98%, before settling Friday at 1.955% as consumer inflation came in hot with the month to month increase in prices coming in at a +.6% showing that pressure to the upside remains hot. We will see producer price numbers tomorrow (Tuesday) for another read of potential future inflation—a plus .5% is expected.

The Fed balance sheet assets moved higher by $5 billion last week. In the last 3 weeks the balance sheet rate of increase has slowed substantially as the last 3 weeks has shown a total increase of just $11 billion.

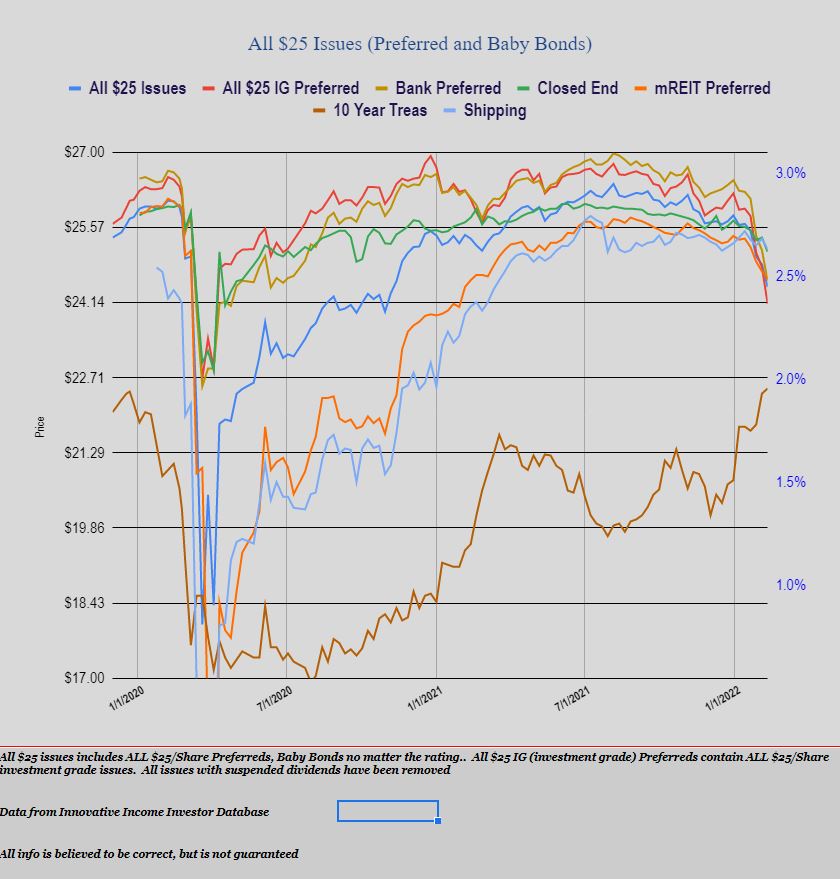

The average $25/share preferred stock and baby bond took a shellacking last week with a loss of 43 cents/share. Investment grade issues were hammered down by almost 3% with a 70 cent/share loss. mREIT preferreds fell by 14 cents and shipping issues by 20 cents. Bank preferreds were off 58 cents/share with CEF preferreds off 27 cents. This continues to confirm that the most high quality issues fall the most during times of increasing interest rates.

The chart below gets uglier by the week.

Last week we had no new income issues priced–no surprise in this time of turmoil.

Regarding the debate about LIBOR vs SOFR, can’t we assume that institutional holders will sue any issuer that tries to replace a 3-month rate with an overnight rate? If the info on the difference between the two is correct (i.e., large decrease in the rate), it is hard for me to believe that institutional holders are going to accept this without a fight.

Many here are upset that their income portfolio’s dollar value has dropped. In my opinion, the reduction in value is not particularly troublesome, in that the prices are lower for the “right” reason, mostly due to interest rates rising in general, as opposed to the value going down for the “wrong” reason : credit spreads widening. With many income investors going out on the risk curve to try to generate a reasonable cash flow and take advantage of the Powell put, an implied increase in the future default rate would be more concerning. As you continue to initiate/add to positions the value of your holdings may well go further below its all time high, but your investment income will keep setting fresh “all time highs”. When the lower quality issues have the biggest price drops, which is the opposite of Tim’s astute assessment of the current situation, concern may well be warranted

Tim. In your opinion ,is this the bottom,,time to sell ,to buy all these deals…

Georges..

LIBOR3 is really jumping. Doubled in a month. https://www.global-rates.com/en/interest-rates/libor/american-dollar/usd-libor-interest-rate-3-months.aspx

and SOFR stays at 0.05%..and this is what is supposed to replace LIBOR??!! it is manipulated by the FED.. LIBOR for all its ‘faults’ is a somewhat accurate feel for what is going on in credit markets.. SOFR is not!

Bea, you’re comparing an overnight rate to a 3-month rate…maybe you’re not quite qualified to criticize the Fed, yet.

What being compared is the 3 month rate to what is written in for a number of prospectuses as the replacement for 3 month LIBOR if it no longer exists.

No, the tenor of the replacement needs to match the original. You think investors who are getting a payment tied to 3-month, or even 12-month Libor, or just going to accept an overnight rate as a replacement? Not a chance.

Tell that to the authors of the prospectuses that have the language already written in.

Show me such a prospectus, please.

I read enough prospectuses to have made a mental note to self. “Self, pay attention and red flag any interest you have when you see SOFR as the substitute for 3mo LIBOR if it ceases to exist.” Can I name one in particular now? No…I read and move on… Am I going to go look for one now to prove the point? That too is a no……. Don’t forget that there are prospectuses in existence that essentially say if LIBOR stops, then the F/F reverts to the last level before it disappears, so anything’s possible and should be paid attention case by case.

2WR,

So here’s the point: SOFR is relatively new. If overnight SOFR is built into the contract to replace 3-month LIBOR at some point (which I haven’t seen, but there are lots of prospectuses I haven’t seen), then that is not actually a problem because both parties to the transaction agreed to it.

Bea’s implication above is that, for older contracts that are using 3-month Libor (including many outstanding preferreds and long-term notes), the rate will be replaced with overnight SOFR. There are trillions of dollars of contracts tied to 3-month Libor – is it sensible to think that they will all be changed in a way that guarantees a lower payment solely because a shorter tenor was chosen? Isn’t it obvious that this will NOT occur?

Yes, there may be a small number of issues out there that say if the reference rate disappears, they will just use the final rate forever. But the vast majority have language that specifies the replacement rate is to get a rate as close as possible to the original reference rate, which includes the tenor.

I don’t know how they will resolve all of these and it’s a colossal mess, but Bea claiming that the Fed is manipulating overnight SOFR in order to eventually reduce someone’s 3-month Libor linked income…well, that’s just a serious misunderstanding of the situation.

There is one message I’ve trumpeted here a few times – know what you own. Actually read the prospectus and try to understand the technical issues like this – most don’t bother. If anyone owns Libor-linked issues and still hasn’t done this to figure out what might happen, today is a good day to start.

https://www.cmegroup.com/market-data/cme-group-benchmark-administration/term-sofr.html

This page has SOFR terms out to 1-year. 3-month SOFR is listed at 0.37486.

The most recent 3-month Libor is 0.37. Looks pretty close when you match the tenor, doesn’t it?

No doubt that the transition will not be perfect, but the industry standard will be to attempt to match the tenor of the replacement rate with the original.

I think we’re actually tooting the same trumpet, KC. Know what you own…. My problem these days as I age is remember what I own…. Quite honestly I was skipping over the comment about Fed manipulation entirely I’m not a conspiratist……… Also agree there have got to be many an issue, particularly the older F/F issues that might be silent in their documents about what could happen if/when LIBOR goes away….Unquestionably there’s going to be a few very messy situations to be cleaned up. I think I heard this somewhere and I fully agree with it (don’t know where I heard it ;)) : “If anyone owns Libor-linked issues and still hasn’t done this to figure out what might happen, today is a good day to start.”

FWIW, I see quite a few that reference in the end this way…After the usual if we cant find 4 banks, 3 banks, etc….

If fewer than three New York City banks selected by us are quoting rates in the manner described above, the Three-Month LIBOR Rate for the applicable interest period will be the same as for the immediately preceding interest period or, if the immediately preceding interest period was within the Fixed Rate Period, the same as for the most recent quarter for which the Three-Month LIBOR Rate can be determined.

……So it is, you need to know what you own. That was for NSS by the way.

….But its not all that cut and dried….Look what Co-Bank in their recent SEC filing they dont know what will happen including getting sued over it. So, “knowing what you bought” isnt so simple if the issuing entity doesnt have a definite solution either… And this is in reference to their own preferred stock they issued also.

We have exposure to various LIBOR-indexed financial instruments that mature after 2021. This exposure includes loans that we make to our customers, investment securities that we purchase, Systemwide Debt Securities that are issued by the Federal Farm Credit Banks Funding Corporation (Funding Corporation) on the Bank’s behalf, PREFERRED STOCK that we issue and our derivative transactions. Alternative reference rates that replace LIBOR may not yield the same or similar economic results over the terms of the financial instruments, which could adversely affect the value of, and return on, instruments held by us. The transition from LIBOR could result in us paying higher interest rates on our current LIBOR-indexed Systemwide Debt Securities, adversely affect the yield on, and fair value of, the instruments we hold that reference LIBOR, and increase the costs of, or affect our ability to effectively use, derivative instruments to manage interest rate risk. In addition, to the extent that we cannot successfully transition our LIBOR-indexed financial instruments to an alternative rate-based index that is endorsed or supported by regulators and generally accepted by the market as a replacement to LIBOR, there could be other ramifications including those that may arise as a result of the need to redeem or terminate such instruments. Disputes and litigation with counterparties, investors and borrowers relating to the transition are also possible. Due to the uncertainty regarding the transition from LIBOR-indexed financial instruments, including when it will happen, the manner in which an alternative reference rate will apply, and the mechanisms for transitioning our LIBOR-indexed instruments to instruments with an alternative rate, we cannot yet reasonably estimate the expected financial impact of the LIBOR transition.

FWIW, I have read Bea for quite a while now and respect Bea’s thoughts and posts. Keep ‘em coming Bea!

Grid, that’s all CYA language. They say rates may go up, because that’s their risk. Read the prospectus and it says rates may go down, because that’s our risk. Could go either way but I would guess the net impact will be relatively small.

AGNCP’s prospectus.. if read carefully mentions SOFR and LIBOR. If the right conditions take place the SOFR could become the LIBOR replacement. It would not surprise me and how I read it in the past that is what I think they are warning about. It could affect the price of the shares.

https://www.quantumonline.com/search.cfm?tickersymbol=AGNCP&sopt=symbol

https://www.sec.gov/Archives/edgar/data/1423689/000142368920000008/seriesfprosupp.htm

Anyway.. I have read variations of this. They are just not easy to dig up because you have to read a couple of parts of the prospectus to get the gist of it.

From AGNCP prospectus:

“Notwithstanding the foregoing, if we determine on the relevant Dividend Determination Date that LIBOR has been discontinued, then we will appoint a Calculation Agent and the Calculation Agent will consult with an investment bank of national standing to determine whether there is an industry accepted substitute or successor base rate to Three-Month LIBOR Rate. If, after such consultation, the Calculation Agent determines that there is an industry accepted substitute or successor base rate, the Calculation Agent shall use such substitute or successor base rate. In such case, the Calculation Agent in its sole discretion may (without implying a corresponding obligation to do so) also implement changes to the business day convention, the definition of business day, the Dividend Determination Date and any method for obtaining the substitute or successor base rate if such rate is unavailable on the relevant Business Day, in a manner that is consistent with industry accepted practices for such substitute or successor base rate. Unless the Calculation Agent determines that there is an industry accepted substitute or successor base rate as so provided above, the Calculation Agent will, in consultation with us, follow the steps specified in the second bullet point in the immediately preceding paragraph in order to determine Three-Month LIBOR Rate for the applicable Dividend Period.”

Again, the industry accepted substitute for 3-month Libor would be 3-month SOFR, not overnight SOFR. This appears to be the cause of confusion when it just says “SOFR”.

Oh. I did not think we were still debating the overnight rate. That is wrong from the get go. It has to be a 3 month SOFR rate. I think we all agree with that immediately.

Added thought I forgot to mention….Hopefully as CoBank alluded to maybe companies will do the path of least resistance and redeem the issues and start fresh with a new issuance. That would eliminate some chaos if things dont go right in transition.

That is pretty apparent, the point is nothing is in concrete. Your opinion is certainly as good or logical as the next, but it isnt what is in their SEC filing so one needs to be aware of that….This similar type subject was brought up at a Citi CC a while back when some of their issues could have been staring down the road of a possible negative Libor float. Management said they were aware of it, respect their investors and basically said they would try to do the right thing. They never were specific with the answer and it looks like that problem is avoided anyways; but they were willing to find an equitable solution…. Hopefully that is the end result for any issues that stumble into problems.

Grid, 2WR.. it’s always something here, I don’t know why you waste your time.. I won’t be wasting mine anymore for sure..my last few posts convinced me of that. Thanx for kind words.. retiring at 55, a degree in finance and 32 years in financial work plus 47 years of investing I guess do mean something to some .. I am only trying to help and add meaning to a conversation as are you my friends..

3mo SOFR is 0.05%..if you want to apply the ‘fallback’ adjustment to it, which did not exist in any prospectus’ as you know and have pointed out (and I would venture NO ONE KNOWS MORE than Grid about pfds, bb bonds et al)..

you can maybe get to 0.31 today w 3m LIBOR at 0.45.. so even in that case–which I would gather would still generate massive lawsuits by ins co’s and/or pension funds that hold most of these instruments– you lose out. https://www.sofrrate.com/ If they don’t like the ‘calculation’ agent -which adds more confusion- more wrangling ensues.

LIBOR adjusted pfds/bb bonds can be traded until d-day if you like..but after that you are at the mercy of the issuer who will do what is the best -and lowest cost- way to handle payouts. And thus as a result, I fully believe hundreds of lawsuits will ensue and at the very least, your holdings will be penalized in the market by uncertainty- the bane of the markets. Of course it won’t ‘hit the fan’ until around d-day when it catches a lot of attention..we see that happening w call dates here..etfs/cefs/individual investors hold over par issues close to call dates and get burned all the time..

Personally, I feel higher rates are coming and here to stay and will be treading very lightly and only into issues fixed or floating at 5yr treasury rates OR with a very high reset if they use Libor in the prospectus.

oh- and Bye

Bea, damn, that is a nice pedigree! No wonder I like all your posts, you back the knowledge with experience behind it. Not a “I stayed at a Holiday Inn” person as my experience is.

Remember the silent majority thing as most dont want to engage in these matters and many people read and learn from your insights without ever posting. Please reconsider…..

Heck you and I have had divergent viewpoints at times… And I think that is great as groupthink is the worst type of thought process. However never any rancor or ridicule was expressed between us. And I certainly respect your civility.

I have mellowed a lot since retirement, but you made me reflect and laugh. When I worked and was an administrator in charge, I was an old school believer in “Bully the Bully”. An old boss of mine when I was near the end of my career wanted me to move to the city and take a job under him that would have a nice salary bump….. I told him, are you crazy, the things I get away with saying and doing here, would get me fired in a month up there……

Bea – i second Gridbird’s comments. I certainly understand your frustration with a few folks. Alas, you have them in every crowd. My background is very similar to yours. Retiring at 57, degree in finance , 35 years in financial work and 40 years of investing so I know exactly where you are coming from. My suggestion is rather than walking away, just step back, become part of that silent majority Grid mentioned but participate here and there where you feel your expertise can help someone. That is what I have done. I have found it eliminates a lot of frustration from dealing with the usual suspects while still helping out those who can learn and benefit from your wisdom. Something to consider.

Put me in the ME TOO pile along with Grid and Mav, Bea… Please reconsider.

2WR.. yes you know..and will benefit thusly! Bea

Dude, sorry, but you are still wrong and 47 years of experience can’t change that. You just said that 3-month SOFR is 0.05%, but it isn’t and you are giving bad information to people who are becoming unnecessarily confused about the Libor transition. The 3-month average of overnight SOFR is 0.05% – this is not the same as 3-month SOFR! That’s like saying the 10-year treasury yield is the average of the 1-day T-bill yield over the past 10 years.

C’mon, people, if someone is wrong and it’s going to potentially lead others to making bad investment decisions, it is to the benefit of everyone for the info to be corrected.

KC – Isn’t this really an argument without a distinction right now???? BY definition, SOFR stands for “Secured OVERNIGHT Financing Rate” – https://www.newyorkfed.org/markets/reference-rates/sofr. Over the past 3 months, it has averaged .05%, has it not? Therefore, isn’t it impossible for there to be an actual 3 month SOFR rate if SOFR is an OVERNIGHT rate???? I am far from an expert on 3 month LIBOR vs a definition of SOFR that might reference a 3 month average for it, but it seems that any comparison of SOFR, be it a 3 month average of overnight rates or what’s probably a non-existent by definition actual 3mo SOFR itself vs 3 month LIBOR, (with 3 month LIBOR being a rate major global banks charge other banks for short-term 3 MONTH LOANS) is bound to make for a substantially lower rate and poor substitute for 3 month LIBOR…. Unquestionably, I could be wrong but it makes sense to me. And in any case, right now in this environment, SOFR is .05% and the 3 month average of SOFR is .05%, isn’t it? That’s a big difference when 3 month LIBOR is .37% and rising….

Wow, lots of comments flying. In the end, the NY Fed and Treasury publish a daily, 30, 90, and 180 SOFR rates. The 30, 90, and 180 are averages. You do have groups like CME that have gone to ARCC and have had their reference rates so called approved, but that is not universal. Just because you link to CME doesnt mean that is the universal rate. Your investment would have to have fallback language that would reference their rates that they publish.

Yes there is a gap between both SOFR and Libor, but remember the guidance that ARCC has recommended is to pick the daily rate, or an average and couple that with some type of spread adjustment. As you can see, many investment firms have been working on this for awhile and it is taking forever. Each investment needs people (finance and law) to look at the fallback language and see if there is a “strong” enough language to understand what happens when libor goes away. They need to address it by amending or closing it out and re-issuing. There is a lot more complexity to this and it is taking awhile and many involved keep kicking the can down the road. Libor will eventually die. You need to look at what you own (mortgages, loans, investments, etc) and see if libor impacts them and do your own diligence.

WTREP, Libor adjustments…. Sometimes looking at what you own doesnt always help. I have looked at this before and forgot so I looked again. It didnt help. WTREP has no backup provisions stated concerning Libor being unavailable, other than 1% would be the minimum rate.

This isnt surprising I guess, since it never had a prospectus, being part of the founding capital at companies birth. Only has a certificate of designation.

https://www.sec.gov/Archives/edgar/data/1601669/000162828019000643/c88072_ex4-1.htm

So Im assuming at worst if Libor goes away the 6.68% plus 1% will be maintained as the minimum floor.

Very interesting history here. It was original capital, then it went public trading 5 years later, and days after it went trading, over 75% of the float was immediately redeemed which coincided within a few months of first call date. It still had a $50 million plus float, but never really traded as such. Being the way this company was and is structured, I wonder if company redeemed in 2019 the ones that wanted out, and left outstanding the ones that didnt, but registered the issue to trade if they wanted to at a later date. As they redeemed a very odd amount of shares that made an odd fractional percent redemption, also. And also, there just wasnt a real relative flurry of trading activity in this issue even at the end before going private.

And the way the company is constructed the originals could just want to continue to hold. But yet they stated they would have financing secured at closing to redeem these. And it didnt happen… We are heading quickly towards our 3rd exD next month post going private and no redemption notice yet. Its not like they haven’t had the time to redeem a puny $50 million left issue. It would be interesting to find out why, but it wont ever be revealed. But, since I own a lot, it sure helps as a ballast as it isnt going to drop in price, lol.

Well Grid, as long as WTREP keeps paying. i own 6,000 shares. They have until end of June 2023 to actively do something when the can was kicked down the road. If they don’t do anything by July 2023, then whatever the last published rate was, it will be frozen at that rate. It would get real interesting if rates are still being raised 1 and 1/2 years from now. I am just enjoying the low volatility.

I agree, Mr. C. Since I have no need or desire to sell like you, the fact the price cant drop makes it just fine with me. Though stash of it isnt as big. You got about 4k more than me, so your divi check is a lot meatier than mine is! Who knows, it is possible Libor could claw its way to 1.50% by then and that would put us over 8% if it stays outstanding.

2WR, yes you are wrong and it definitely does matter, but members of the board have spoken out strongly that they would rather have wrong information stay on this site because no one should have their feathers ruffled just because they are spreading misinformation. Good luck.

I think part of the point is that it’s not really the III way to try to convince someone that their thesis is wrong by ruffling their feathers.

3 month SOFR is based on the SOFR futures curve, which is based on where the market believes SOFR will be 3 month from now. I doubt $trillions of floating rate securities will be priced off a futures curve. I think we will be stuck with an overnight rate replacing a 3 month rate. This is going to good for borrowers at the expense of investors. This is just my opinion.

Thanks, kapil…. That being said, what presently is 3 month SOFR right now and where is it published???? I probably didn’t search hard enough, but I didn’t see the actual rate anywhere.

2WR, Can I go so far to suggest it wasnt part of the point, it is the entire point.

You and I have corrected and/or disagreed with each other often and I dont feel either of us have ruffled the others feathers would you? But more importantly we never wrote these in a manner as that was our goal either, I would suggest.

https://www.cmegroup.com/markets/interest-rates/stirs/three-month-sofr.quotes.html

https://www.sofrrate.com/

Grid – absolutely I would agree on all parts…. fortunately for me, though, I suffer from male patterned featherlessness so in some instances I can handle it, but for the most part, purposefully aimed feather ruffling is more suited for SA than here imho.

Thanks for the links, kapil and danzeb. So right now, the substitute for 3 month LIBOR is 3 month SOFR futures rate that is either .26161% or .31095% dependent upon if what’s supposed to be used is the fallback spread or the fallback rate??? I would guess “rate” is supposed to be the number… If that’s accurate as to the substitute when SOFR is mentioned as the alternative to LIBOR in a prospectus, then I guess we’re at least getting close to not hurting too badly if/when it comes into play.

Bea,

I too am concerned about the retirement of LIBOR. Who knows what the issuers of PF/Notes that are tied to LIBOR are going to offer as a replacement. I like the idea that NRZ-D used in their issue, “…U.S. five-year treasury rate…plus 6.223%” Maybe other issuers will use something like that instead of some sort of low ball SOFR rate.

well at least you get it!! best to you.

Hmmm. Citigroup Preferred series K doesn’t leave many options.

https://www.sec.gov/Archives/edgar/data/831001/000119312513411732/d617242d424b2.htm

Justin I dont remember any specific issue sited, I just remember a caller asked management what they do on any negative Libor issue, and they gave a generalized repsonse. So I dont know if there was a specific issue the person was angling about or not. Citi has several Libor based debts. They even presently have one thats 3 m Sterling Libor plus 88 bps that was issued 15 years ago.

Every time an investment grade issue gets hammered, a corporate treasurer gets their wings…

I believe why the high quality issues fall the most stems from the fact that they tend to have lower coupons and long dated/no maturity dates (so the issuer can lock in those low rates), both of which add to their convexity. When rates were low, many traded around 0-1% YTC for a glimpse of the other side of that coin. Now an opportunity is opening up for discount pricing we haven’t seen since late 2018

While this rebalancing is very painful (and a bit overdone) at least there are bargains starting to appear. 3 months ago there was nothing to buy (generally speaking).

libero:

You are correct. I remember when Grid mentioned that 4.2% CMS+C would be real interesting at $21/share….but now that it is there – is anyone on this site buying?

My guess is most likely not. Human psychology really “perks up” when markets/prices are plummeting.

I am buying CMS+C – but only 10 shares at a time! At this rate, my 35% cash won’t get done being re-invested until the Rapture.

BTW – another $200 million in outflows in PFF last week. Now down 9%+ for 2022. None of this relentless selling will stop until these outflows cease.

Rob,

I too hold about %25 in cash but i have started buying (maybe a bit soon). I have to believe issues like RC-E at $22.88 with 7.08% div surely must be near bottom.

I sold off all my 4-5% preferred’ s a couple of months back before the drop but i should of cut deeper. I got caught with the 5-6% payers. AGM-D 5.7% has dropped from >$27 to $24.89. I also lost a lot with BAC-L and WFC-L (although i did unload a third of them a few weeks ago). My AZ MUNI NAZ shed everything it had made in the last year.

Even though my portfolio is only down a couple of percent it still hurts lol.

Ya, Rob, my emotions are holding me back here. Many things have fell so fast, I still dont know if the trap door has been opened even yet. Plus you have ALP-Q right down to par now and its 5.0% A3. Plus I bought so much SR-A I dont need as much lower stuff. Im still watching!

Gridbird,

I have been watching SR-A, if it reaches par i will load up but not sure if it will go that low. It may as it is a sub 6% divi.

Libero, Its hard to tell. I know situations change but when it was $28 I was would have thought it was a gift at this price. But a fund could dump it and drive it to an even better price. My cost basis now is $25.65, but I traded them hard and gained well over a buck in past month flipping several times before recent carnage. So I have the mental math gymnastics contorted enough in my head to feel good with where I am at with this. I would consider buying more…but dont need anymore that is for sure. At this point I am under no illusions its nothing more than a safe income play whose price could deteriorate even more.

I am just scared these are still sucker prices. How high does the Fed need to raise interest rates to tame 8% inflation? Probably a lot more than is priced in now. If that is the case, then what would be the point of getting in now vs. later?`

We could have a long, long ways to fall here yet. And my portfolio (as well as my psyche) is not nimble enough to jump in and out at the drop of a hat.

I kept asking myself how does raising interest rates actually tame inflation? Interest rates is the cost of money, so increasing the rates makes money more expensive. Isn’t that the greatest inflation of all, considering many things has to be paid for with borrowed money, such as homes, autos, and many other items. The US currently is at a high level of debt. I’m no economist, but it seems to me raising rates is just a measure to destroy the economy. Inflation is two much money chasing to few product. Seems this is all the result of the free money from Washington, and now comes the time to pay for that money. My belief is this inflation really is a short term problem and if the Fed gets carried away with rate increases, we will certainly see a recession. Sorry, just had to get out there to see if I’m crazy or what.