The S&P500 moved lower last week by about 1.5%. Of course the movement was an up and down affair with no conviction in either direction. Futures tonight are up 1/2%, but we will have to see if that holds.

The 10 year treasury tumbled last week closing at 1.34% down 14 basis points. This week we are going to have the Consumer Price Index released on Friday–for what it is worth the forecast is a hot .9% increase.

The Federal Reserve balance sheet fell by $31 billion last week. We should see the trajectory of the balance sheet flatten just a bit month by month as tapering takes hold.

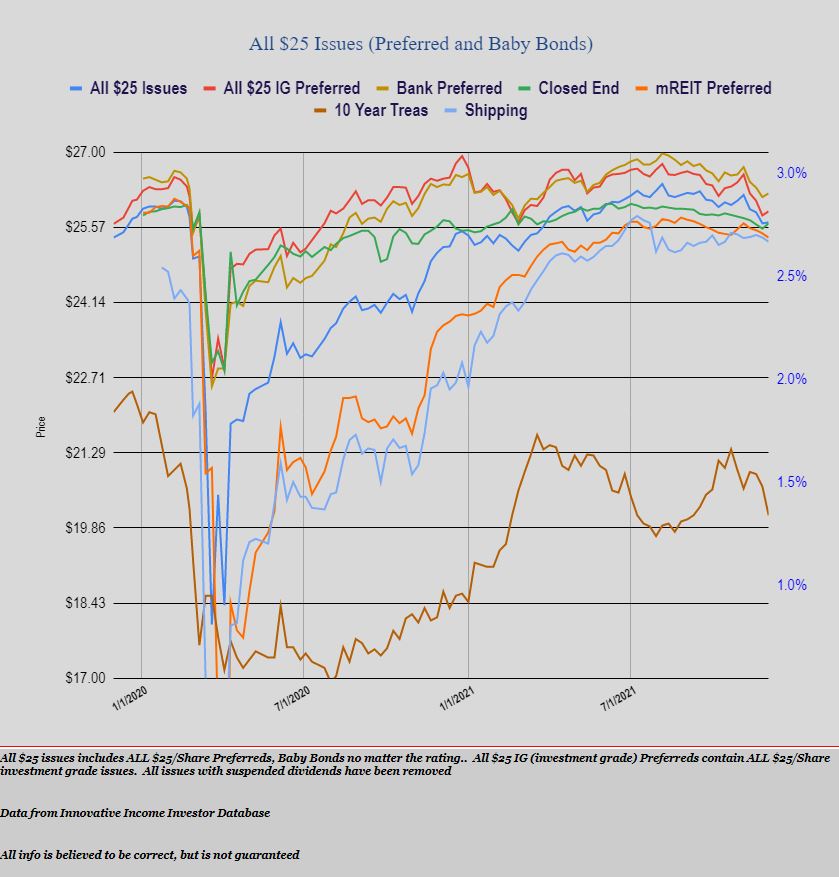

The average $25/share preferred stock and baby bond moved 2 cents higher last week although investment grade issues moved 8 cents higher. mREIT preferreds moved 8 cents lower.

Last week we had 3 new issues announced.

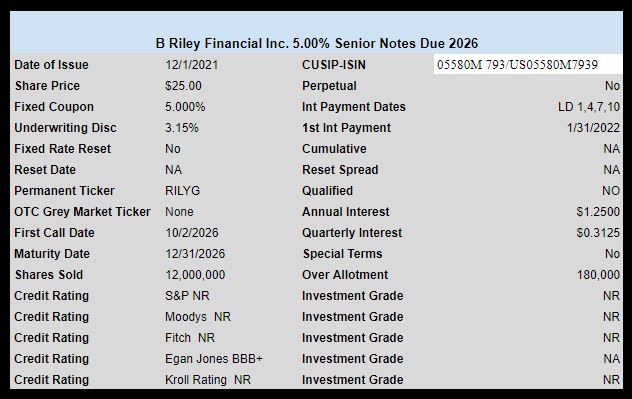

B Riley (RILY) sold a new issue of baby bonds with a 5.00% coupon. This is a giant sized issue of 12 million shares (bonds). Egan-Jones has rated this issue BBB+.

The issue is not yet trading.

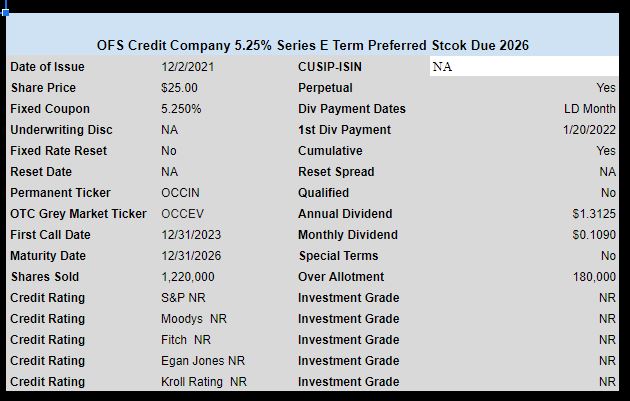

CLO owner OFS Credit Company (OCCI) sold a new issue of term preferred with a coupon of 5.25% and monthly dividend payments. This will be trading on the OTC under ticker OCCEV.

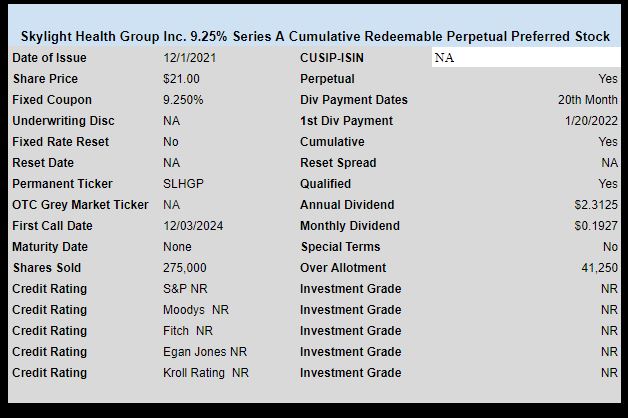

Canadian health services company Skylight Health Group (SLHG) sold a tiny issue of preferred stock with a 9.25% coupon. This issue was priced at $21/share.. This issue is now trading under NASDAQ ticker SLHGP and closed on Friday at $20.05. This is a monthly payor.

RILYG trading

https://www.otcmarkets.com/stock/RILYG/overview

Höegh LNG Partners (NYSE:HMLP) says it received a buyout proposal from Höegh LNG Holdings to acquire all publicly held common units for $4.25/unit in cash.

The proposal would take effect through a merger between the Partnership and a subsidiary of Höegh LNG.

The offer requires approval by the HMLP Conflicts Committee, the HMLP board and the Höegh LNG board, followed by the vote by a majority of outstanding common units in the partnership.

A contractual dispute that obstructed an otherwise routine debt refinancing nearly forced Höegh LNG Partners into bankruptcy earlier this year.

Have you any idea how this might affect HMLP-A? Thanks

If the deal goes through, I think it is bad for HMLP-A in the long run. In the short run, it might be good for a nice exit bump. The history of orphaned preferreds, where the common no longer trades, is not good, although there are some exceptions where the private owner treats the preferreds fairly. Given the recent financial woes of the now private parent, Hoegh LNG, I wouldn’t count on them being on one of the good guys if the HMLP common goes away in a private takeover. That’s a pretty lowball offer, and a conflicts committee with any backbone would push for a better deal – but don’t hold your breathe on that either.

If the preferred is delisted, is there no way to follow the price and can the parent stop paying dividends?

if the issue is delisted, it will eventually not have a price listed on an exchange and it will be very difficult to sell (nature of delisted securities). See, for example, the watford preferred that was delisted earlier this year.

You have to go read the prospectus about when/whether they can stop paying. sometimes you see covenants that they can’t pay other things if they don’t pay the preferred dividend. BIG YMMV. Lots of diligence required. HMLP-A is a cumulative issue, but that may not matter if they want to screw the preferred holders.

Personally, I hold a couple of delisteds that I am OK with – but you have to really do some digging and decide how much you trust management.

https://www.otcmarkets.com/stock/OCCEP/overview

Thanks af