Moving in a range of 3662 to 3826 the S&P500 closed the week near the high at 3825—a gain of near 2% on the week from the previous weeks close of 3756.

The 10 year treasury yield traded in a range of .91% to 1.13% before closing the week around 1.11%–a giant sized gain on the week of .19% from the close the previous week of around .92%.

The Federal Reserve balance sheet fell by $29 billion last week. The previous week the balance sheet had fallen by $41 billion. While these 2 weeks show a fall of $70 billion we will likely see a sharp increase in the next 2 weeks as the stimulus money is distributed.

Last week we saw the most damage to the average $25/share preferred and baby bond that has been seen in around 3 months. The average share fell by 18 cents–not too bad on average. Investment grade issues fell by a large 53 cents, with banks falling by 36 cents. CEF preferreds fell by 4 cents while mREITs gained 3 cents.

Price action in the $25 preferreds and baby bonds was typical last week during a time of rising interest rates. On a short tern basis high quality, low coupon issues fall the most during times of rising rates. These losses will be recouped in a few months if rates stabilize–if rates continue to rise prices will fall most on the low coupon issues as investors demand higher current yields.

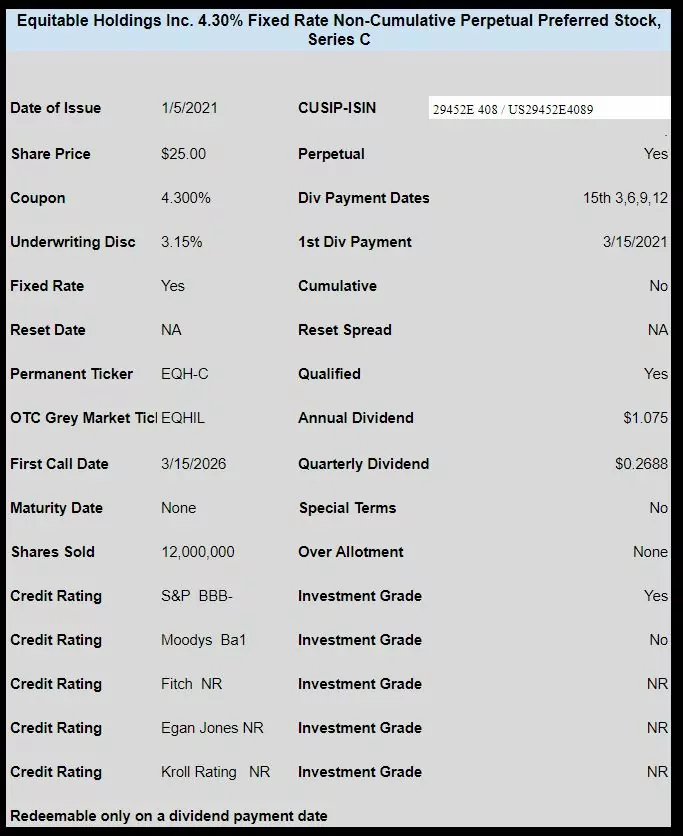

Last week we had just 1 new income issue priced as Equitable Holdings (EQH) announced pricing of a 4.30% non cumulative preferred. This issue is trading under OTC grey market ticker EQHIL and closed on Friday at $24.97. This issue is split investment grade (investment grade from Standard and Poors while a notch under investment grade from Moodys).

Given the general consensus that rates are going up its going to be interesting to see how the pricing of this issue stands up given it’s modest coupon.

I understand why lower-coupon issues would be more affected than higher-coupon issues when interest rates increase.

But why are investment-grade issues affected more than non-IG issues?

Bur, here’s a double dip on your interest rate comment. Although I’m talking municipals bonds the same applies to all bonds, CD’s, Pref’s. We have muni’s tax free and taxable across 3 accounts including retirement. Most were added 2 -3 year back when the “fed” was raising rates, even with that said, they average only 3%+ coupons 10-13 year duration, as conservative as I could get then. They now have $35k+ unrealized qains ” on the way down,” the yield to maturity or call stinks. They are all high investment grade, average AA or better. I can’t answer the IG vs non-IG questioned except that prudent investment decisions don’t seem to matter as long as the the market doesn’t set the interest rate.

Bur, I believe that the IG issues that also had some call protection are the ones affected. When rates rise, investors with low coupons get skittish as rates climb for fear of new issues coming out with higher rates. I think we all understand this 1st part. But, also folks that are seeing (or had paid a premium) are also evaluating whether they should sell and take the gains, or just hold until call, and let their premium and unrealized gains that they have enjoyed in their trading consoles the last 9 months evaporate. These drops are caused by those investors taking gains as well as making a determination that rates would continue higher and devaluing the premium on their investment.

In the end, I think we all welcome changes in the rates as it allows rotation and movement in the market so that we can enter some new positions for cash that we have accumulated.

Mr. conservative, you bring up a good point. The “premium bond” I’ve refused to buy a premium bond except some “build america bonds” with great rates in 2009-11 in a retirement account. I have enough trouble keeping up with real yields and actual returns without paying a premium knowing up front you’ll lose principal, not to mention the tax headache. Am I right or wrong? thanks Mike

Mike said: “without paying a premium knowing up front you’ll lose principal.”

Mike, I will overly generalize and say that all bonds issued before 2020, now trade at a premium. When medium to long term rates collapsed in 2020, it drove these prices higher. And yes, there were some default risk issues that did not follow this rule. So if you wanted to buy say a 5-30 year US treasury, corporate or muni bond, you were going to pay a premium. And that continues today. I see MANY CD’s, corporates and munis every day that have negative yield to maturity. In some cases, I can confirm that investors BOUGHT them with negative YTMs. I don’t know if the investors are planning on flipping them to a “greater fool” or just wanted to lose money when held to maturity.

And the tax consequences of buying bonds at a premium is not too bad IMO. Obviously if you hold them in a tax deferred account, it is not an issue.

Bottom line is that if an investor wants to hold individual bonds, you better plan on paying a premium above par. We bought many many (Not a typo.) CD’s, corps, and munis above par in 2020 and are still doing so in 2021. One of the accounts I manage currently has 329 bonds valued above par, of which 252 were bought above par.

Bur, Its just an overall generalization that lower yielding IG issues feel the heat quicker than higher yielding lower credit issues, because IG issues are always being roughly compared and traded off the govt long end.

But there is more to the entire concept including how tight the spread has become on junk also. I have about a month ago got a head of the trend started seeking “protection” in higher yielding issues such as ABR-A, SESCF, CEPQ-, etc. which have all held up nicely and even appreciated from purchase price.

That being said, I am not jettisoning all my IG perpetuals (mostly illiquids). I will tweak and trade to soften any losses going forward, but it is what it is. Im not going 100% junk in an attempt to “protect capital”. That last sentence certainly reeks of an oxymoron doesnt it, ha.

Another example of “hanging on” and grinding it out is PW-A. It was well over $26 before their recent common issuance which very possibly (even likely) to redeem. I finished up buying my 1000 shares today with a blend of $25.35 over 2 days. About a 48 cent divi as making it to exD appears possible. The risk reward here at this price is worth a shot. If nothing else at redemption other stuff may have dropped to switch into.

A lot of volume here past two days, so a call has to be assumed. Might be worth watching to pluck even lower for a few shekel pick up.

Just bought a little slug more at 25.07. Its very interesting at that price point.

I was very proud of myself, and thankful for warnings on this board, for getting out over 26. Couldn’t resist the drop though.

I bought even more at 25.13. Worth a shot.

Irish and Inspy, FWIW, I started peeling off some of these PW-A shares today in the 25.90s. Still holding, but banging out over 80 cents per share for one weeks hold it was time to reel it back into a more normal allocation size for me. I certainly cant complain about the start of this year, but it is going to be impossible to match last year.

Yep I let it go for more than the upcoming dividend too. I’ve enjoyed flipping this one many times this year!

Irish, This has been a frequent fun one for me over the years, too. It crazily jumped one time when I held $3-$4 bucks over par in a days time and that was a fun flip.

I have only a small amount, so no significant amount involved.

Will analyze and decide if I want to dump; if I do, it will go tomorrow.

Thanks for the heads up, I had forgotten about it.

Grid, I had also sold off PW-A at $26.10 some time back. Just bought back at $25.31, and $25.16 ( blended rate of 25.24 )

Even if a call comes today, with the 30 day notice, the accrued dividend should be above 30 cents, so I’m golden.

Inspy, Roughly 10% of the float rolled over in past 2 days (about 145,000 shares outstanding). If it stays outstanding until next divi, I will call this a successful play. We shall see….Family members owned about 10% of the preferred. If the ones being dumped today werent theirs we might see the next entire divi, lol..

Either way, you and Irish did well getting out when warned and reenetered at a good price point.

Inspy, I just checked. Squeeze out 19 more days before redemption notice and dividend will be paid in full.

Payment is in arrears and pay date is not pay period. So March 1, is full payment period, not 3/15. So next dividends will be payable quarterly in arrears for the preceding Dividend Period (as defined below) on the 15th day of March, June, September and December of each year or, if not a business day, the next succeeding business day, to all holders of record on the applicable record date. We refer to each such payment date as a “Dividend Payment Date,”, and “Dividend Period” means, with respect to a given Dividend Payment Date, the nearest preceding period among the following: March 1 to May 31, June 1 to August 31, September 1 to November 30 and December 1 to the last day of the next following February (other than the initial Dividend Period, which shall commence on the original issuance date of the Series A Preferred Stock held and end on and include May 31, 2014).

Grid – now that SESCF only trades on the OTC, when does it go ex-dividend? Can’t find the ex-div date anywhere. I do like the fact that these notes are now the financial responsibility of much larger and better capitalized ATCO (after its late 2019 transformation).

Ex-div this week? You are confident it will pay on 1/31/21? Atlas recently did a $175M 3.75% debt offering for the Seaspan subsidiary. Any chance they will redeem SESCF with the proceeds? Thanks!

SESCF reminds me of the delisted LTS notes (LTSH, LTSK, LTSL), but of course the LTS notes are now part of a highly leveraged Advisor Group. The LTS notes continue to pay.

Rob, you have to be a holder of record 1/15, but not positive about the important exD, which I assume 1/13, but not 100% sure. It pays end of this month. So I suspect its too late to capture interest payment this quarter.

Once they delist, notes are harder to track, as info is not as prevalently posted. I own another delisted note for 4-5 years now, and I have never seen a bit of info ever since its delistment. But it dutifully pays none the less.

Just for the record this is still a Seaspan note and obligation of the subsidiary Seaspan. ATCO is not guaranteer of payment. But I consider that a good thing. Kroll recently upgraded Seaspan senior secured to BBB-, so this senior note is probably BB range.

fwiw -Merrill Edge has the ex-dividend date for SESCF as 1/14/2021, but there’s no guarantee that is an accurate date. Who’s your broker?

Citadel, this old link from when SESCA was SSWA would support your info from Merrill. This showed in 2019, exD was Jan. 14 2019 and record was Jan. 15. Seems awfully tight. I would hate to buy this as a pure play interest payment capture without totally solid info though.

https://marketchameleon.com/Overview/SSWA/Dividends/