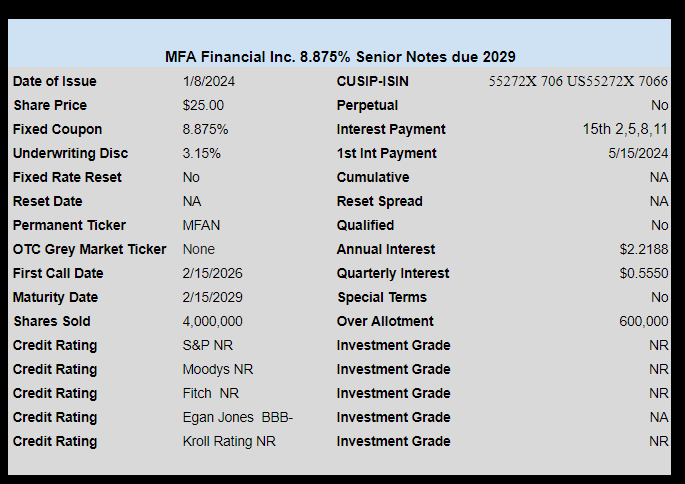

Below is the pricing detail for the new mREIT MFA Financial baby bonds priced last night.

This issue will likely start trading sometime next week.

The pricing term sheet is here.

7/25/2024

Our site runs on donations to keep it running for free. Please consider donating if you enjoy your experience here!

Below is the pricing detail for the new mREIT MFA Financial baby bonds priced last night.

This issue will likely start trading sometime next week.

The pricing term sheet is here.

MFAN selling today in the $25.20 range. Anybody buying? I sold some MFA-B in anticipaton but holding out for a slightly lower price.

Help me understand how a mREIT can borrow at 8.875% in this market and make money.

Exactly. Particularly as there is no tax shield. The mREIT preferred issues are also expensive capital NLY is paying ~10% now.

This firm has about $8B in whole loans financed with $8B in “financing agreements” from the Q:

“The Company finances the majority of its residential mortgage assets with financing agreements that include securitized debt, repurchase agreements and other forms of collateralized financing.”

This $100M is expensive, but not collateralized so it gives them some measure of flexibility I suppose. Out of $8B this $100M really wont change their overall capital costs much and evidently provides some small measure of flexibility in that it is longer duration and fixed coupon. It is also looks like it has been priced (relative the preferred) to ensure a pop when it starts to trade. Seems like they could have locked in a lower coupon.

Interesting to see how these trade relative to the preferred.

That’s the going rate for their ilk. Make money on leverage, or if trouble strikes lose money for the same reason.

Same as MFA-B current dividend. B doesn’t have a maturity date but could have more price upside. I’ll switch to MFAN if the price is right.

Senior debt in front of Preferred in capital stack. Seems like senior is way to go if yields are about equal. 🤔

But if the plane hits the ground hard enough, it doesn’t matter if you were sitting in back or up front.

This is an interesting dilemma – there is a ton (~$8B) of Sr Secured debt ahead of Sr Unsecured ($100M) in the capital stack. The total debt is financing about $10B of assets of which $8B are whole residential loans.

Yes these bonds are Sr to the preferred, but they are Jr to Sr Secured.

I am wondering how much protection the seniority really provides in practice. Also we should also remember that the preferred is cumulative.

It will be interesting to see how these trade, but I am wondering if the fixed rate preferred is the better option as they are nicely under par and callable now.

August, that is always a good question to ponder. Keep in mind what looks good could look worse later. As companies tend to keep the “senior secured” more clean as that allows later flexibility to access capital if ever needed. And even after that you can get hosed by Bank or DIP that immediately slides above the stacks.

Generally one isnt likely to collect if they are holding a subordinated note and in general doesnt carry much more safety than a preferred. Though depending on situation the market tends to give them a bit of an edge in pricing over preferreds though. Senior unsecured in general is where more crumbs start getting passed out to the bag holders.

This isnt any be all info, and not totally relevant, but it at least throws a number at you, from this year.

For those representing lenders and creditors, the recovery rates in bankruptcy underscore the importance of perfecting liens. According to data compiled by NGR on 1H bankruptcy filings, the average recovery rate on first position lien debt in Chapter 11 bankruptcies was 68%, while the recovery rate for unsecured debt averaged 35%. Put differently, first position lienholders were able to recover $0.68 for every dollar owed, while unsecured creditors recovered only $0.35 for every dollar owed.

https://www.wolterskluwer.com/en/expert-insights/bankruptcies-are-on-the-rise-and-what-this-means-for-transactional-attorneys#:~:text=According%20to%20data%20compiled%20by,for%20unsecured%20debt%20averaged%2035%25.

Thanks Grid – I am not sure that average recovery rates really apply to mREITS. The most likely failure/BK scenario for an mREIT, it seems to me at least, is either a melt down in mortgage credit (MFA is not an agency player and does take credit risk) or a run on the short term repo financing supporting the mortgage book. Most likely a combination of the two.

In either case there is not much equity left for Sr Unsecured or Preferred.

In any event – I will be interested in seeing how these bonds trade.

August – Just wanted to share my 2 cents, how I generally get comfortable with MREIT prefs.

yes a “melt down in mortgage credit” is absolutely a risk. But most of the credit names use securitizations to finance their positions. This gives them years to work out any stresses, and many of the issues are non-recourse. If a levered credit play uses mark to Market financing, be VERY wary. I.e. GPMT..

The agency names are financed by repo, but the beauty of this is that they are almost always margin called way before the equity is impaired. And agency mbs is very liquid and can be sold near the marks.

Just look at the COVID crash. It was the most violent and quick rise in spreads we have experienced in decades, yes even greater than ‘08. Some of the credit names got close to a wipeout (see MITT) but even they survived.

After they took their book value beat down, they issued new common equity to solidify the balance sheet. Management and pref holders are strangely aligned in this regard.

disclosure: long many MREIT prefs, including MITT-C, AGNCL, and RITM-B

P.s. one other thing, the best time to invest is generally after a disaster. COVID was a disaster for MREITS. Many shops implemented controls to reduce risk going forward. for example, MITT switched 100% to non-agency and very little mark to market and recourse financing.

I am not against mREITS at all, and have NLY F and G in my portfolio. I also have a very small amount of RWT A. I have also owned CIM and AGNC.

So don’t get me wrong I am not against mREITS.

My only point is that when you want there to be a difference between bonds and preferred (when it hits the fan) I only wonder if Sr unsecured will provide the protection over preferred that one expects.

To me – if the choice is between a Sr Unsecured bond issue at par with the same current yield as a preferred which trades at a discount to par I might be inclined to go with the preferred (the cumulative aspect of the preferred is a minor point, but makes the comparison easier)

If both issues were at par this would be a different story.

I wrote:

“before the equity is impaired.”

But I meant to write:

“before the equity is wiped and the prefs are impaired.”

couldn’t help but post a clarification!

BTW, anyone playing with the BPO canadian prefs? Some trade in the 7’s. That enough “margin of safety” for you?? If i had to guess, BN offers a tender to buy them below par, but well above $7.

Yes, August, I am just giving generalized numbers. Certainly not specifically applicable to this company or the sector. I generally like subordinated debt from IG senior unsecured companies. As I get more yield while piggy backing off the IG relative safety. As sub debt cant go bankrupt unless the senior unsecured does too. I havent made my mind up if I will buy for a flip on this issue or not.

Grid thanks for the feedback and comments.

For now I am going to stand still and wait.

My window here really is the March-May time frame. I have a couple of positions on in RILY that expire/mature in that time frame. Either something like MFA Preferred or Bonds or a BDC bond would fit nicely in that slot. So I am happy to watch and see how this trades.

It is good that we seem to have so many choices in this environment.

Grid

You comment here is interesting in light of the news from ET. They will be issuing a both Sr and Jr Sub debt to call the preferred. You your logic the Sub Debt might be the better play in this case. Of course depending on how it’s priced.