With these wild markets investors will be looking for any possible weakness in economic data released.

Next week we have 15 Fed speeches (or presentiations) that are scheduled to take place. These are always ‘wild cards’ as each of the messages are not ever in sync–at least have not been in the past–any one of them could send markets higher or lower. One has to believe that they will choose their words more carefully than they have in the past.

On Tuesday we will have Durable Goods Orders for August released–the forecast is for a drop of 1.2%.

We also have the Consumer Confidence Index for September released with a forecast of 104.5 versus 103.2 last month. Below is some history.

New home sales will be released on Tuesday with forecasts of 505,000 units versus 511,000 last month.

Wednesday we have pending home sales for August.

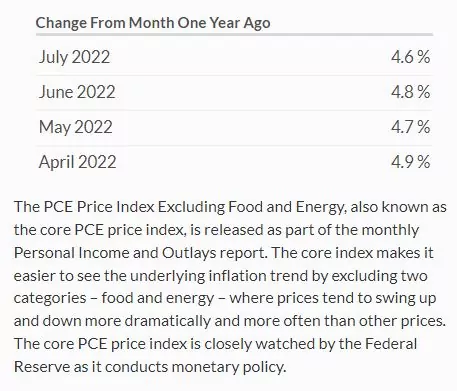

Friday we have a biggie in the PCE (personal consumption expenditures). Here is the recent history for ‘core’ PCE. Forecasts seem to have this ticking higher by 1/10 point–any number under last month would be helpful.

So in summary hard economic data is minor until Friday—assuming the Fed officials don’t get carried away with their comments during their speeches and presentations.

I’ll be watching on Tuesday if GDP NOW goes negative after durable goods orders. We are very close to getting 3 straight quarters of negative GDP. The spin meisters will be busy.

I was watching Bloomberg this evening.

I was surprised to see the SOFR jump 74 basis points, to 2.99.

SOFR is not something I usually follow, as the jump from LIBOR to SOFR for floating -rate preferreds is still out in the future, with uncertainty (at least in my mind) as to how smooth the transition will be, and how much you can count on something being “added” to SOFR.

Does SOFR run lock-step with the Fed Funds rate?

If so, why not just use the Fed Funds rate to replace LIBOR, and not fool with SOFR?