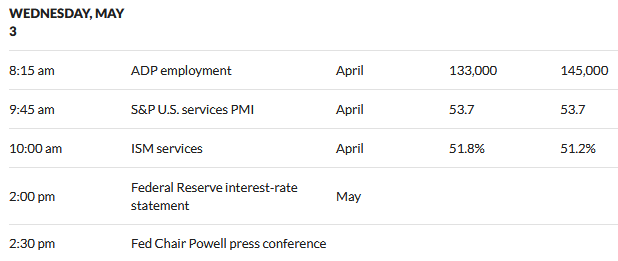

All eyes are on the FOMC for the interest rate decision at 1 p.m.(central) and the consensus is a ¼% rate hike. More anticipated is the press conference with Jay Powell at 1:30 p.m.- what will he say about the future? On one hand Powell can’t appear to be soft on inflation and on the other hand he can’t turn dovish. We are likely to get major market moves regardless of what Powell says in the press conference.

Yesterday we had interest rates drop sharply after a large spike on Monday – the 10 year treasury closed Tuesday at 3.44% as the JOLTS report showed a decrease in job openings and layoffs are increasing – so a sign of a weakening economy. Today we have a few other economic releases including the always unreliable ADP jobs report for April.

Most certainly I will sit on my hands today which is the typical day for me for many weeks (or has it been months). We are not going to be able to buy any banking for quite a while–although for those willing to try to ‘catch a falling knife’ there are many issues of the smaller banks with current yield over 8%–stay with small positions and diversify across a basket.

Yesterday I was reviewing current offerings of CDs and there were issues available at 5.25%, but just like the terms of preferred stock and baby bonds banks can play around with the terms. Most of the current offers pay interest at maturity and the highest coupons are callable – I like monthly payers that are non callable, which pay a lower interest rate. We’ll see what is available later this week after Fed actions–I may go ahead and lock down some more CDs since it is unlikely I will be buying preferreds or baby bonds for some time.

Well let’s get the day going – it is going to be a wild afternoon.

It’s nice to get a proverbial second bite at the apple of ~5% CDs. Seems to me the settlement dates have been getting stretched out on the higher yields recently, some five to seven days. Used to be anything I bought would settle in a day or two.

I prefer (and currently own only) non callables, 6-12 months, but I am trying to rationalize callable 5%’s at 12-18 months as some sort of a high yield synthetic MM fund where there’s always a risk of lower rates. If rates drop, and I get a call, I’d probably want to get my money back to reinvest elsewhere anyway. Just thinking out loud.

BearNJ;

Exactly right, I bought a Government bond (FHLB) months ago that has a 6.1% rate for 10 years, but it is callable in 1 year then semi-annually. I bought it with the idea in mind if it gets called at the 1 year mark, it still beat any 1 year CD rate available at that time and if it doesn’t get called, it’s bonus time. Deals like this haven’t been available for so many years I can’t count them. The last Government bonds I bought ( in the 1980’s) were zero coupon STRIPS that paid around 10% if held to maturity. Higher rates could go away very fast, get them while you can.

Government bond? FHLB is a regional bank.

Quasi Government ? At any rate, Schwab has the FHLB bonds listed as “Government Agency” bonds. All backed by the same printing press I suspect.

What Is the Federal Housing Finance Agency (FHFA)?

The Federal Housing Finance Agency (FHFA) is U.S. regulatory agency that oversees the secondary mortgage market and players within it. Established in 2008, the FHFA’s responsibilities include supervising Fannie Mae and Freddie Mac, as well as the “11 banks that comprise the Federal Home Loan Bank (FHLB) System” and the Office of Finance (OF), a joint office of the FHLBanks

Bill S. – Ok, you were referring to Federal Home Long Bank System not the regional bank Friendly Hills Bancorp (FHLB) which recently changed its name to First Pacific Bank.

danzeb;

Yes, sorry for the mix up.

Symbol “FHLB” does actually trace to Friendly Hills Bancorp not Federal Home Loan Bank system, the Govt sponsored agency.

Not sure any of us would want that Fed Chief job right now.

alpha–the pay is pretty meager–no thanks.