The 5.4% non callable mentioned below is gone–I doubled back to get a little and they are sold out.

I don’t watch CNBC much–a little bit premarket, but other than that it is so much news I don’t need, but on occasion I miss news items that happen minute to minute.

The big banks are going to ‘bail out’ First Republic (FRC)?? Wow that is decent news I think–I haven’t looked at the details, but I hear the big banks (jpmMorgan etc) are looking to put $20 billion into FRC. On the surface big banks bailing out small banks sure seems preferred to the treasury stepping in–whether it makes a difference depends on the true strength of the big banks.

Regardless the preferred shares of FRC are flying. After opening flat in the $9/share area all the issues are trading up $3-5/share. In fact when I look at the bank and insurance preferred page it is extremely green. Looking at my accounts they are modestly green also–I never argue with green.

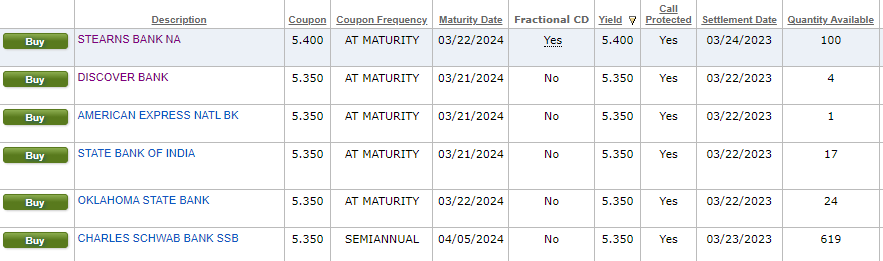

I note today that we have a new CD available from Stearns Bank (which is in Minnesota) offering 5.4% on a 1 year–non callable issue. Not many available on Fido and I am sure they will be gone quick.

I wonder what happens to the preferreds if FRC is sold. Am I correct in that they would need to be paid in full before the common shareholders received anything?

The bank has taken such a hit have to believe that’s an option.

Understand FRC suspended its common divvy after hours. No mention of the preferred divvy.

Anyone have a calculation of the quarterly cash requirement of the preferreds vs. the common?

Right now at Schwab a bunch of 1 year non-callable CDs.

CUSIP 23204HNJ3 Buy Fixed Customers Bank PA 5.4% CD 03/22/2024

23204HNJ3

Recently Issued 5.400 At Maturity 03/22/2024 — Ask 25 100.00000 1 29326 5.400 — — 25,000.000 View

CUSIP 857894J42 Buy Fixed Stearns Bank Ntnl As MN 5.4% CD 03/22/2024

857894J42

Recently Issued 5.400 At Maturity 03/22/2024 — Ask 25 100.00000 1 914 5.400 — — 25,000.000 View

CUSIP 06740KRN9 Buy Fixed Barclays Bank Delaware DE 5.4% CD 03/21/2024

Recently Issued 5.400 At Maturity 03/21/2024 — Ask 25 100.00000 1 80 5.400 — — 25,000.000 View

CUSIP 02589AEL2 Buy Fixed American Express Ntn UT 5.35% CD 03/21/2024

Recently Issued 5.350 At Maturity 03/21/2024 — Ask 25 100.00000 1 1948 5.350 — — 25,000.000 View

Has anyone gotten paid interest at the rate of their CD if the bank fails? My understanding is that the principal will be repaid by the federal deposit insurance fund but the interest is not guaranteed for the full term of the CD. Unfortunately, the listed regional banks (not sure about the size of Amex bank) ability to survive this incredible mess is debatable caused by Herbert Hoover Jr. aka Jerome Powell, Congress, both political parties and Janet Yellen aka Mrs. Herbert Hoover. Without the regional banks, small business lending is in serious trouble. Home building by small builders is in serious trouble. Not much left for the economy after that with a nation currently with a 1.7 trillion dollar annual deficit and 29 trillion in debt already (not counting unfunded pension liabilities of 50 Trillion if not more). Powell and Yellen are on the verge of infamy for the next 100 years around the world if things continue to get worse. My grandparents who survived the depression never forgot the name Hoover and cursed the name for the next 50 years of their lives.

Home builders rely on many sources not just the banks. You have local funding sources such as RWT who are not FDIC or as heavily regulated and they can take on bigger risks than the banks can. They are also more willing than banks to foreclose on the developers to recover assets. This is why your getting higher rates of return on investments like AGNC as your sharing the risk. This is why I own no MREIT’s at this time, but am willing to risk holding bank preferred because of the illusion of federal backing.

Here are the basic main rules as posted to me from TD….

… As with all deposits, if it becomes necessary for federal deposit insurance payments to be made on the CDs, there is no specific time period during which the FDIC must make insurance payments available. Accordingly, you should be prepared for the possibility of an indeterminate delay in obtaining insurance payments.

As explained above, the $250,000 federal deposit insurance limit applies to the principal and accrued interest on all CDs and other deposit accounts maintained by you at the Issuer in the same insurable capacity.

…..

Insolvency of the Issuer. In the event the Issuer approaches insolvency or becomes insolvent, the Issuer may be placed in regulatory conservatorship or receivership with the FDIC typically appointed the conservator or receiver. The FDIC may thereafter pay off the CDs prior to maturity or transfer the CDs to another depository institution. If the CDs are transferred to another institution, you may be offered a choice of retaining the CDs at a lower interest rate or having the CDs paid off. See the sections headed “Deposit Insurance: General” and “Payments Under Adverse Circumstances…..

Thanks Grid for your post. Much appreciated. The “indeterminate” time for the FDIC to pay you on your funds is not something worth having a CD in any shaky banks. Furthermore, your post clarifies that you are not assured that you are going to get the interest rate you began with if the bank becomes insolvent from the date the bank is deemed insolvent.

Clipping the 4/5 of your post that is political soapboxing and focusing on the actual question,

> Has anyone gotten paid interest at the rate of their CD if the bank fails?

The answer is yes. Here’s how the FDIC puts it:

> FDIC insurance covers depositors’ accounts at each insured bank, dollar-for-dollar, including principal and any accrued interest through the date of the insured bank’s closing, up to the insurance limit.

In other words, so long as principal + accrued interest is still below the insured limit, you’ll get it paid to you.

FTM, like Grid posted, the FDIC will reimburse you for principal and accrued interest with two caveats:

1) If you paid over par (aka $100), you will suffer a capital loss because the FDIC will reimburse you at par. Not really an issue for CD’s you buy now, but if you hold some that were purchased when interest rates were low, it is an issue. We hold hundreds of issues that were purchased above par, because that was all you could buy on the secondary market back then.

2) There is no implied “make whole” provision when the FDIC pays these out. You might think you have a 5 year 5% coupon CD with 4 years before maturity. If the FDIC takes over tomorrow, you will NOT receive the additional 4 years of interest.

Added note: During the 2008 GFC, the FDIC became very proficient at quickly paying off CD’s of failed banked. It took them a while to get good at it, but they got better with more experience.

2nd added note: in a perverse way you are hoping that banks fail if you bought the CD under par on the secondary market. You will get an outsized return in that case, but it is unseemly to be hoping that a bank fails.

T2

Tex you are much more knowledgeable than most of us. But things can change. It’s been 15yrs since the GFC . Not saying it is the same. But I talked to a friend last night that is dealing with the IRS another G agency over getting compensation. His CPA was hacked and his tax return was diverted and his SS# stolen and his bank account also comprised. His CPA confirmed it and police report filed. The IRS admits he is owed his money but told him it would take some time. Several reasons were given that the refund was still being delayed. Before his call yesterday it has been a year. Now that has been extended another 100 days. The information Grid posted points out there is no specific time to make a CD owner whole.

I only buy CD’s that pay monthly, sometimes I take a little bit less than paid at maturity ones, but I invest for monthly income, so it works best for me. I bought a 1 year 5.4% ConnectOne CD CUSIP# 20786AFK6 from Schwab today that pays monthly.

I do too, Bill, when I can.

I have had depositor monies at hundreds and hundreds of banks that have been taken over/failed/restrutured. You are insured for principal and interest unto insurance limit. Whether the CD continues to maturity date is an open ended question.

Failed banks. Money sent back. Maybe a period when your P doesn’t earn interest. Once in a blue moon FDIC will test the valifdiity of the depositors (pooled/brokered CD/trusts/etc) If rates are lower you lose the rate. If rates are higher you tend to get to reinvest.

Taken over bank (Shot gun wedding). In many cases everything honored to maturity. But there is possibly an escape clause for acquiring bank. Where/when they can break the CD and send you the P+I.

Restructured bank…Such as adding ‘The New XYZ Bank’. Again no guarantee cd goes to term.

Secondary FRC cds hit this week. Wayyyy over market fully insured at a discount. The risk was that one might have learned about the name in the news (the hard way) and perhaps FRC could fold and the be subject going non interest bearing for a stretch. But they’d have to pay off at face so any discount to principal would be credited to investor.

Then there’s also a difference in treatment whether the CD is direct with bank. Or a brokered CD directly into bank….Or if it’s pooled block securitized brokered to bank.

I go back to having done business with Charles Keating and all of the rest in the 80-90s. Those old enough might remember when they told every S+L in the country to sell their junk bonds before a date. Like 6/1/1990. The prices went to 5 cents on the dollar. And the Treasury created RTC to handle the over 700 failures. They issued bonds I think they were called FICA bonds. Included Zero’s out to 40 years at like 12%. They all paid off in full. It was a bonanza. Zeros were hard to find, and tended to be CMO tranches that had questionable pre payments. To have a government backed 0 paying 3% over treasuries going 10 years longer with juice like you’ve never seen. Well as I said anyone who bought these on faith got the kicker of their life time.

The biggest failure I can remember was Bank of New England. Their deposit notes were FDIC insured, but sold in 500K and million dollar blocks. Well they were dumped at 90 cents on the dollar. Broken up and sold for par. Quite a mark up! They too all paid off

I had a CD at Washington Mutual when it was taken over in a shotgun wedding by B of A. They paid me P & I at maturity, except that they deducted a $50 fee. I complained to management and they coughed up the last $50.