So today we had a dovish producer price index which was on top of the softer consumer price index–of course this is excellent news for us all.

With the most recent data the hawkishness of the Fed is no doubt going to be softened this month–but does that mean no rate hike?

The FOMC is in a pickle. Two weeks ago I thought–and many people thought — 25 basis points was a cinch while 50 basis points was ‘on the table’. Now any rate hikes at all will serve to worsen the banking situation–higher rates equal lower bond values. Of course the Fed now has backstopped much of the underwater bonds held by banks–but just the same the Fed will not want to exacerbate the situation. What to do? It will be extremely interesting to watch next Wednesday.

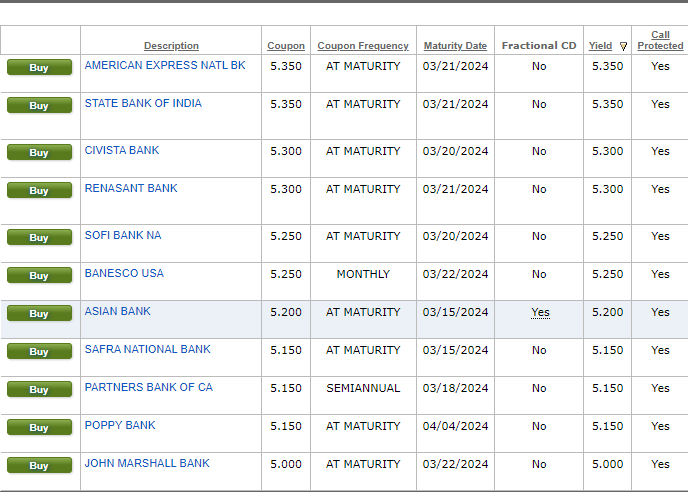

Today I bought more CDs–1 year maturity. Here is what I found at Fido right now for 1 year terms. I bought the American Express 5.35% which is call protected (as all those below are).

I took a look at the 2, 3 and 5 year maturity issues–but once you move out in maturity many (or most) are NOT call protected so for now I stuck to the 1 year. We will see where they go from here and what is offered–I have quite a few treasury notes maturing later this month so will be considering further CD’s. I really need the markets to calm before I start heading back into the preferred issues–of course I won’t catch the bottom in preferreds, but I never do since I am a lower risk investor.

Thanks for listing those CDS. Other than AXP I never heard of those others,

Where are JPM, WFC, and the other big banks? Doesn’t look right explain why?

1) With the loaning of cash to the banks against Treasury Securities and MBS at PAR is the FED still in QT or are we sliding closer to QE rev 3.0? I am confused.

2) The special assessment from the FDIC has not been determined yet and, of course, will not be for a while. Will all deposits be defacto insured now or only those which are under the 250k limit? Either way bank insurance rates are going to increase. Will the effect to the net interest margin be significant? The banking industry is not going to like it.

The changes in yield for the 2yr and 10yr are quite dramatic. Amazing how quickly things can change. In a few days the inversion could disappear.

The inversion between the 3M and 10Y is pretty steady at 110-120? The 3M is said to be the more reliable indicator?

Not sure to be honest. I think I have read something like that before. It just seems like when the 2/10 inversion ends it signals a recession before the 3m/10 even bottoms…

But I am just eyeballing FRED charts and was thinking in terms of a recession and rate cuts.