Yesterday’s euphoric rise in stocks and bonds is quickly fading away this monring. I really don’t think that any of us thought ‘the bottom is in’ given that the economic data simply doesn’t show the weakening economy that is being blabbered about constantly of late.

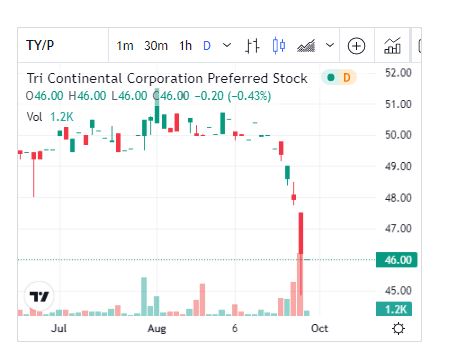

Today once again I am mostly just watching the markets–I say mostly because there are fair odds during the course of the day I may nibble a bit. Yesterday I had no intention of buying anything, but the Tri-Continental $2.50 (5.00%) preferred (TP-P) took a bit of a tumble so I nibbled shares with a 5.40% current yield. This $50/share issue has been outstanding since 1963 and has a call price of $55–yesterday it closed at around $46. I consider this unrated issue to be the safest CEF preferred in existence with a asset coverage ratio of 4400% as of 6/30/2022. They hold all Level 1 securities (exchange traded securities-common stocks etc).

Just looking at the markets stocks are tumbling hard–off 2.3% while the 10 year treasury yield has risen 8 basis points after the giant 25-30 basis point tumble yesterday–a little stability here would be great to see, but after the strong jobs numbers this morning as well as some hotter inflation numbers I think rates are destined higher.

Wish I was one of those lucky people who bought TY-P back in the 1980s when it was trading in the $20s. I was fresh out of high school back then and inherited $10k. So I didn’t blow it on beer, Van Halen tickets, and a used Trans Am, my dad bought a 12ish% CD with it for me. Will we get there again? Who knows but with the fed hell bent on sopping up the unprecedented amount of cash sloshing around, I think maybe.

Among the best opportunities to me in the current market are investment grade, large cap BDC with bonds maturing in 3-5 years yielding in the 7.5%-8.0% range. No BDC has ever gone bankrupt, and these large cap I-grade ones are very solid with approx 2 coverage. I have been adding 2026 bonds of Main Street Capital and Hercules Capital, both 2026 bonds yielding close to 8%. Holding to maturity.

Looks like the market is trying to find a bottom at the June lows? Time will tell as when the inflation, interest rate increases and future earnings are not such a question mark?

It’s certainly easy to take a day off as tomorrow always seems to be worse.

I’m seeing some stupid dumping. Capitulation?

Joel, Seeing the same thing.

We’ve been adding proportionally to positions daily with occasional surges in activity that occur within a 2-3 minute period. This phenomenon has occurred half a dozen times over the last few weeks.

Know nothing, but I suspect these to be index fund dumps which create temporary imbalances in the standoff between bid and ask. In at least half of those scenarios we’ve been able to sell back to the market for a few filet mignon gains and re-buy at an even lower price (full round trip) within 24 hours.

Bit hectic, but driving down average cost and increasing portfolio yield every day. Overall yield of holdings is now 6.22% with an average rating north of BBB+.

Tim, a large financial question involves your day job. Assume you appraised a house at $100k on January 1st, when 30 year mortgage rates were roughly 3.0%. This week they hit ~ 7.0%. So what will that house appraise for today? And yes, we understand that potential sellers are still thinking it is worth $100k, but the market might disagree.

BTW, this is going to dramatically kill house sells, even ignoring buyers can’t afford the house they used to. Think of a potential seller that currently has a 3.0% mortgage. Are they going to sell and buy a new place with a 7.0% mortgage? Gotta be pretty rare.

The other related question is how long will take for prices to fall into the economic reality range. . .

Interesting stuff. . .with a few MINOR implications for the broader economy.

Tex–here (rural MN) it would be unchanged. I suspect prices are heading lower–BUT at this moment I can not detect that occurring and with the use of backward looking data (I use sales looking back 1-5 months) no change is detected (up or down). I am putting a note in now ‘markets are in the process of changes etc., etc.). Over my twenty something years of appraising I note that the west and east coasts change much more rapidly than the midwest–in both directions. We continue to have a giant shortage of properties.

Ask me this question in a few months and I suspect my answer will be different.

I am thinking at least 6 months to a year for housing prices to adjust. If you are thinking about a home equity loan get it before home prices adjust downward.

The fire sale looks so good on almost everything…..but then every time you buy today it drops another 2% tomorrow and the next day and the next. The fed is hellbent on driving the global economy into an active volcano, so why fight it. Wait until SP500 hits 3000 and mortgage rates hit 10%….then maybe buy a little.