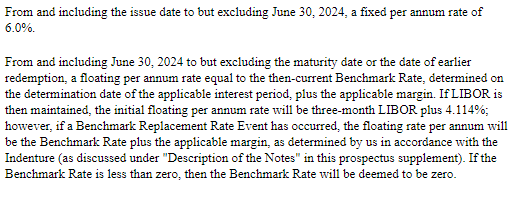

A few of our astute readers (sorry lost track of who these folks were) commented recently that baby bonds of the First Internet Bancorp (INBK) have a clause in the floating rate reset determination section of the prospectus that states the following–

The key part is the last sentence which reads ‘if the benchmark rate is less than zero, then the benchmark rate will be deemed to be zero’.

While I don’t expect that we will see a zero 3 month Libor rate anytime soon, I also didn’t think we would see a 10 year treasury under 1%.

What this means is that if 3 month Libor went negative you would have a ‘floor’ coupon of the spread used to set the coupon rate. For instance the First Internet Bancorp 6.0% baby bond (INBKL) has a spread of 4.85% which will be added to 3 month Libor. Thus 4.85% will be the lowest coupon this floating rate issue would be reset at.

I did some random looks at other mREIT issues and did not find the language that set the 3 month Lior floor at zero.

This is likely not a big deal–BUT you may want to know if you have a floor on your floating rate issue–the details are in the prospectus of each issue.