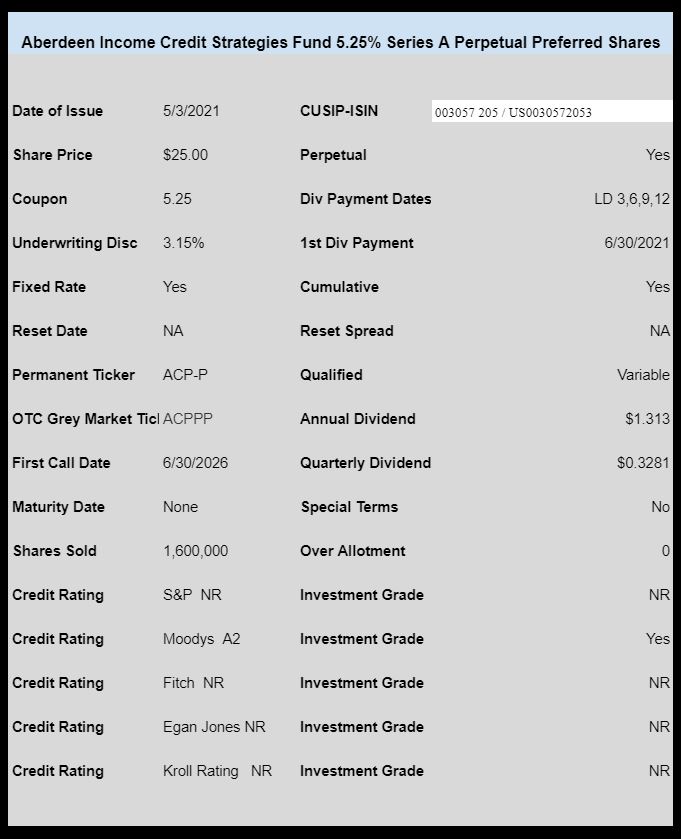

Closed end fund Aberdeen Income Credit Strategies Fund (ACP) has finally priced their new issue of preferred stock.

The issue prices at a rock solid 5.25%. This issue is rated A2 by Moody’s and will be one of the highest rated preferreds outstanding.

The issue will be trading immediately and the OTC grey market ticker will be ACPPP.

The pricing term sheet can be read here.

Bob-in-DE and aview were on top of this one.

I see this was only a 40 million dollar deal. That’s OK for some but in general I can’t be doing a lot of this issue. A few positions at most. I don’t want to own issues that might go dry on volume.

Aberdeen has a good reputation, with open end mutual funds anyway. They know what they are doing. Compare them to Highland? They blew up billions in their CEF…… never to be returned. From 20 to 3 and never back to 10. The bid ask on Aberdeen was big enough to drive a truck thru at 3PM today but that should close up.

Leverage on CEF’s is often misunderstood. In my opinion it’s playing with fire but …….but the A rating is solid!! As for the coupon I’m happy! I hear people bellyaching when the rates are set too low, now we complain about the rate being too high???

A CEF preferred backed by liquid, low volatility holdings in not “playing with fire” at all.

I’ll make it as simple as possible: the scenario in which such a CEF preferred is impaired is an environment in which you would have considerable defaults across the rest of your bond/preferred portfolio, not to mention the stock market would probably be down 80% or more. Just because you imagine the CEF preferred to be riskier doesn’t make it so.

As always, I distinguish between CEFs with liquid. lower risk holdings vs those with illiquid, high risk holdings. Personally, I avoid the latter unless they are trading at a substantially higher yield (which ain’t the case today).

I’m referring to the CEF itself..

Dude you’re preaching to the choir I’ve been in he bond market since 14% rates

Temp ticker was changed to ACPPV this morning, 5/5.

ACPPP

Chart

Last Price$25.82 /1 N/A

Day Change+0 ( 0.00% )

Bid/Size25.82 /1 N/A

Ask/Size25.95 /2 N/A

Day Range25.75 – 26.42

52 Week Range0.00 – 0.00

Today’s Open25.75

Previous Close0.00

Volume

76,961 (Schwab )

The people who price these things, have they never traded a preferred stock before? I’m searching for an explanation for why an A2 rated preferred gets priced at 5.25%. Maybe kickbacks or hanky-panky for friends and family?

Its always interesting how a potential relative value trade or buy quickly dissolves into a greater fool trade play, which I am not doing here. Better relative values now being its at $26. I just bought a chunk of DTJ at $25.33. That already is under par, being it pukes out the 34 cent interest payment exD, next week. Dare them to call it, you have nothing to lose and utes are notoriously slow at redeeming. They have 6% DTY becoming callable end of year, so they may wait and redeem that first. And you also know sister 4.38% is over par itself. So the DTJ is definitely a relative value play here. Would much rather milk this cow than grab the udder of ACPPP at $26.

I like that value Grid. I had to pay a penny more than you at 25.34 for DTJ if they call it, I break even. If they don’t, nice yield in this environment for a ute

Maverick, you are already in the money big time. Its already accrued 5 days of additional interest even if they announce redemption tomorrow, ha.

I was able to join Maverick in getting a small amount of DTJ at $25.34. Let it roll!!

With the call set for June 30 (I believe) what is the accumulated interest for then? I am confused, but that is normal.

The 2016 Series B 5.375% Junior Subordinated Debentures will be redeemed on June 30, 2021. The redemption price is 100 percent of the unpaid principal amount of the 2016 Series B 5.375% Junior Subordinated Debentures, together with accrued and unpaid interest up to, but excluding, June 30, 2021.

I am unclear how many days of interest will have accumulated–if from last payment date, then I think it is from June 1, per TDA.

It will be about 11 cents

I put in a gtc sell at 25.15. If it hits, good, if not I’ll take the 25.11

I see 13 cents accrued interest and a ask of 25.39 so isn’t that a risk of 26 cents? It’s a negative yield to call

My calculator is wrong you are right.

I’m curious on how this preferred is used. Is it used to assist the cef ACP fund? My quick reading might yield errors, but it seems that it has 3% in fees, has a high payout ratio (subjective) and at least for 2 years has return of capital. So the fund is definitely not for me, and am curious how this preferred is used.

So for me, I am not a buyer until I know more, no matter what the ratings are from Moodys as that is just 1 metric in a sea of metrics.

MrConservative–I’m sure it is used for ‘leverage’. The fees on Priority Income Fund are out of this world (compared to Aberdeen). I look past the common share details–as long as the asset coverage ratio is solid I am all for the common holders guaranteeing my investment.

Ok, i read their prospectus. Last Fall they were at 310% coverage, along with some verbiage around maintaining 200%.

It’s easy to get information overload with all the metrics out there. Here’s all you need to know. Assuming the minimum 200% level of coverage, half of their diversified portfolio of loans/bonds would need to default before the preferred was impaired. The record for default rates is 10.5% in the GFC. So, defaults would have to be 4-5x worse than the worst on record. If that came to pass, the entire financial system would be well past collapse. The kind of scenario where that could happen would either be war or a black swan like an EMP or much more fatal pandemic.

CEF preferreds are issued to raise cash to buy more investments for the CEF. It is implausible to me that it could possibly make economic sense to borrow at 5.25% when the average junk bond is less than that.

So it seems like a pretty terrible idea for ACP holders, but as I’ve said before, whether the CEF common is attractive has very little to do with whether the preferred is attractive. Due to quarterly asset coverage tests, all you really need to see is that the CEF holdings are reasonably liquid and not likely to fall so fast in price that the preferred would be impaired. ACP’s holdings are pretty junky, but ACPPP will be fine unless there is a catastrophic decline in risk assets.

The economic sense is that it will allow the sponsor to increase AUM and that in turn increases their management fee. That is what one sees in badly run CEFs. I have always considered Aberdeen to be among the worst of the CEF families. They go the route of high payout at the expense of destruction of capital.

Head on over to CEF data and check out the 10-year return on NAV. 20th out of 21 funds. Barely half of the top performing fund. Hot hand recently, thought, but that’s a product of what they own rather than brilliant management. Their biggest holding is an ETF. You are paying an arm and a leg in fund fees on this one and they go out and buy an ETF with an additional 49 bps in fund fees.

Would I hold my nose and buy the preferred? Maybe, at the the right price.

Bob, yeah I’m talking about logic for holders of ACP, not the managers.

“ ACP’s holdings are pretty junky, but ACPPP will be fine unless there is a catastrophic decline in risk assets.”

Yeah, folks should be aware that they are not holding CLO equity. With that, the economy could sneeze and wipe out CLO equity (well, more than a sneeze but anyone who tells you they truly know how much is lying).

I didnt take a peek at what they hold, but in prospectus CLOs are in their risk statement, as well as their strategy.

Risks of Structured Products. The Fund may invest in structured products, including collateralized debt obligations (“CDOs”), collateralized bond obligations (“CBOs”), collateralized loan obligations (“CLOs”).

A closed-end fund that seeks attractive risk adjusted returns …including non-stressed and stressed credit obligations, and related derivatives;

These should be listed in their structured products listings.

I don’t see any CLO equity in their top 10 holdings. A minor amount wouldn’t be a concern. CLO debt would be fine as it’s a lot safer, similar to ordinary high yield bonds.

The management fee is closer to 2%. 3% includes the cost of leverage. Leverage is good if it’s properly done, not just to boost AUM for the benefit of the sponsor.

That said, 2% is on the very high side for a CEF. For 1-1.25% you can get a well managed fund that actually adds alpha.

So the shunned OPP-A was a decent market rate, esp when it was lower? Hmmm. I have a few open orders too, will reports when I stop if I get a fill. Now, we’re eating each others young. This is a FOMO driven market now.

Thanks for the info, but the beauty and isolation makes up for the action.

Tempted to just buy a twenty years certain annuity and just check out.

25.85

Right james–now actual trades in the 25.85-25.87 area.

Continuing to fly higher. Now $26.28.

My price, my terms. Let’s see a working bid/ask somewhere, 20 minutes in. Real time quotes…a nice ad.

No cell service here in Hot Springs, NC. so perhaps we can use III for a close to real time FILL price. Thanks Tim.

Value is what you get, price is what you pay.

I may place some staggered orders and walk off.

Joel–I am seeing a 25.75 bid, but don’t see actual trades.

At 25.75 the YTC is 4.58%

I have an order in Steven at 25–we will see what happens. I want this one for the ‘sock drawer’ but don’t know if I want to chase it.

hi Tim, Me too.. Schwab allowed me to enter a trade online but just sitting there. Won’t hold my breath on my $25 order. I won’t chase as well..

GL

25.50 was showing for a long time, but none of my brokers will let me place a trade.

Looks like the price is going to get away quickly. It is already at a worse yield than what you can get the Allianz for before the first share trades. But the Allianz is callable in2023 IIRC.

Scott–etrade allowed an order, but I am not seeing actual trading.

8,000 shares, last trade at 25.80

At Fidelity had to call and place an order. According to the representative after being on hold about 12 minutes there isn’t any action at this time. according to him it was supposed to start trading yesterday but there is no information on it. He placed an order for me as their system would not let me do it.

TD now taking orders, but price is higher than I would buy so I put a limit in just in case it floats lower after the initial surge.

Has this issue actually started trading ?

Thanks

Waiting Gary–I see a 25.75 bid, but no ask and no trades.

5.25%. Not bad for an A2 rating, with CEF leverage rules, in the current environment. I expected slightly lower.

rjz–I’m loving it and it will go in the ‘sock drawer’