Opening the week at 3142 the S&P500 moved lower to 3126 on Tuesday before moving higher to close the week at around 3169–short of a 52 week high in the 3183 area.

The 10 year treasury opened the week around 1.83% and drifted plus and minus a few basis points before taking a run all the way to 1.92% on Wednesday based on never ending Chinese trade rumors. Rates then drifted lower as the trade ‘deal’ turned in to not much at all–closing the week at 1.82%. We shall see the veracity of Chinese ‘deal ‘ claims this coming week – I would not be surprised to see rates drift through the week.

The FED balance sheet grew again last week–this time by $30 billion for a 3 week total of $65 billion–this non-QE, quantative easing is really quite the joke as FED explanations make little sense and as some on the site have posited–Who is in trouble? Is it the German derivative king Deutsch Bank (DB)? Or is the FED simply monetizing the massive debt of the U.S. Government? Sooner or later we will find out what the hell is up–but for now ‘party on’ -ignorance is bliss.

Last week we had a number of new issues priced.

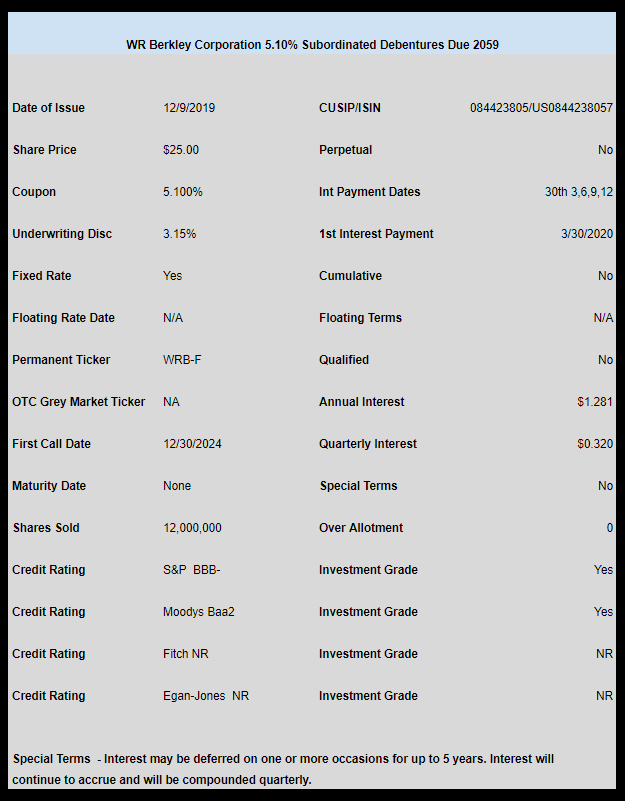

Insurer WR Berkley (WRB) priced a new baby bond. The issue is not trading as of yet.

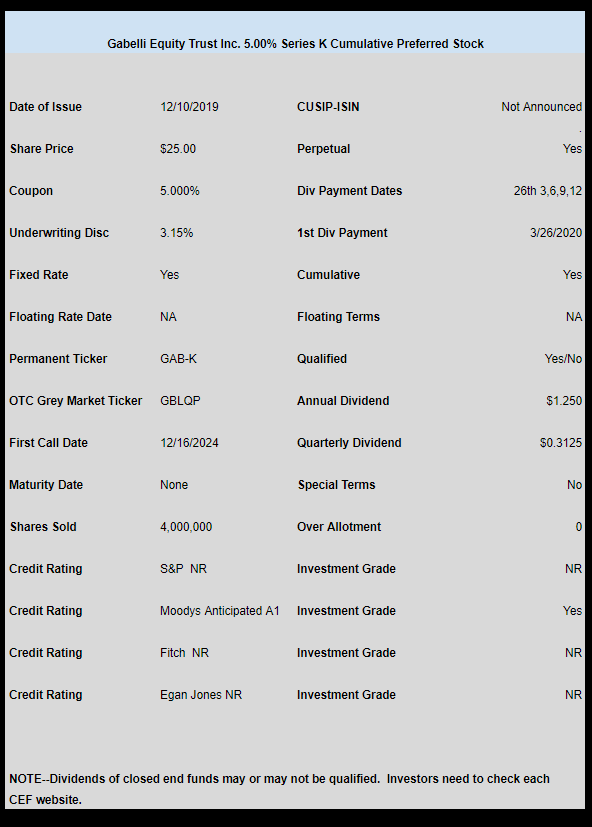

Closed End Fund Gabelli Equity Fund (GAB) priced a new 5.00% perpetual preferred which is now trading under OTC ticker GBLQP and last traded at $25.26

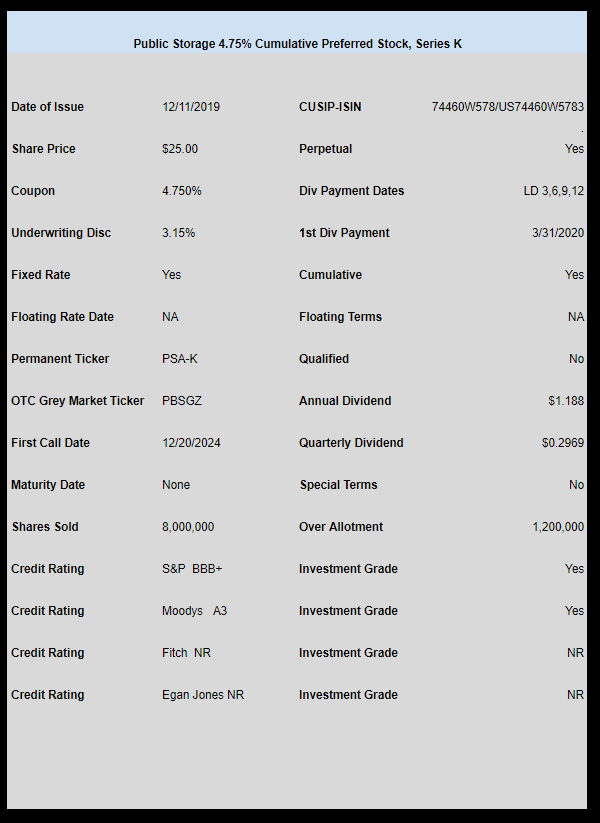

Self storage giant Public Storage (PSA) priced a new perpetual preferred issue with a coupon of 4.75% which is trading under temporary OTC ticker of PBSGZ. The issue last traded at $25.10.