Irrespective of the 10 year treasury being at 3.48% there remains plenty of ‘fear’ from income investors–not about interest rates.

Generally we have prices that move with interest rates from the preferreds and baby bonds–but there are times–like now when the baby gets tossed out with the bath water as folks say ‘let me out’!! Quite obviously we are in the soup until we gain back a level of confidence in the banking system–and that is still weeks away. First Republic (FRC) is gyrating as the BIG banker talk of further actions.

I noticed someone snagged some of the Tri-Continental 5% preferred (TY-P) today at $47.29. Unfortunately it wasn’t me but 1,319 shares changed hands–heavy volume for this one–looks like a ‘get me out’ trade by the seller. I do have a G-T-C buy order in at slightly lower levels.

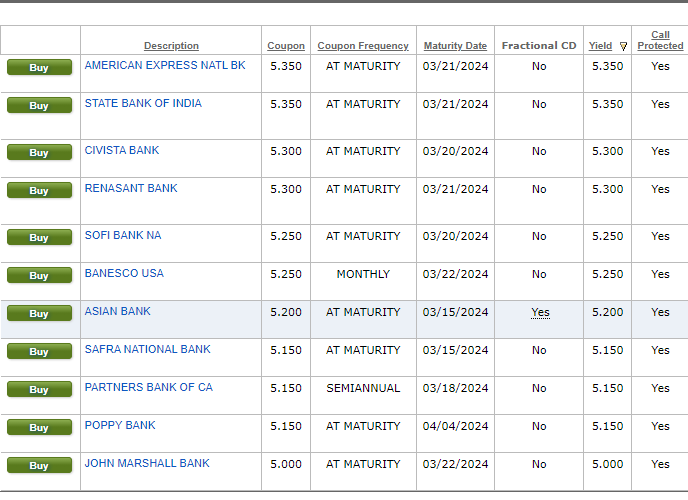

Just reviewed the CD rates–mostly out of curiosity, because I am not looking for more of them. Yields are off maybe 20-30 basis points depending on the maturity date and call protection provided.

So I am watching but not acting–need a bit more market confidence, but there are a number of utility issues I am watching and will write about in the next few days.